Introduction

Bond laddering is a fixed income strategy that staggers maturities across several dates so you regularly receive principal back and can reinvest at current rates. It helps investors manage interest rate risk while preserving predictable cash flow and avoiding the single-point risk of a long-term bond.

Why does this matter to you? Because interest rates move, and those moves change bond prices and future yields. A ladder smooths the impact of those moves so you don't have to time the market to capture attractive yields.

This article explains how laddering works, shows step-by-step construction, covers reinvestment mechanics, compares ladders to bond funds, and includes real-world examples. You'll learn how to build a ladder for different goals and what mistakes to avoid.

- Stagger maturities so you receive principal regularly and reinvest at current rates, reducing interest rate risk.

- Ladders reduce price volatility because only a portion of the portfolio is exposed to long-duration risk at any time.

- Reinvestment helps capture rising rates, while initial diversification across maturities cushions falling-rate scenarios.

- Use ladders when you need predictability, control over credit and tax attributes, or liquidity for specific future needs.

- Bond funds offer diversification and active management, but they carry ongoing duration exposure and potential liquidity-driven price swings.

- Watch for common pitfalls: concentrated maturities, callable bonds, credit risk, and tax consequences.

How a Bond Ladder Works

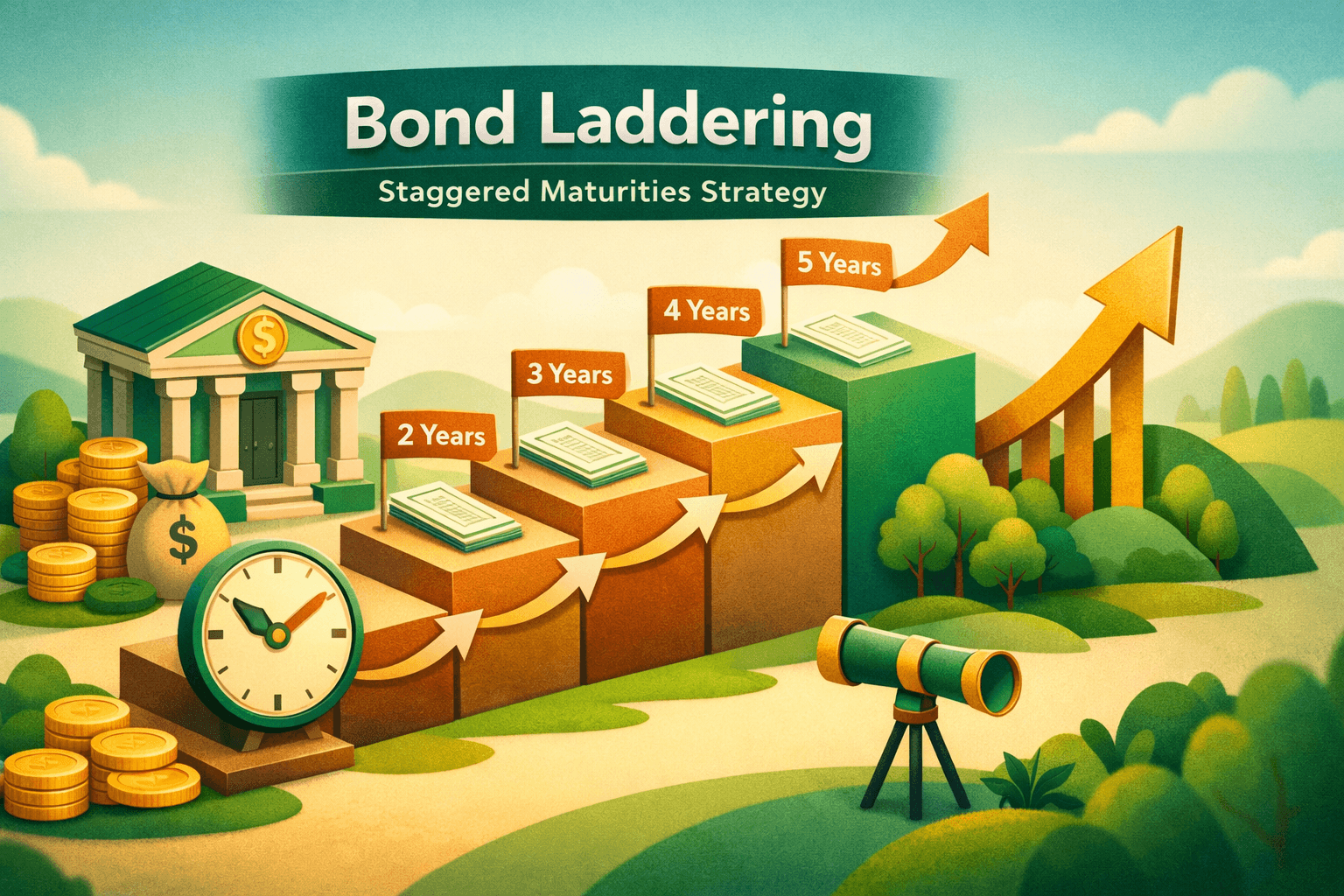

At its simplest, a bond ladder holds a set of bonds with staggered maturities, for example one-year, two-year, three-year, four-year, and five-year maturities. Each year one rung matures and returns principal to you, which you can spend or reinvest at the long end to rebuild the ladder.

A ladder reduces interest rate risk in two ways. First, only the longer-maturity rungs have high duration and larger price sensitivity. Second, regular maturities mean you can reinvest when rates rise, capturing higher yields over time. That makes the strategy less dependent on rate timing.

Key concepts, defined

- Duration, a measure of price sensitivity to rates, falls for shorter maturities and rises for longer ones.

- Reinvestment risk is the danger that future coupon and principal payments must be reinvested at lower rates.

- Credit risk is the chance the issuer defaults, which you manage by issuer diversification or using government securities.

Building a Bond Ladder: Step-by-step

Start by defining your objective, the ladder size, and the target maturities. Are you saving for a specific liability such as tuition in five years, or do you want ongoing income? The answer determines ladder length and bond types.

Next, choose the type of bonds. Options include Treasury securities, municipal bonds for tax-exempt income, corporate bonds for higher yield, and bond ETFs for ease of execution. You can mix types to balance yield, credit quality, and tax treatment.

Practical construction example

Suppose you have $100,000 to allocate to a 5-year ladder with equal notional amounts. You buy five bonds each with $20,000 par and staggered maturities at 1, 2, 3, 4, and 5 years. Example yields at purchase:

- 1-year: 2.0%

- 2-year: 2.2%

- 3-year: 2.6%

- 4-year: 3.0%

- 5-year: 3.5%

Each year the bond maturing returns $20,000 principal plus coupon income. You reinvest the $20,000 into a new 5-year bond, keeping the ladder length constant. Over five years your portfolio will continually refresh and converge toward prevailing rates.

Execution tips

- Use round notional amounts for cash management and tracking.

- Prefer bullet maturity dates to avoid clustered call risk.

- Consider using Treasury STRIPS or high-quality corporates depending on credit tolerance.

Reinvestment Mechanics and Yield Dynamics

Reinvestment is the engine of ladder returns. Every time a rung matures you reinvest principal at current yields, which increases portfolio yield if rates rose since purchase and vice versa if rates fell. That makes the ladder adaptive.

Here is a numeric scenario to make it concrete. Using the prior 5-year ladder example, suppose rates jump after year one and 5-year yields rise from 3.5% to 5.0% when you reinvest the first $20,000. By buying a 5-year at 5.0% you immediately lock a higher long-term yield on that rung.

Contrast that with owning a single 5-year bond bought at 3.5%. If rates rise to 5.0% its market price will fall, causing an unrealized loss if you sell. With the ladder you only hold one matured principal at a loss of opportunity and you capture the higher rates going forward.

Average yield illustration

Assume all coupons are paid annually and you reinvest principal into new 5-year bonds each year. If rates rise steadily, the average yield of the ladder will increase gradually as more rungs are replaced at higher yields. If rates fall, the ladder retains higher yields on earlier rungs until they roll off, smoothing the decline in average yield.

Laddering vs Bond Funds: When to Use Each

Both ladders and bond funds give access to fixed income, but they suit different investor needs. A ladder gives you control over maturity dates, credit selection, and tax lot management. A bond fund gives instant diversification and professional management, but you do not own individual bonds and you face perpetual duration exposure.

Use a ladder when you want predictable cash flows, a scheduled stream of maturities for liabilities, or control over credit and tax attributes. Use bond funds for small account sizes, broad diversification across many issuers, or when you prefer liquidity without managing individual securities.

Practical ETF examples

- $SHY is an ETF that tracks short-term Treasuries, similar to the short end of a ladder.

- $BND is a broad aggregate bond ETF, representative of a bond fund alternative to building a full ladder.

- $TLT tracks long-duration Treasuries and behaves like the long rungs in a ladder but without fixed terminal cash flows to you unless you sell.

Note that bond funds report yield-to-worst and effective duration. Those metrics matter because the fund's NAV will change with rates, and you face market price risk even though there is daily liquidity.

Real-World Examples

Example 1, conservative ladder for a near-term liability: You need $50,000 in three years for a down payment. Build a 3-year ladder with $50,000 split into three rungs of $16,667 each at 1-, 2-, and 3-year maturities using Treasury or high-grade municipal bonds. That way you have increasing portions of principal maturing each year and can meet the liability with minimal price risk.

Example 2, income-focused ladder: You have $500,000 for income and choose a 10-year ladder to capture higher long-term yields. You purchase ten corporate bonds staggered annually, diversify across industries, and avoid callable issues. As each rung matures you roll it into a new 10-year security to maintain ladder length and capture prevailing rates.

Example 3, converting a bond fund to a ladder: Suppose you hold $100,000 in $BND but want scheduled maturity control. You can sell $BND in tranches and buy individual bonds with maturities you choose. Be mindful of transaction costs and taxable events when selling fund shares.

Common Mistakes to Avoid

- Concentrating maturities: Buying many bonds that mature at the same time defeats the ladder's diversification. Stagger maturities evenly to keep regular liquidity.

- Ignoring callable bonds: Callable bonds can be redeemed early by the issuer, which breaks ladder timing. Avoid callable issues if you need predictable maturities.

- Neglecting credit diversification: Holding many bonds from one issuer increases default risk. Spread credit exposure across issuers and sectors or favor government securities for lower credit risk.

- Forgetting tax and transaction costs: Municipal yields may look lower but are tax-advantaged. Also account for brokerage fees and bid-ask spreads when buying individual bonds.

- Assuming ladder eliminates all risk: Ladders reduce but do not remove interest rate, credit, or reinvestment risk. Be explicit about the residual risks.

FAQ

Q: How many rungs should my ladder have?

A: There is no one-size-fits-all number. Common choices are 3 to 10 rungs. Shorter ladders give simpler management and quicker access to cash. Longer ladders provide broader maturity diversification and smoother rate capture. Match the count to your liquidity needs and portfolio size.

Q: Can I ladder using bond ETFs instead of individual bonds?

A: Yes, you can stagger ETFs by duration, for example using $SHY for short, mid-duration ETFs for the middle, and $TLT for long. Remember ETF shares do not mature, so you must sell to access principal. That exposes you to NAV fluctuations unlike holding individual bonds to maturity.

Q: Should I include callable bonds in a ladder?

A: Generally avoid callable bonds if predictability is important. Callable bonds can be redeemed at the issuer's discretion, shortening maturities and creating reinvestment risk at often lower yields.

Q: How do taxes affect ladder decisions, especially municipal bonds?

A: Municipals can be attractive for taxable accounts because interest is often tax-exempt at the federal level and sometimes at state level. Compare after-tax yields across municipal, Treasury, and corporate options when constructing a ladder, and consider tax lots for reinvestment decisions.

Bottom Line

Bond laddering is a practical, flexible way to manage interest rate risk while maintaining regular liquidity and control over maturities and credit exposure. It smooths both price volatility and reinvestment outcomes by spreading risk across time.

If you need predictable cash flows for liabilities, want control of tax or credit attributes, or prefer to lock in yields gradually, a ladder is often a good choice. If you prefer professional management and broader instant diversification, bond funds or ETFs may be more appropriate.

Start by defining your cash needs, decide the ladder length, select maturities and credit quality, and monitor reinvestment opportunities each time a rung matures. At the end of the day a ladder gives you a disciplined, low-complexity way to navigate a changing rate environment.