The Big Picture

Renewables and grid investment set the tone for the utilities sector on May 26, with major solar projects coming online, a strong quarter for energy storage, and a sizable slate of transmission proposals from CAISO. These developments matter because they accelerate capacity additions and long-term demand for grid services, which shape utility planning and corporate offtake strategies.

You’re seeing momentum across multiple fronts, from behind-the-meter university arrays to 400 megawatts of commercial solar backed by global brands. What does that mean for the pace of clean-energy deployment, and can the policy backdrop keep up?

Market Highlights

Today’s headlines show concrete capacity and contract wins, while trade group data underlines structural growth in storage. Specific market pricing moves were not reported in the itemized stories, but the news flow points to stronger fundamentals for renewable developers, storage integrators and transmission contractors.

- Sequoia Solar, Callahan County, TX: First phase 400 MW now operational, delivering power under long-term PPAs to $TM, $PEP, $T and $DCI. A 415 MW second phase is expected by year-end.

- DESRI New Mexico portfolio: Ground broken on 270 MW of solar plus storage including a 170 MW solar site paired with an 80 MW, 320 MWh battery system under a long-term PPA with the Incorporated County of Los Alamos.

- University of Michigan Maize Rays: Two behind-the-meter arrays added on North Campus, part of a 2.5 MW target across seven sites on Ann Arbor and Dearborn campuses, feeding the university grid directly.

- Energy storage: SEIA reports Q1 installations hit a record, up 32% year over year, with a projection of 613 GWh of deployment by 2030, driven in part by data center demand.

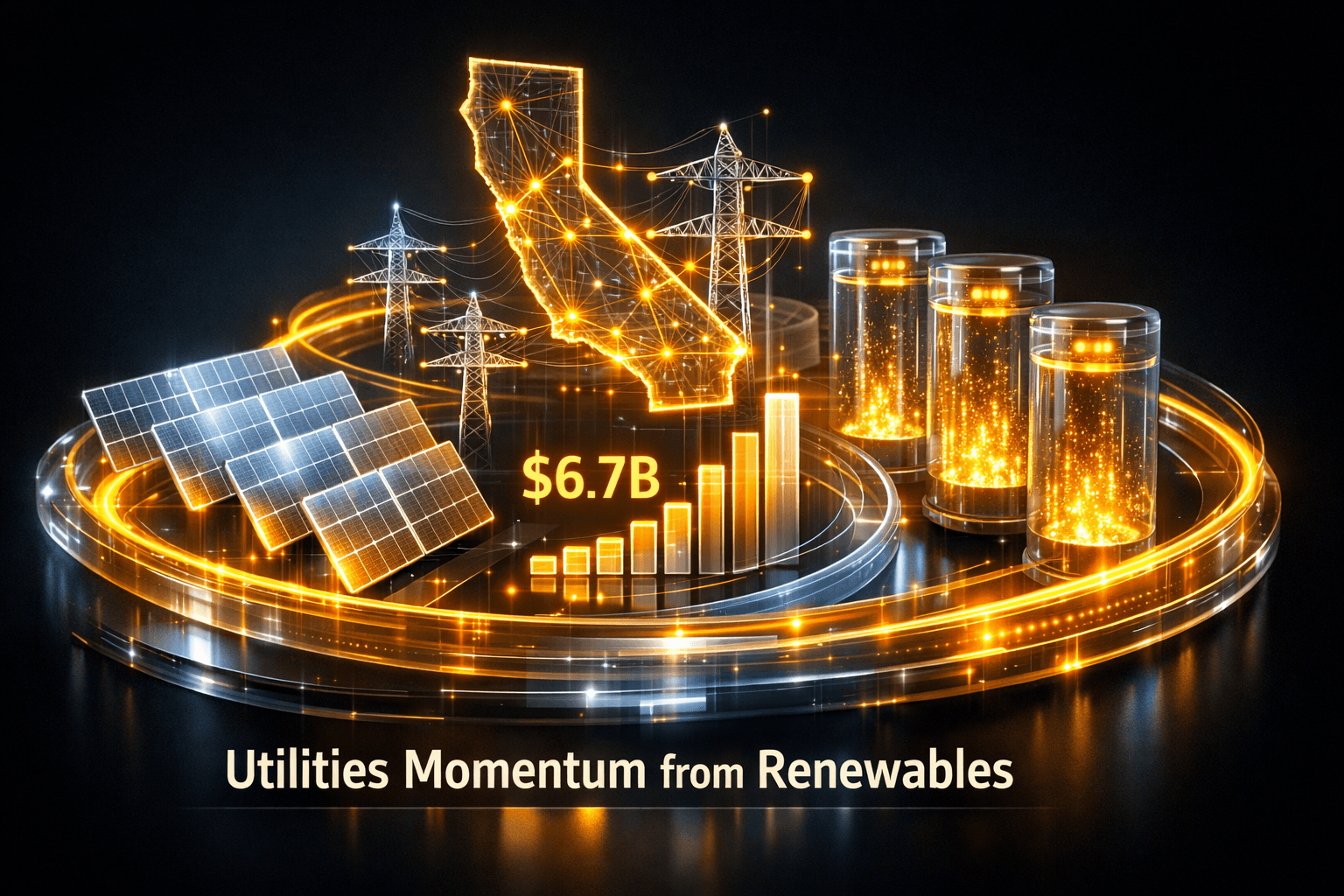

- Transmission: CAISO recommended 38 projects with an estimated cost of roughly $6.7 billion to meet forecasted load growth and expand reliability.

Key Developments

Corporate offtakes boost large-scale solar: Sequoia’s first phase online

Enbridge’s Sequoia Solar project reached commercial operation on its 400 MW first phase, backed by PPAs with AT&T, Toyota, PepsiCo and Donaldson Company. These corporate offtakes demonstrate continued private-sector demand for clean power and help underpin financing for large utility-scale builds. For you that means offtake-driven projects are likely to remain a core growth channel for developers and for utilities seeking contracted supply.

Storage and repowering signal capacity build and lifecycle work

SEIA’s Q1 report showing a 32% YoY increase in installations underscores rapidly expanding battery deployments. At the same time, industry coverage on wind repowering notes an upcoming wave of projects where owners will reuse sites and grid interconnections to boost output. Together these items point to both net-new capacity and modernization work for existing assets, a combination that supports sustained activity for equipment suppliers and EPC contractors.

Grid strengthening: CAISO’s $6.7B plan and behind-the-meter projects

CAISO’s recommendation of 38 transmission projects totaling about $6.7 billion highlights a shift in planning, from simply accessing low-cost renewables to reliably meeting rising customer demand. That pairs with smaller scale behind-the-meter efforts like the University of Michigan’s 2.5 MW Maize Rays program, which keep load localized and reduce distribution strain. The mix of bulk transmission and local solar-plus-storage will shape procurement needs for utilities and municipal customers.

What to Watch

Look to project timelines and policy signals tomorrow and in the weeks ahead. You’ll want to keep an eye on PPA start dates, interconnection queues, and the pace of CAISO approvals because those determine when capacity hits the system and when revenue streams begin.

- Project milestones: Monitor Enbridge’s second Sequoia phase targeting 415 MW by year-end, and DESRI’s construction progress on Foxtail Flats and Four Mile Mesa.

- Regulatory and policy risks: SEIA flagged federal gridlock as a threat to storage’s trajectory, so any legislative movement or regulatory approvals will be material to deployment forecasts.

- Demand signals: Rising EV adoption globally, illustrated by Colombia’s 316% April EV sales increase and near 20% BEV market share, will keep load growth and charging infrastructure demand on your radar.

- Supply chain and repowering schedules: With more than 75,000 turbines aging, repower contracts will create opportunities and execution risks for owners and contractors.

Can this momentum continue without clearer federal support? You’ll want to watch whether policy catches up to project pipelines.

Bottom Line

- Major corporate PPAs and large utility-scale builds today point to durable demand for renewable generation and contracted revenues for developers.

- Record storage installations, up 32% YoY, reinforce the role of batteries in grid reliability and commercial procurement strategies.

- CAISO’s $6.7 billion transmission recommendations signal increased spending on grid capacity to meet load growth, not just access to low-cost renewables.

- Behind-the-meter projects and repowering efforts show the sector is investing at both distribution and bulk-grid scales, giving the industry a second wind.

- Policy uncertainty remains a key risk, so track regulatory moves closely because they can accelerate or slow deployment trajectories.

FAQ Section

Q: How do corporate PPAs affect utility planning? A: PPAs add contracted supply that can reduce pricing volatility and support financing for new projects while shaping utilities’ generation mix and transmission needs.

Q: Why does storage growth matter to you as a retail investor? A: Storage increases grid flexibility, enables higher renewable penetration, and creates recurring revenue opportunities for developers and integrators, according to industry data.

Q: What are the main risks to the renewables buildout? A: Key risks include federal policy gridlock, interconnection delays, and supply chain or permitting hurdles that can shift timelines and costs.