The Big Picture

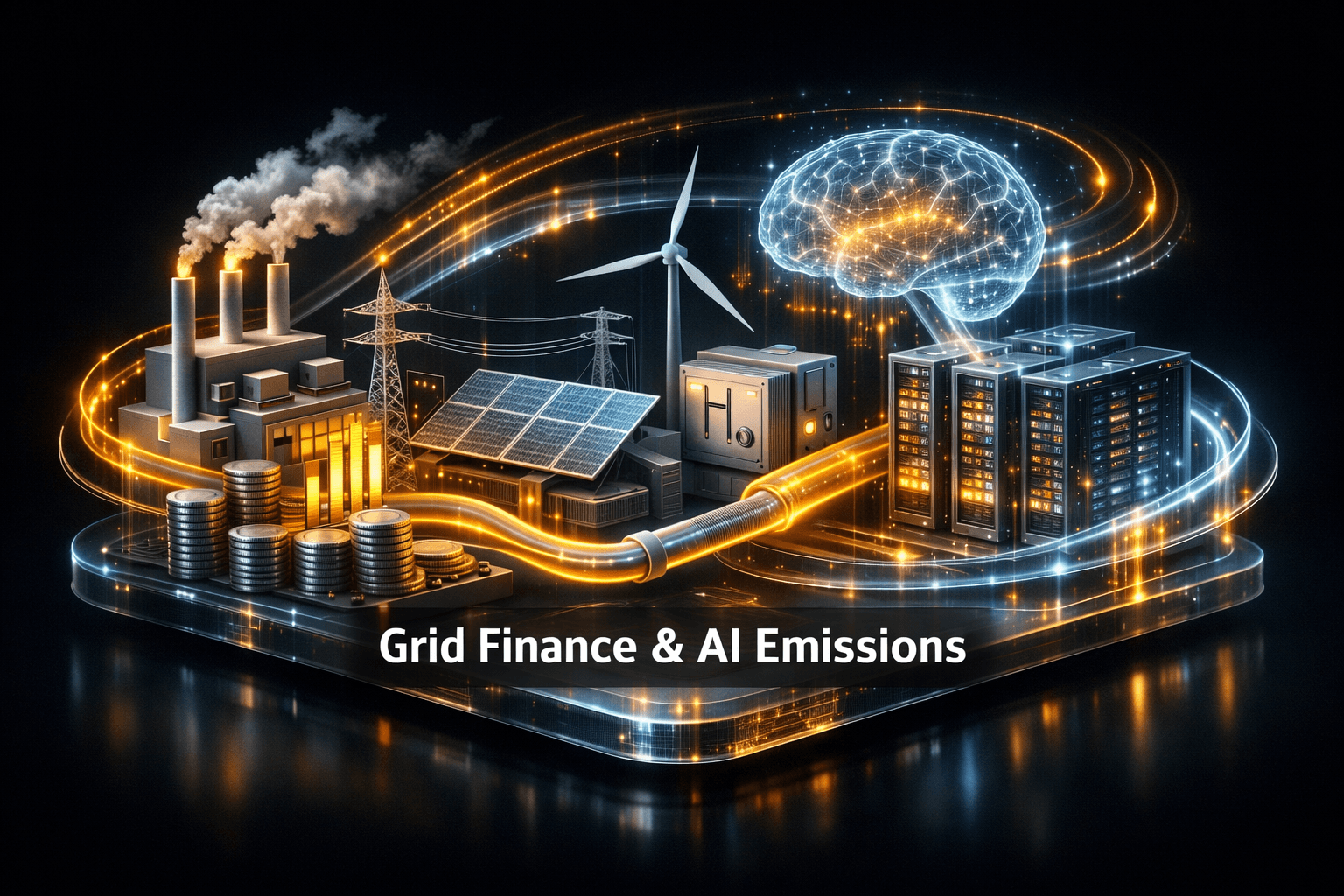

Big dollar flows and big emissions sit side by side in this morning’s utilities headlines. Federal and private financing is accelerating transmission, solar-plus-storage, and onsite power for data centers, even as new reports highlight a jump in CO2 tied to AI-driven data center growth.

This matters because you’re seeing the two forces that will shape utility company strategy and regulatory scrutiny over the next several years: heavy investment in grid capacity and clean tech, and mounting pressure over carbon footprints as compute demand soars.

Market Highlights

Key numbers and quick facts to start your trading day and research list.

- DOE closed a loan of up to $3.26 billion to AEP Texas to fund nearly 100 transmission projects and roughly 2,800 miles of lines, the largest single transmission financing in recent federal actions, tied to $AEP.

- Avantus secured more than $525 million in construction financing for the Aratina 2 Solar and Storage Project in California, a major solar-plus-storage raise to accelerate capacity buildout.

- Brookfield and Bloom Energy expanded a funding framework to $25 billion to support onsite data center power and fuel cell deployment, a large corporate financing signal for $BAM and $BE.

- New project proposals include the $3.2 billion, 932-MW Greenlight Electricity Centre gas plant in Alberta, aimed at serving a major data center development.

- Environmental and policy figures: Ember reports Drax emitted 14.1 million tonnes CO2e in 2025 while receiving £999m in subsidies. The Energy Institute notes the U.S. accounted for nearly 50% of global CO2 emissions growth in 2025, driven largely by AI data centers.

- Distributed energy milestones: New York reached 8 GW of distributed solar capacity, and Polestar recorded 30,423 vehicle sales for H1 2026, signaling sustained EV demand that affects long-term electricity load, relevant to $PSNY.

Key Developments

Massive financing for grid and storage

The DOE’s $3.26 billion closed loan to AEP Texas is designed to rebuild, reconductor, and add new transmission lines across several states. That federal backing reduces financing risk for large-scale grid upgrades and could accelerate interconnection for renewables.

At the same time Avantus’ $525 million project finance for Aratina 2 shows private capital is still flowing into utility-scale solar-plus-storage. For you, that means developers and equipment suppliers may see more stable project pipelines in the near term.

AI data centers reshape demand and emissions

Multiple stories tie AI infrastructure to rapid shifts in power demand and emissions. The Energy Institute’s review highlights the U.S. share of 2025 emissions growth at nearly 50 percent, and several project announcements explicitly serve data center clusters.

Brookfield and Bloom Energy’s $25 billion framework, and the planned Alberta gas plant, underline a pragmatic response: companies and utilities are racing to secure reliable onsite or grid power for compute loads, even if that means adding gas-fired capacity in some regions.

Distributed solar, edge compute pilots, and corporate deals

Sunrun launched a distributed AI compute pilot that leverages home solar-plus-storage systems to provide edge compute capacity. That’s an innovation pivot for residential renewables and it could help monetize behind-the-meter assets for $RUN.

Meanwhile, New York’s 8 GW distributed solar milestone shows policy and interconnection improvements can unlock rooftop and community solar growth. The combination of distributed resources and corporate onsite power deals is changing how utilities plan capacity and manage load.

What to Watch

Look ahead to these catalysts and risks that could move utilities stocks and project valuations this quarter.

- Regulatory scrutiny and emissions reporting. With the Energy Institute and Ember findings, regulators and ESG-focused capital may increase pressure on utilities and generators to disclose and mitigate emissions. How will companies respond to tighter permitting or subsidy reforms?

- Transmission build timelines and interconnection queues. The AEP loan should speed some projects, but construction timelines and permitting remain risks. You should track milestone filings and regional grid operator notices for capacity additions.

- Data center power deals and technology choices. Watch firms like $BE, $BAM, and project developers for deal announcements that clarify whether fuel cells, gas peakers, or storage will dominate onsite solutions.

- Policy and job impacts from OBBBA. The E2 analysis claims the administration’s One Big Beautiful Bill Act cut nearly 500,000 clean energy jobs; legislative or administrative responses could alter incentives and project economics.

- Distributed energy adoption and utility rate design. As New York, Sunrun pilots, and other deployments scale, utilities will need clearer rate structures and interconnection processes. That’s both an opportunity and a source of short-term friction for you to monitor.

Which metrics should you track first? Keep an eye on quarterly project announcements, regulatory filings, and any emissions or ESG disclosure updates from major utilities, because those will signal how the tradeoffs between reliability and decarbonization are being managed.

Bottom Line

- Federal and private financing is accelerating grid upgrades and large-scale storage, improving project pipelines for developers and suppliers.

- AI-driven data center demand is creating new load centers, prompting both clean and fossil-fuel solutions and raising emissions concerns.

- Distributed solar and edge compute pilots are expanding revenue models for residential and commercial players, pressuring utilities to modernize interconnection and rate design.

- Policy and subsidy debates remain a major risk, and emissions data will shape investor and regulatory responses in the coming months.

- For now, the sector shows mixed signals, so exercise selectivity and watch near-term catalysts rather than assuming a one-way trend.

FAQ Section

Q: How will the DOE loan to AEP Texas affect transmission buildout timelines? A: The $3.26 billion loan reduces financing hurdles and should speed procurement and construction, but permitting and siting still determine exact timelines.

Q: Do data center power deals mean more gas plants will be built? A: Some data center projects rely on flexible gas for reliability, while others will use fuel cells, storage, or onsite renewables; expect a mixed buildout depending on local policy and market economics.

Q: Should I expect faster rooftop solar growth after New York reached 8 GW? A: Policy improvements and reduced soft costs that New York used are replicable, so other states may see accelerated distributed solar if they adopt similar steps.