Share this article

Spread the word on social media

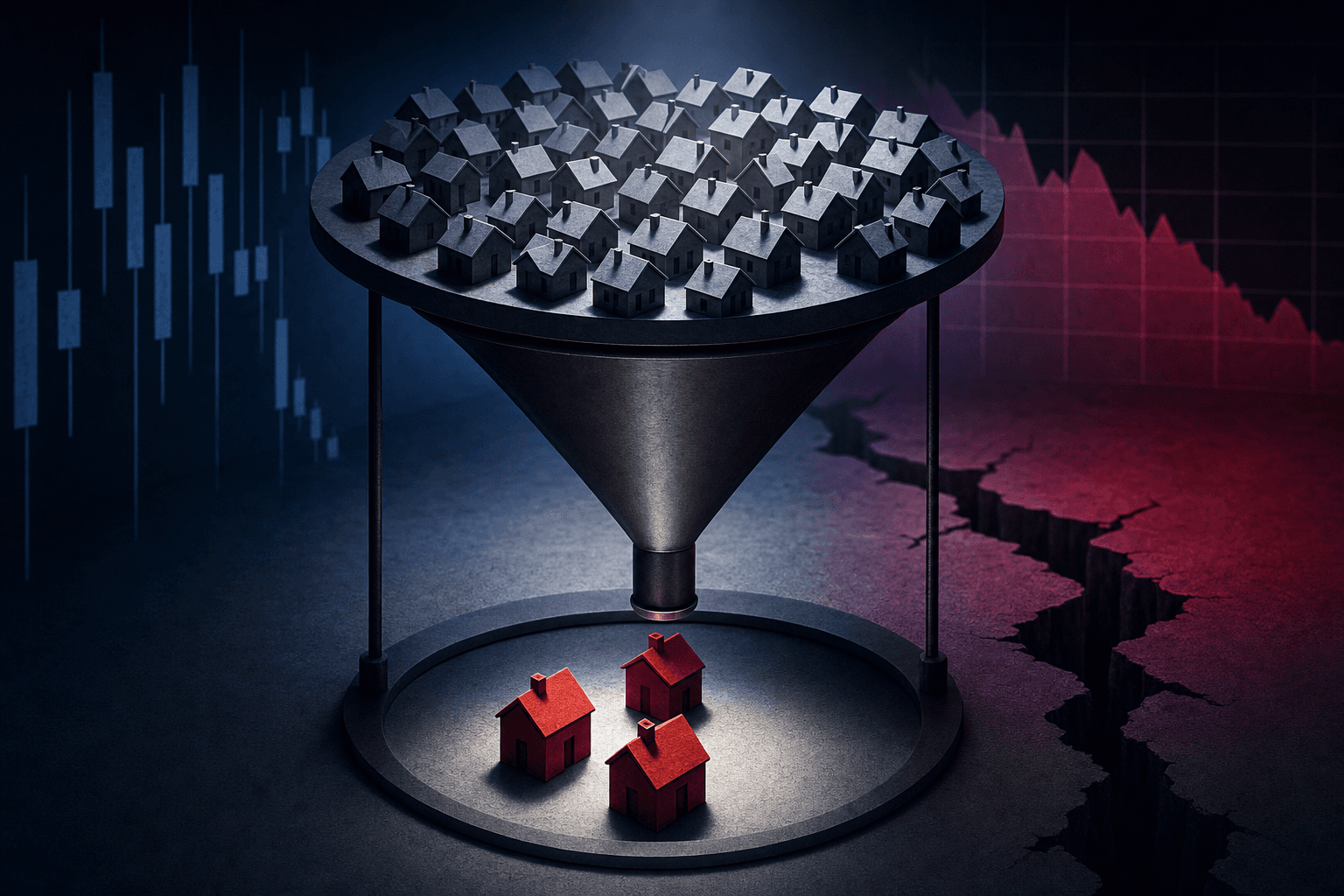

Opening hook: Homeownership costs jumped 39% and buyers are sidelined

Annual homeownership costs rose from about $20,000 in 2019 to more than $28,500 in 2025, a 39% increase that outpaced inflation. That single move has removed millions of potential buyers from the market and forced a reprice across related stocks.

Monthly housing costs that averaged $1,700 in 2019 now hover around $2,400, squeezing household budgets and demand.

What happened: Higher rates, record prices, and rising carrying costs

Mortgage rates rose into the high-6 percent to low-7 percent range by 2023 and remained elevated through 2025, cutting real purchasing power by a substantial amount versus the pre-spike era (estimates vary; reductions on the order of roughly 20 percent for a given monthly payment are plausible depending on assumptions). At the same time, many national home-price measures remained near record highs, keeping median prices elevated above $400,000 in many metros according to major indices.

Those forces combined with higher property taxes, insurance, utilities and maintenance to push the annual cost of ownership to $28,500 in 2025. The result has been a sluggish resale market, with existing-home sales below pre-pandemic levels in many months and inventory tight in many suburbs, producing months-long listing times in some areas.

Why it matters: Demand destruction, margin pressure, and a reallocation of capital

Less buyer demand does not only slow transaction volume, it changes pricing power. When prospective buyers drop out because monthly carrying costs exceed budgets, sellers reduce list prices or hold off, reducing turnover. Lower turnover cuts fee and origination volumes for banks and brokers, where mortgage originations can account for 10 percent or more of annual revenue for some firms in boom years.

Homebuilders face a two-front hit. New-home demand has a higher tolerance for price because buyers can lock rates and customize, but when entry-level monthly payments climb from $1,700 to $2,400 that market shrinks. Builders such as D.R. Horton (DHI) and Lennar (LEN) that rely on entry and move-up buyers see order books thin and cancellation rates tick higher, compressing margins; while some large builders reported net margins near or above 10% in stronger pre-2020 years, margins vary by firm and have been pressured recently.

Retailers and services tied to existing owners, like Home Depot (HD) and Lowe's (LOW), see mixed effects. Owners who stay put spend on repairs, driving near-term demand for tools and materials, but they cut discretionary renovations. Insurers and property-tax sensitive REITs face higher claims and revaluations, shifting cost structures into 2026.

The bull case: Structural shortages sustain prices and selective beneficiaries emerge

One bullish view notes chronic supply shortages. Permits and completions remain below historic demand in many coastal and Sun Belt metros, so prices can stay supported even as transactions fall. If mortgage rates retreat to the mid-5 percent range, a 10 to 15 percent rebound in affordability could unlock a wave of pent-up demand and re-accelerate activity.

Publicly traded companies tied to renovations, like HD and LOW, and mortgage rate-sensitive platforms such as Zillow Group (Z) could win if refinancing flows restart. Institutional buyers and single-family rental operators may also scoop up inventory, supporting REITs that target rental yield and giving a lift to specific names.

The bear case: Prolonged affordability gap and secular shift away from ownership

The downside is straightforward. If carrying costs stay 30 to 40 percent above where they were in 2019 in real terms, homeownership becomes materially less attainable for younger cohorts. That could depress home sales volumes for years and permanently shrink the addressable market for entry-level builders like KB Home (KBH) and NVR (NVR).

Higher default and credit stress among marginal owners is another risk. Emergency repair shocks and property tax reassessments can push previously solvent households into delinquency, raising loss expectations for mortgage lenders and originators such as Rocket Companies (RKT) and regional banks exposed to first-lien originations.

What This Means for Investors: Reposition, hedge, and watch four signals

Investors should treat the housing complex as a bifurcated trade. Favor companies with recurring revenue or pricing power that benefits from owners who stay put. Avoid high-exposure builders and small lenders that depend on volume to cover narrow margins.

Watch these four signals closely. First, the 30-year fixed mortgage rate level, where a move below 5.5 percent materially increases buying power. Second, existing-home sales and months-supply, where a return to the 5 to 6 months range would signal normalization. Third, new-home cancellations and orders at DHI and LEN, which give real-time demand data. Fourth, mortgage refinance volume and originations at Rocket (RKT) and JPMorgan Chase (JPM).

- Long ideas: HD, LOW, REITs targeting rentals (select exposure), insurance carriers with solid combined ratios.

- Short/avoid: Volume-dependent builders such as KBH and NVR during a prolonged affordability squeeze, small regional mortgage banks without hedge programs.

Stocks to monitor: DHI, LEN, HD, LOW, RKT, Z, RDFN, NVR. Each name offers a different exposure to construction, renovation, origination, and platform flows.

Investor takeaway

Rising homeownership costs have already reduced buyer participation, cutting transaction volumes and reassigning profits across the housing supply chain. Position for lower volumes but selective winners: maintenance and retail for homeowners who stay put, institutional buyers of rental assets, and mortgage platforms that can capture digital market share when rates normalize. If the 30-year rate slips below 5.5 percent, re-evaluate builder exposure quickly, because affordability can rebound fast and create upside for volume-sensitive names.