Introduction

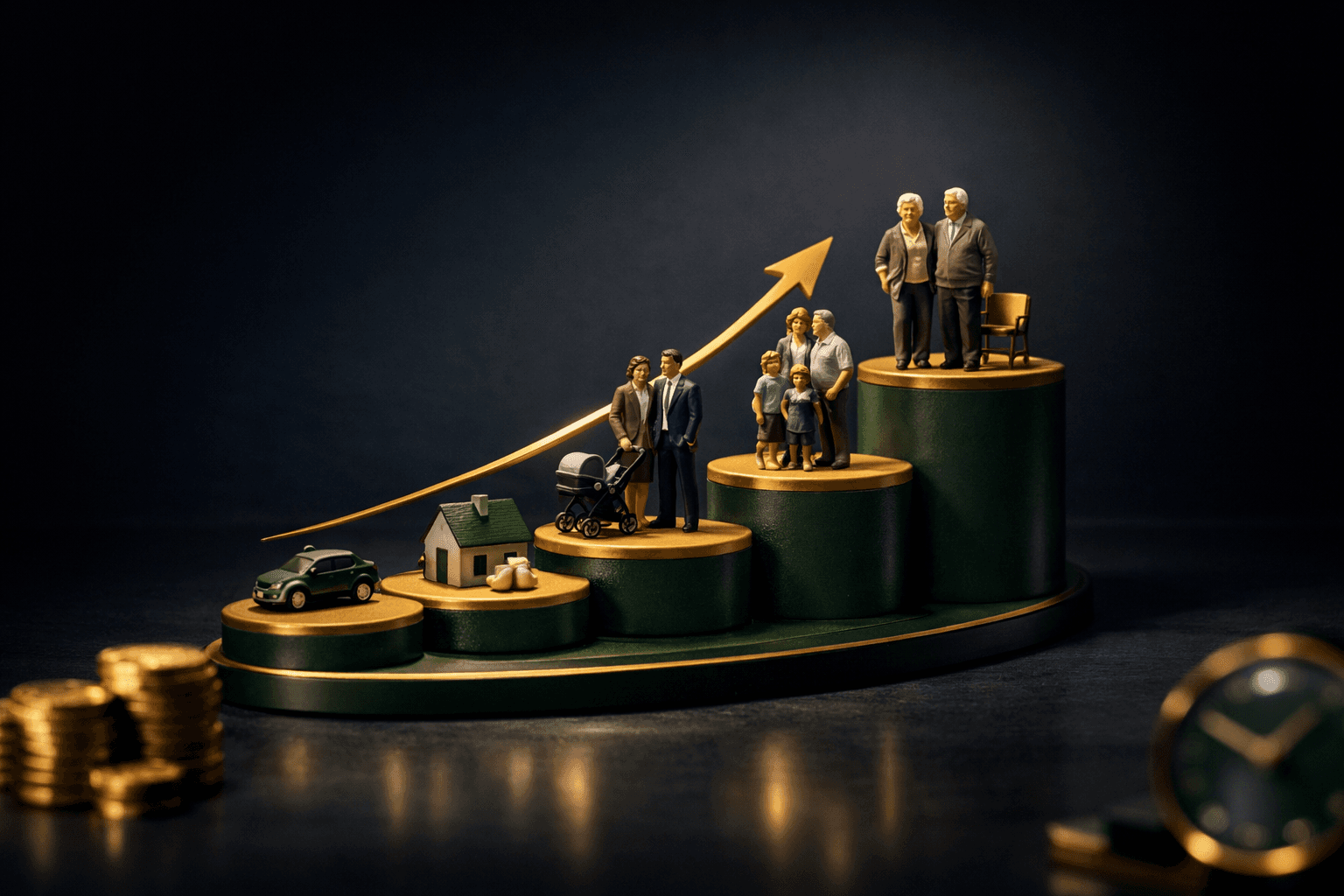

Life-stage investing means changing a portfolio to match an investor's age, goals, and time horizon. How should you adjust investments as life changes? That simple question drives the core idea: longer time horizons can usually tolerate more risk, while shorter horizons need more capital protection.

This guide explains why allocation should evolve and previews what follows: basic risk principles, sample allocations by decade, target-date funds and glide paths, rebalancing rules, and concrete examples using well-known ETFs and stocks. Read on for clear, actionable steps to keep a portfolio aligned with long-term financial objectives.

Key Takeaways

- Time horizon is the single biggest factor when setting allocation: more years to retirement generally means more equity exposure.

- Young investors often prioritize growth with higher stock allocations, while those near retirement shift toward bonds and income-producing assets.

- Target-date funds automate gradual shifts in allocation through a glide path, making them useful for hands-off investors.

- Regular rebalancing and periodic reviews after life events keep risk in check and maintain the intended asset mix.

- Practical tools include broad ETFs like $VTI for stocks and $BND for bonds, plus dividend ETFs like $VIG for income exposure.

Why risk tolerance changes with age

Risk tolerance often depends on two things: emotional comfort with volatility and the investment time horizon. A longer horizon gives more time to recover from market downturns, which supports larger allocations to higher-return assets like stocks.

Historical returns illustrate the trade-off. U.S. large-cap stocks have averaged roughly 10% annualized over the long run, while broad bond indexes have returned about 5% to 6%. Higher expected returns come with higher short-term swings, so the closer someone is to needing the money, the more critical capital preservation becomes.

Typical asset mixes by life stage

Below are sample allocations aimed at beginners as starting points. These are not investment recommendations but illustrations of common approaches. Think of these as templates to be adjusted for personal risk tolerance and goals.

Age 20s: Growth-focused

Sample mix: 90% stocks, 10% bonds. With decades until retirement, many younger investors emphasize equity exposure to benefit from compounding and higher long-term returns. A practical portfolio might include $VTI for broad U.S. stock exposure and $QQQ or select growth names like $NVDA for higher growth tilt.

Age 30s and 40s: Balance growth with increased diversification

Sample mix: 80% stocks, 20% bonds in the 30s, shifting to 70/30 in the 40s. As financial responsibilities grow, adding bonds reduces volatility. International stocks and small-cap funds can add diversification across regions and company sizes.

Age 50s: Preparing for income

Sample mix: 60% stocks, 40% bonds. The focus shifts toward protecting accumulated capital while still pursuing growth. Including dividend-growth ETFs like $VIG can introduce an income element without fully abandoning equity exposure.

Age 60s and retirement: Capital preservation and income

Sample mix: 40% to 60% bonds, depending on retirement timing and income needs. More emphasis on high-quality bonds, a bond ladder or short-duration funds, and dividend or real estate income sources helps support withdrawals during retirement while limiting sequence-of-returns risk.

Tools and products that make life-stage investing easier

Several investment vehicles simplify managing allocation over time. Target-date funds are one of the most common choices for retirement accounts because they adjust the mix automatically. A glide path is the schedule that defines how the fund shifts from aggressive to conservative as the target date approaches.

Target-date funds from large providers, for example Vanguard target-date series, typically start with high stock exposure and reduce equity weight as the selected retirement year nears. For hands-off investors, this automation can replace manual reallocation and help maintain an appropriate glide path.

Practical steps to change allocation over time

Follow a clear process to move from theory to action. First, set a baseline allocation that reflects the time horizon and risk preference. Second, automate contributions into that allocation using dollar-cost averaging to reduce timing risk.

Next, rebalance regularly. Many investors rebalance annually, or whenever an asset class drifts by a defined threshold such as 5 percentage points. When rebalancing, move proceeds from outperforming assets into underperforming ones to bring the portfolio back to target. For taxable accounts, consider tax consequences before selling taxable gains.

Reallocation after major life events

Significant life changes like marriage, home purchase, job change, inheritance, or health issues warrant a portfolio review. It's sensible to adjust allocation after these events to reflect new goals, cash needs, or income sources. Don’t make knee-jerk decisions during market stress, but do stick to a regular review schedule.

Real-world examples

Example 1: A 25-year-old starts with $10,000 and contributes $500 monthly to a 90/10 split using $VTI and $BND. With a hypothetical average return of 7% annualized, the portfolio compounds significantly over 40 years, illustrating how time and regular contributions work together.

Example 2: A 55-year-old with $500,000 decides to shift from 80/20 to 60/40 over five years to reduce volatility while still chasing some growth. The investor uses a laddered approach by moving 4% of the portfolio each year from equities into a mix of $BND and short-term investment-grade bonds, smoothing the transition.

Example 3: An investor who prefers automation picks a target-date fund for a retirement year about 30 years away. The fund starts at roughly 90% stocks and reduces equity exposure gradually along its glide path to about 50% stocks at retirement, removing guesswork from the process.

How to think about withdrawals and sequence-of-returns risk

As retirement approaches, the risk of withdrawing funds during poor market performance increases. To mitigate sequence-of-returns risk, many retirees keep an emergency cash buffer covering 1 to 3 years of expenses. Bond ladders and short-term Treasury bills can also act as a liquidity cushion while longer-term assets remain invested for growth.

Adjust withdrawal rates conservatively. A common rule of thumb is the 4% rule, which suggests withdrawing about 4% of the initial portfolio value annually, adjusted for inflation. This is only a starting point and must be adapted to changing market conditions and personal needs.

Common Mistakes to Avoid

- Chasing past winners: Moving heavily into recently hot sectors increases risk, as past performance rarely predicts future returns. Stick to a plan that fits long-term goals.

- Ignoring rebalancing: Letting a portfolio drift can unintentionally increase risk. Rebalance on a regular schedule or when allocations deviate by a preset amount.

- Overreacting to market downturns: Selling after big drops locks in losses. A disciplined plan often outperforms emotional reactions over long horizons.

- Failing to update the plan after life changes: Major life events can change goals, time horizons, and cash needs. Review allocation after significant personal or financial changes.

FAQ

Q: At what age should I start shifting from stocks to bonds?

A: Start shifting as your time horizon shortens and the need for capital preservation grows. Many investors begin modest shifts in their 50s, with larger changes in the decade before retirement. Personal goals and risk tolerance matter more than exact age.

Q: What is a glide path in a target-date fund?

A: A glide path is the programmed schedule a target-date fund follows to reduce equity exposure and increase fixed-income exposure as the target retirement date approaches. Glide paths vary by provider and can be steeper or more gradual.

Q: How often should I rebalance my portfolio?

A: Common approaches are annual rebalancing or rebalancing when allocations drift by a set threshold like 5 percentage points. The right choice depends on tax considerations, trading costs, and the investor's willingness to monitor the portfolio.

Q: Can I use target-date funds for all my retirement savings?

A: Target-date funds are convenient for a hands-off strategy and work well inside retirement accounts. However, if an investor wants more control over asset mix, tax-efficient moves across accounts, or specific income strategies, a customized allocation might be preferable.

Bottom Line

At the end of the day, life-stage investing is about aligning risk with time horizon and financial goals. Start with a clear allocation plan, automate contributions, and adjust the mix as the need for capital protection increases.

Make a plan that fits goals and timelines, rebalance regularly, and review the portfolio after major life events. With a disciplined approach, it’s possible to pursue growth when there's time and protect capital when retirement nears.