The Big Picture

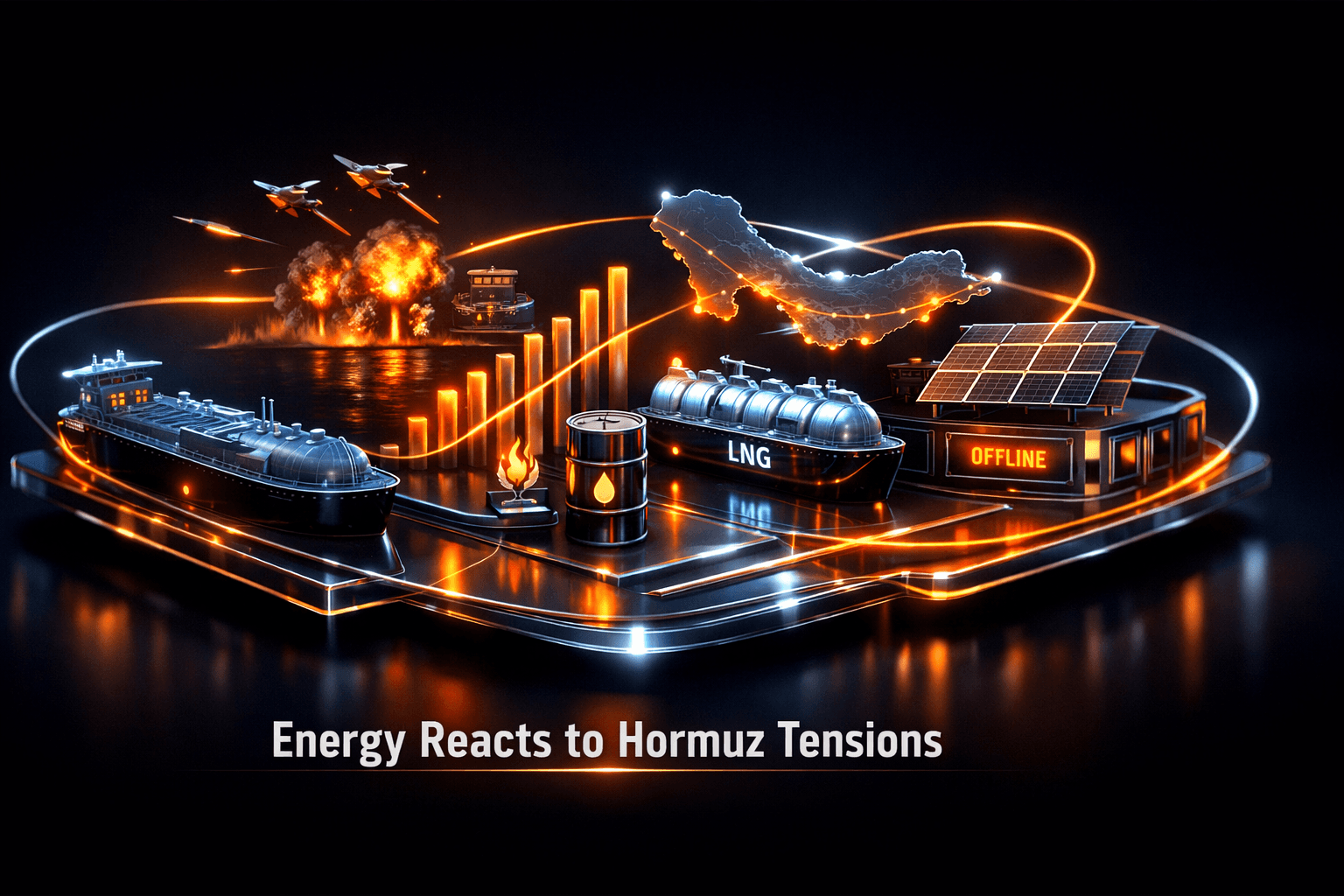

Overnight U.S.-Iran strikes around the Strait of Hormuz reignited a supply-risk premium across oil and gas markets, sending crude and European natural gas prices higher as vessel operators scrambled to avoid the chokepoint. That geopolitical shock remains the dominant driver for energy markets this morning, with immediate implications for commodity prices, shipping risk, and short-term revenue prospects for fossil fuel producers.

At the same time, the renewables chain showed mixed signals. France’s Reden halted solar module production, underscoring manufacturing pressure in Europe, while project tenders and material-technology advances pointed to continued demand for solar capacity. If you hold energy exposure, you’ll want to weigh the near-term upside from fossil fuels against structural challenges in parts of the clean-energy supply chain.

Market Highlights

Markets opened with a clear risk premium after weekend and overnight strikes. Here are the fast facts to scan this morning:

- Oil prices jumped on Monday after fresh U.S.-Iran strikes and renewed concerns over safe passage through the Strait of Hormuz, according to Rigzone reporting.

- European natural gas, Dutch TTF August 2026 futures, rose about 3.35% to $59.51 per MWh, opening roughly 3% higher as traders priced potential LNG shipment disruptions.

- Tanker traffic through the Strait of Hormuz collapsed to six vessels on Sunday, with operators switching transponders off to transit in so-called "dark mode," per Kpler data cited by Bloomberg and OilPrice.

- Renewables: French module maker Reden halted production at Roquefort-sur-Soulzon due to cost pressure and Asian competition, leaving Voltec as France’s only remaining PV panel producer, PV Magazine reports.

- Project pipeline: Türkiye will tender 900 MW of solar capacity on October 13, reflecting ongoing project-level demand in key markets.

- Technology note: KUKA Cable highlighted material innovation and long-term cable reliability at The smarter E Europe 2026, signaling attention to component durability in large-scale solar projects.

Key Developments

Hormuz escalation lifts oil and gas prices

Fresh strikes between the U.S. and Iran over the Strait of Hormuz over the weekend and into Monday have pushed oil prices higher as traders reassessed supply risk. Analysts quoted by Rigzone and OilPrice warn that further military action or interference with shipping could amplify volatility and disrupt flows of crude and LNG out of the Middle East.

For you, that means higher short-term prices can support upstream revenues and refining margins, but elevated geopolitical risk also raises downside volatility. What does this mean for energy equities and your portfolio in the near term?

Shipping disruption: tankers go dark

Operators again switched off Automatic Identification System transponders when transiting the Strait of Hormuz, a tactic that reduced visible traffic to six vessels on Sunday. Dark-mode transits increase insurance and operational risk and may raise freight and charter costs if disruptions persist.

Higher freight and insurance premiums typically filter back into spot fuel prices and can tighten physical supply availability regionally, so LNG and crude market balance could remain tight while the situation is unresolved.

Renewables: manufacturer setback, but project demand stays alive

Reden’s decision to halt module production at Roquefort-sur-Soulzon signals mounting cost pressure on European solar manufacturers and intensifying competition from Asian suppliers. That reduces domestic manufacturing capacity, and policy responses may follow.

Offsetting that, Türkiye’s 900 MW solar tender and industry focus on cable-material innovation suggest strong ongoing demand for new solar capacity and better reliability for long-term projects. Project developers and balance-of-system suppliers are likely to remain active, even if module manufacturing margins are under pressure.

What to Watch

Short term, monitor newsflow out of the Strait of Hormuz and statements from the U.S. and Iranian military or diplomatic channels. Escalation or de-escalation will drive price volatility and shipping behavior.

Watch energy price indicators and specific tickers for directional moves, including major integrated oil companies such as $XOM, $CVX, $SHEL, and $BP as prices rise. You’ll also want to track freight insurers and maritime security advisories, because rising premiums can feed into energy-market spreads.

On the renewables side, check for policy reactions in France or the EU after Reden’s shutdown, and follow Türkiye’s tender developments ahead of the October 13 deadline. Will governments step in to support local manufacturing, or will market forces push more sourcing to Asia?

Bottom Line

- Geopolitical risk in the Strait of Hormuz is the dominant market driver today, pushing crude and European gas prices higher and increasing shipping and insurance costs.

- Short-term price gains favor upstream and integrated oil companies, but they also increase volatility and downside risk if the situation deteriorates.

- Renewable manufacturing faces headwinds, illustrated by Reden’s production halt, yet project demand and technological improvements keep the solar pipeline active.

- Key near-term catalysts include further U.S.-Iran actions, shipping advisories, Türkiye’s October tender, and any EU or French policy measures to support local PV manufacturing.

- Data suggests selective exposure and active risk management are prudent, as the market balances a jump in fossil-fuel prices with structural challenges in parts of the clean-energy supply chain.

FAQ Section

Q: How will Strait of Hormuz tensions affect oil prices? A: Supply-risk premiums typically lift crude prices quickly when chokepoint security is threatened; continued escalation would likely sustain volatility and higher prices.

Q: Does Reden’s factory closure mean Europe will lose its solar pipeline? A: Not necessarily, production closures hurt domestic manufacturing but tenders, project demand, and technological improvements still support deployment, though sourcing may shift to non-European suppliers.

Q: What indicators should I track today? A: Monitor oil and TTF gas futures, shipping and insurance advisories for the Strait of Hormuz, official U.S. and Iranian statements, and updates on Türkiye’s tender timeline and EU manufacturing policy news.