The Big Picture

Deal activity picked up across residential, industrial and hospitality sectors today, signaling renewed transaction momentum for developers and lenders. You saw sizable acquisitions, fresh construction financing and operational hires that together suggest market participants are deploying capital where returns align with current risk.

This matters because access to debt and active sponsorship translate into projects that move from planning to construction, which feeds local jobs and rental or sales supply. What should you watch for next, and how might this shape neighborhood-level values?

Market Highlights

Quick facts and notable moves from Jun 9 that investors and observers can use to frame near-term opportunities.

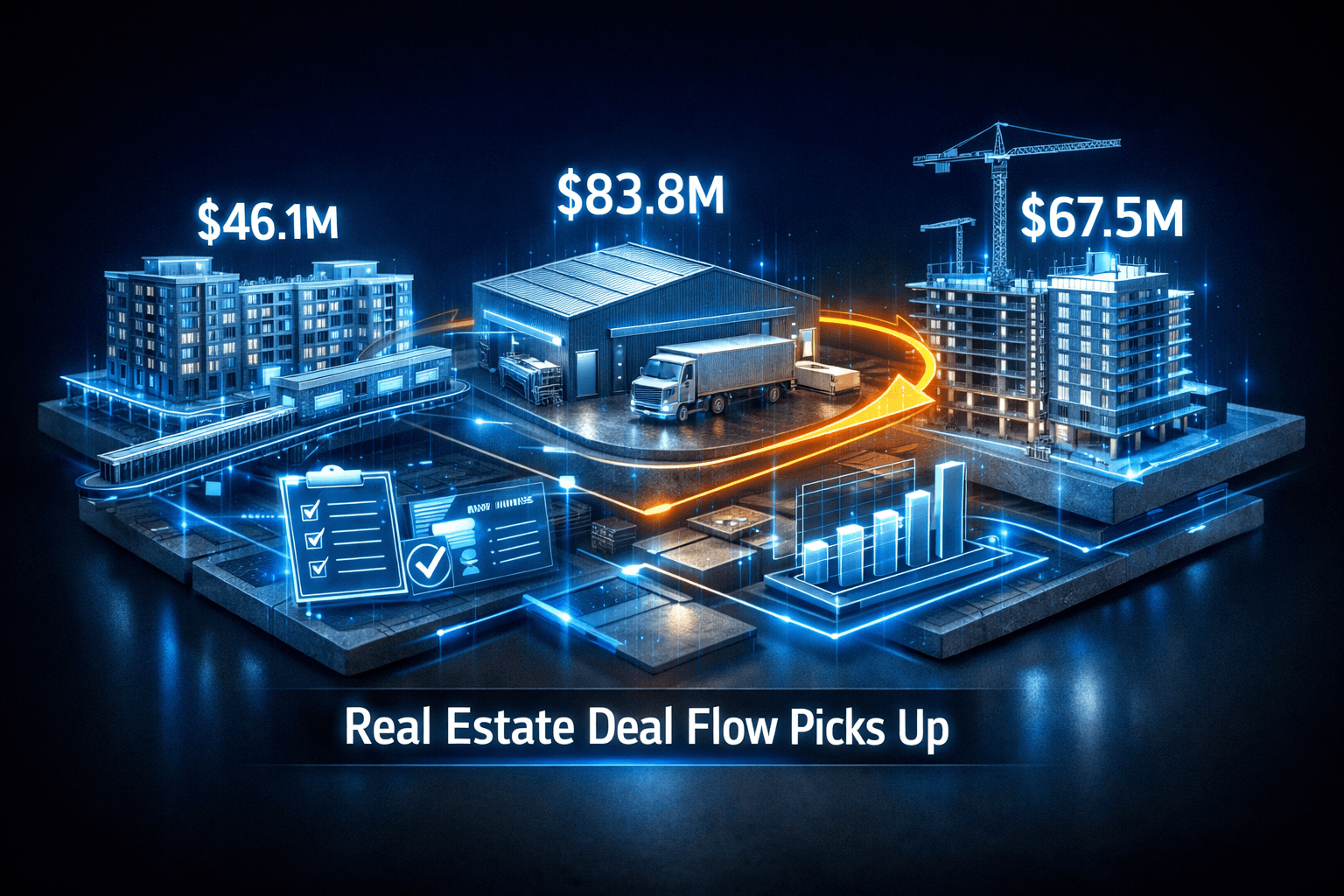

- Queens workforce housing site: Cirrus Real Estate Partners and Resorts World New York City closed on a 1.8-acre site at 92-30 165th St., Jamaica, Queens for $46.125 million, with more than 600,000 buildable square feet.

- Retail leasing in SoHo: French burger chain Junk Smash Burgers leased 2,150 square feet at Thor Equities' 452 Broadway, marking the concept's U.S. expansion into a high-rent Manhattan corridor.

- Hospitality sale: Marcus & Millichap arranged the sale of the 93-room Grand Marquis Waterpark Hotel & Suites in Wisconsin Dells, a long-held family asset now changing hands.

- Large-scale loans: Argentic provided roughly $83.8 million in floating-rate acquisition financing for an 11-building Atlanta industrial portfolio, and BHI supplied a $67.5 million construction loan for a 74-unit boutique condo project in Coral Gables.

- Major development unveiled: Craig International announced Rowlett Station, a $200 million mixed-use redevelopment in McKinney, Texas, on a 58-acre former office campus.

Key Developments

Workforce housing and urban infill moves

The Cirrus and Resorts World purchase in Jamaica is the headline acquisition of the day. At $46.125 million for a parcel with 600,000 buildable square feet, the deal points to continued appetite for large urban infill sites that can be positioned for workforce housing.

For you, that means more supply targeted at middle-income renters and buyers could be coming online in transit-connected parts of Queens. Analysts note such projects often require careful capital stacking and public approvals, but the scale here is notable.

Debt availability fuels projects from industrial to condos

Debt markets showed willingness to finance both industrial and for-sale residential development. Argentic’s $83.8 million floating-rate acquisition loan for an 11-building Atlanta logistics portfolio signals lenders still back industrial fundamentals.

Meanwhile a $67.5 million construction loan from BHI for Cora Merrick Park, a 74-unit boutique condo in Coral Gables, highlights continued targeted financing for coastal luxury and for-sale products. Will lenders keep pricing floating-rate debt, and how will that affect sponsor returns if rate volatility resurfaces?

Industry infrastructure and talent reinforce execution

Operational and policy items rounded out the day. MISMO updated its PaVS procurement dataset to support UAD 3.6, which standardizes valuation orders. The Mortgage Bankers Association launched a forum focused on reverse mortgages and senior lending, improving coordination around a growing segment of loan demand.

On the people front, Dermody hired Manali McCarthy as VP of investor relations to support fundraising and investor communication, a sign sponsors are preparing for more capital-raising activity.

What to Watch

Looking forward, several catalysts and risk factors will steer market direction. You should track these items closely.

- Project timelines and entitlements: Watch for permitting milestones on the Jamaica site and Rowlett Station in McKinney. Delays can push returns out and increase carry costs.

- Loan pricing and structure: Floating-rate financing played a role in today’s deals, so monitor short-term rate moves and lender appetite. If rates spike, sponsor spreads could compress.

- Policy and valuation standards: Adoption of MISMO’s UAD 3.6 updates and the MBA’s senior-lending forum may improve underwriting clarity, which could unlock more capital into specialized products like reverse mortgages.

- Retail and hospitality demand signals: New food and leisure tenants, and the sale of an established waterpark hotel, offer micro signs of consumer resilience. Keep an eye on occupancy and ADR trends in secondary leisure markets.

Bottom Line

- Deal flow is alive across sectors, with meaningful acquisitions in Queens and Atlanta and construction financing in South Florida showing capital remains deployable.

- Industry infrastructure updates and new forums reduce friction for lending and valuations, which may support more transactions if market volatility stays limited.

- Floating-rate loans are prominent in today’s headlines, so you should monitor rate moves as they affect project economics and refinancing risk.

- Mixed-use redevelopment and targeted hospitality and retail transactions demonstrate selectivity, not broad-based froth, so pickivity will matter going forward.

FAQ

Q: How do construction loans affect project timelines? A: Construction loans provide the capital to build, but draw schedules, covenants and rate resets can influence the speed of delivery and developer liquidity.

Q: Will updated MISMO standards change valuation outcomes? A: Standardized datasets like UAD 3.6 improve consistency in appraisals and procurement, which can reduce surprises and speed transaction closings.

Q: Should I worry about floating-rate financing today? A: Floating-rate debt exposes sponsors to short-term rate moves, so you should watch rate trends and hedging strategies that sponsors use to limit downside.