The Big Picture

The most impactful development for utilities this weekend is the continued buildout of grid-scale storage and EV charging infrastructure, offset by growing public scrutiny of the power needs tied to large AI data centers. You should care because these trends will shape electricity demand patterns, capital spending by utilities, and regulatory focus in the months ahead.

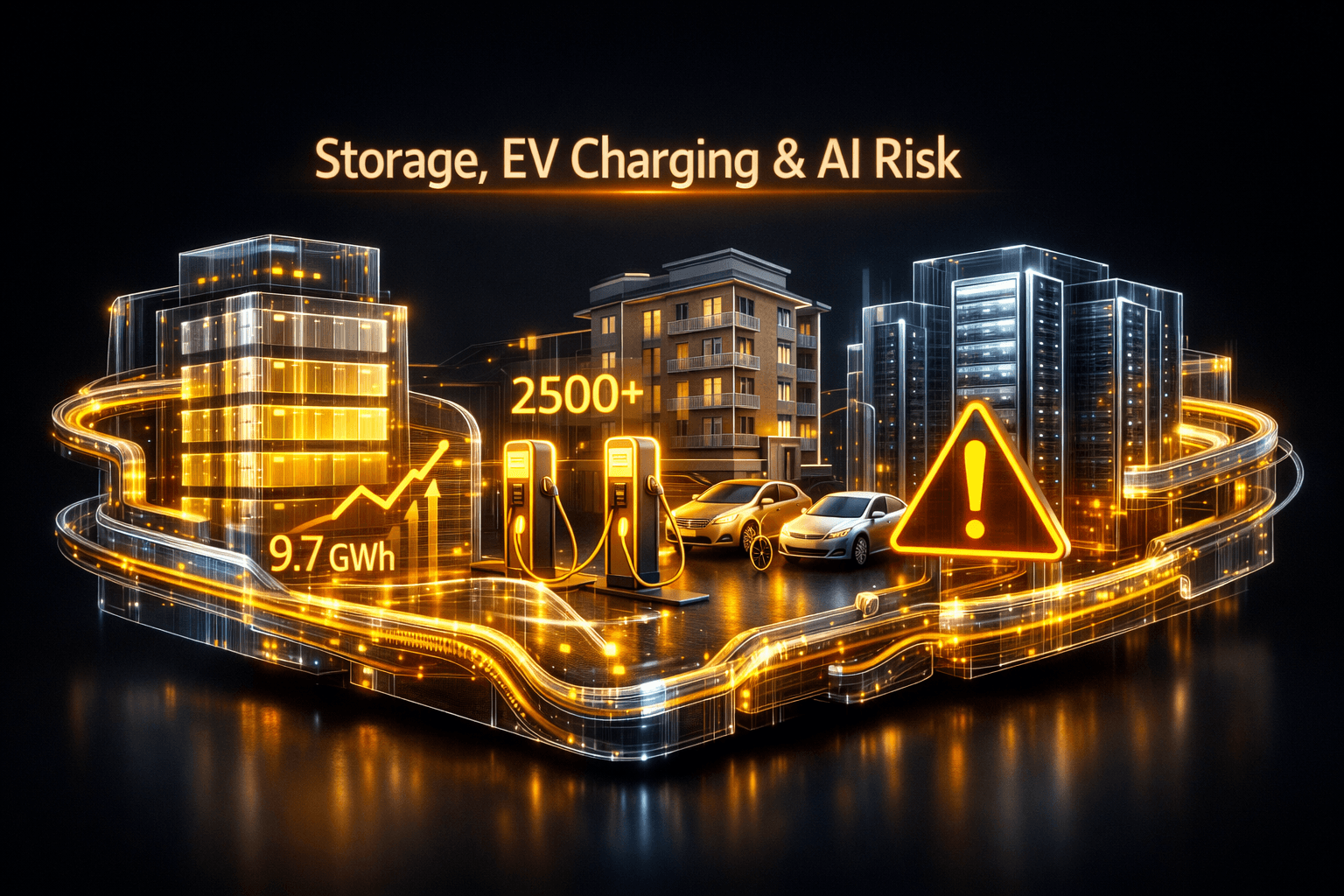

Record first-quarter energy storage deployments and a targeted push to install 2,500 chargers in multifamily housing point to rising distributed demand. At the same time, opposition to massive data-center growth raises questions about siting and permitting that could affect some large commercial power consumers.

Market Highlights

Heading into the long weekend, utility-sector fundamentals show both demand-side growth and policy risk. Here are the quick facts you need:

- Energy storage surge: The U.S. installed about 9.7 GWh of new energy storage capacity in Q1 2026, the strongest first quarter on record according to CleanTechnica.

- EV charging expansion: Developers plan 2,500 new EV chargers targeted at apartment and condo complexes, closing a key gap in multifamily charging access.

- AI data center scrutiny: A growing public debate over AI and the large data centers that support it is increasing opposition and could complicate future siting for high-demand facilities.

- Companies to watch include grid and storage players such as $NEE, $DUK, $AES, and charging or EV ecosystem names like $TSLA, $CHPT, $BLNK, which sit at the intersection of these trends.

Key Developments

Record Energy Storage Growth

CleanTechnica reports roughly 9.7 GWh of new U.S. energy storage capacity installed in Q1 2026. That marks the best Q1 on record and reflects stronger investment as grid operators and utilities prioritize resilience and flexibility.

For you as a reader, this means storage is transitioning from pilot to mainstream. Storage helps flatten peak demand, firm intermittent renewables, and creates new revenue streams for developers. Analysts note forecasts for storage capacity have been revised up over the next five years, driven in part by geopolitical concerns about energy security.

EV Charging for Multifamily Housing

Developers announced plans for 2,500 new EV chargers at apartment and condo complexes. Most EV charging still happens at single-family homes, but this targeted build addresses a structural barrier to EV adoption for renters and urban dwellers.

That shift is important for utilities because multifamily charging creates concentrated, often time-sensitive load. You should watch for utility pilot programs and rate designs that accommodate clustered charging, and for potential partnerships between utilities and charging operators as this rollout progresses.

Rising Opposition to AI Data Centers

Public opposition to AI and the large data centers that support it is growing, according to analysis published this weekend. Concern centers on energy use, local environmental impacts, and the scale of new data-center campuses.

For utilities, this could lead to longer permitting timelines, added conditions on power supply, or requests for community benefits. Do rising local objections mean fewer large commercial loads, or just more complicated planning? That question matters for regional load forecasts and for companies that supply high-density computing power.

What to Watch

Expect activity and potential volatility around a few near-term catalysts. First, utilities and independent power producers will publish Q2 guidance and project updates that reflect recent storage and charging wins. Second, regulators and local governments could respond to AI center controversies with new permitting rules or conditional approvals.

Keep an eye on federal and state grants or incentives for storage and charging, because additional subsidies could accelerate deployments. Also monitor utility filings on rate designs for EV charging, since those will determine how quickly multifamily charging becomes financially viable for building owners and tenants.

Finally, watch company announcements from $NEE, $AES, and charging operators like $CHPT and $BLNK for partnership or contract wins. Who signs large-scale storage or multifamily charging deals will shape market share going forward.

Bottom Line

- Energy storage momentum is real, with about 9.7 GWh added in Q1 2026, suggesting stronger grid flexibility demand ahead.

- Multifamily EV charging growth, illustrated by the 2,500-charger plan, removes a barrier to adoption and concentrates new load in urban areas.

- Public pushback on AI data centers introduces a regulatory and permitting risk that could slow some large commercial loads or change siting requirements.

- Be selective: growth opportunities exist in storage and charging, but regulatory and community risks mean execution matters.

- Data and policy developments over the next few weeks will clarify winners and timelines, so stay tuned into filings and corporate updates ahead of trading on Tuesday, May 26.

FAQ Section

Q: How big is the U.S. energy storage buildout so far in 2026? A: About 9.7 GWh of new capacity was installed in Q1 2026, the strongest first quarter on record according to the report cited.

Q: Will the new 2,500 EV chargers significantly boost overall EV adoption? A: The chargers target a key barrier for renters and urban drivers, so they can materially improve access in multifamily settings, but broad adoption still depends on broader charger availability and supportive policies.

Q: Could opposition to AI data centers reduce electricity demand growth? A: Local opposition may slow or reshape where and how large data centers are built, which could affect localized demand growth, but it does not eliminate the broader trend toward higher digital and compute-driven electricity needs.

Investment disclaimer: This article presents analysis and reported facts for informational purposes only. It does not recommend buying, selling, or holding any specific securities and is not personalized investment advice. Analysts note trends and data, but you should consult a licensed professional before making investment decisions.

Markets were closed on Sunday, May 24. The last U.S. trading day was Friday, May 22, and the next session opens on Tuesday, May 26. Keep an eye on corporate and regulatory news over the holiday weekend that could influence sector sentiment when markets reopen.