The Big Picture

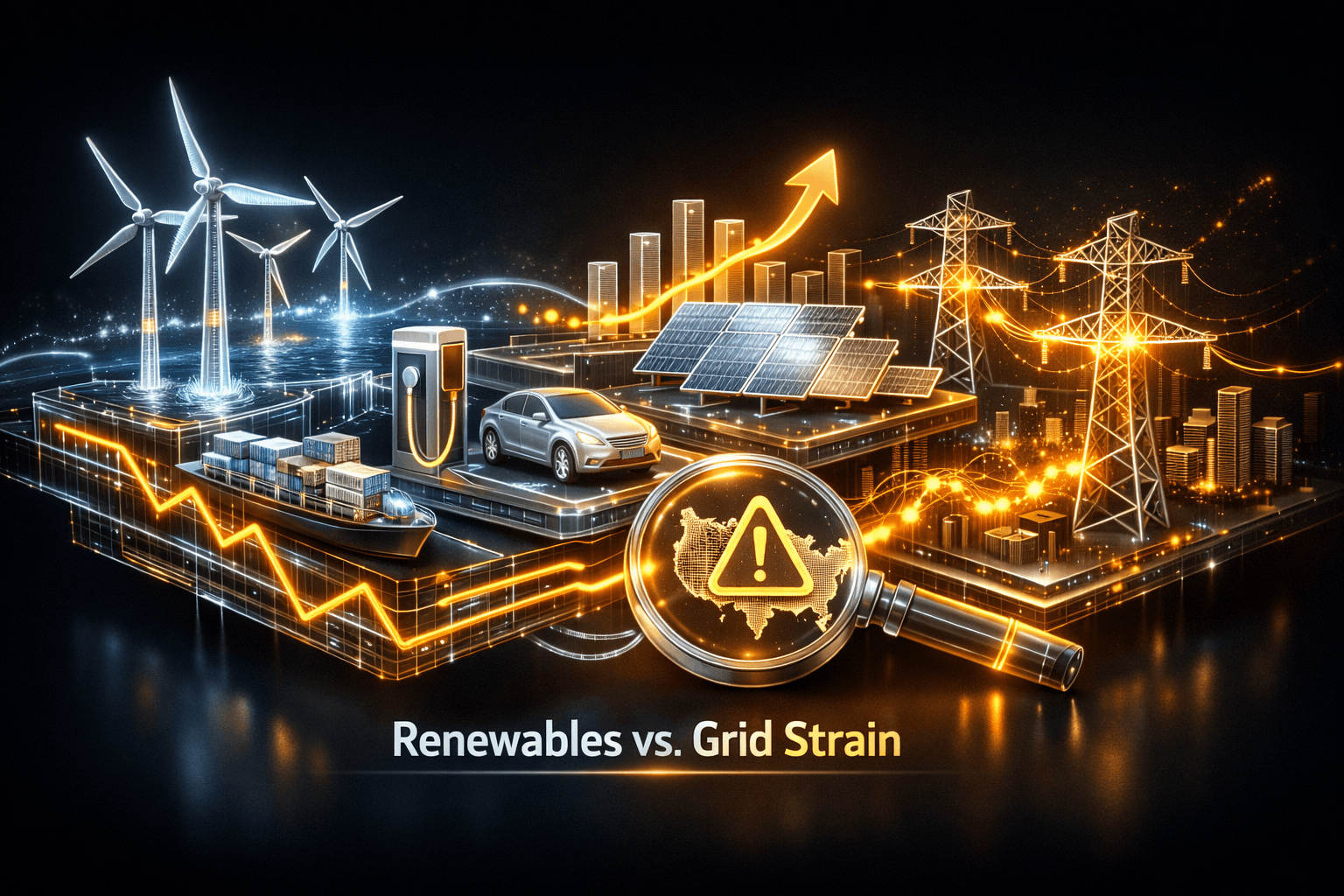

Offshore wind, electric mobility and utility-scale solar keep pushing the energy transition forward, but emerging demand from AI data centers and trade and workforce frictions are forcing utilities to rethink plans. You should know that the story is not one-way; growth opportunities exist alongside mounting reliability and policy challenges.

Markets were closed Saturday, July 18. These stories were reported over the past 24 to 48 hours, with the last U.S. trading session on Friday, July 17, and the next session opening Monday, July 20. Read on to see what matters to you heading into the long weekend.

Market Highlights

Here are the quick facts and takeaways from the week and the most recent reports. Note that price and percentage references are tied to the last trading day, Friday, July 17, when relevant.

- Offshore wind tech advances: New large-construction vessels from China are driving down costs and enabling supersized turbines, a development noted in coverage of global offshore wind expansion.

- EV logistics pilots expand: JRS Express and Voltai began a battery-swap scooter pilot in Metro Manila, highlighting practical electrification in last-mile delivery.

- Solar sector moves: ARRAY Technologies, the solar tracker company $ARRY, announced an acquisition of Affordable Wire Management to broaden balance-of-system offerings.

- Policy and trade watch: The U.S. Commerce Department opened a probe into silicon solar cells from Ethiopia for potential circumvention of AD/CVD duties on Chinese-made cells.

- Grid capacity alert: Bank of America projects data center demand could outpace planned utility additions by more than 100 GW through 2030, increasing reliance on on-site gas generation and battery storage.

Key Developments

Offshore wind and global supply-chain advances

CleanTechnica highlighted a new Made-in-China offshore construction vessel that can handle supersized turbines while cutting costs. That combination of larger turbines and lower installation costs could accelerate offshore deployment globally, and it may change project economics for developers and utilities procuring offshore power.

For you as an investor, the implication is clear. Technology-driven cost declines can boost project pipelines and margins, but they also intensify competition and pressure on firms that lag in scale or manufacturing partnerships. Who can scale and who gets left behind will separate the wheat from the chaff.

EV adoption at scale and practical pilots

Two stories out of Asia show demand-side electrification pushing forward. In the Philippines, JRS Express and Voltai launched a pilot for battery-swapping scooters in Metro Manila. In New Delhi, new air-quality driven EV incentives aim to speed vehicle retirement and replacement.

These are incremental but practical moves that will raise electricity consumption patterns and distribution needs in dense urban areas. If you follow utilities with significant urban grids or municipal partnerships, these pilots are early signals of load growth and local infrastructure requirements.

Grid capacity, AI data centers and regulatory friction

Bank of America analysts told Utility Dive that forecasted data center demand could exceed planned utility capacity additions by more than 100 GW through 2030. That gap points to greater reliance on behind-the-meter gas, battery storage and potentially new transmission builds to maintain reliability.

At the same time, FERC flagged concerns after PJM capacity auction results and asked regional operators to report on seams and reliability. Regulators and planners will be under pressure to reconcile rapid demand pockets with orderly resource procurement.

Solar supply chain and industrial consolidation

The Commerce Department opened an inquiry into Ethiopian solar cell imports for possible circumvention of duties on Chinese cells. That probe introduces near-term policy risk for module supply chains and could affect pricing and procurement timelines in U.S. projects.

On the corporate side, $ARRY is acquiring Affordable Wire Management to expand balance-of-system solutions, a move that suggests supply-chain vertical integration and margin diversification are top of mind for solar suppliers as they chase utility-scale projects.

What to Watch

Expect a tug of war between load growth and grid investment. Will utilities secure the capital and permitting needed to add capacity at the pace AI and electrification demand? Regulatory deadlines and regional auction results will matter a great deal for near-term planning.

Track these specific catalysts and risks going into next week and beyond. First, FERC and regional operator filings on PJM, CAISO and SPP seams and capacity will be important. Second, watch the Commerce Department investigation into Ethiopian cells for potential trade remedies or import restrictions. Third, monitor utility and developer announcements on offshore wind contracts and vessel deployments that could shift project timelines.

Operational risks include workforce constraints. The solar industry reported more than 280,000 workers in 2024 and solar-plus-storage employment over 460,000, yet training shortfalls persist. That gap could delay project builds and increase costs if it is not addressed.

Bottom Line

- Renewable deployment keeps gaining momentum thanks to technology and modular business models, but growth is increasingly constrained by grid capacity and permitting timelines.

- Policy and trade uncertainty is real, with a new U.S. probe into Ethiopian solar cells that could affect module supply and pricing.

- Data center and AI load growth is a material demand shock that could force more on-site generation and storage, and regulators are already sounding the alarm.

- Corporate consolidation and supply-chain plays, like $ARRY's acquisition, signal industry participants are trying to lock in margins and service offerings.

- Be selective, watch regulatory filings and project timelines, and consider network and workforce constraints when you evaluate utility and clean-energy exposure.

FAQ Section

Q: How will AI data-center growth affect utility planning? A: Data-center demand could add more than 100 GW by 2030 relative to planned capacity, pushing utilities toward more battery storage, on-site gas generation and accelerated transmission planning.

Q: What does the U.S. probe into Ethiopian solar cells mean for projects? A: The Commerce Department inquiry could lead to tariffs or import limits if circumvention is found, creating short-term supply uncertainty and potential price pressure for modules used in U.S. projects.

Q: Are offshore wind cost declines a near-term win for U.S. utilities? A: Technology and vessel advances are lowering global offshore costs and can improve project economics, but U.S. deployment still faces permitting, grid interconnection and local supply-chain hurdles before large near-term impacts materialize.