The Big Picture

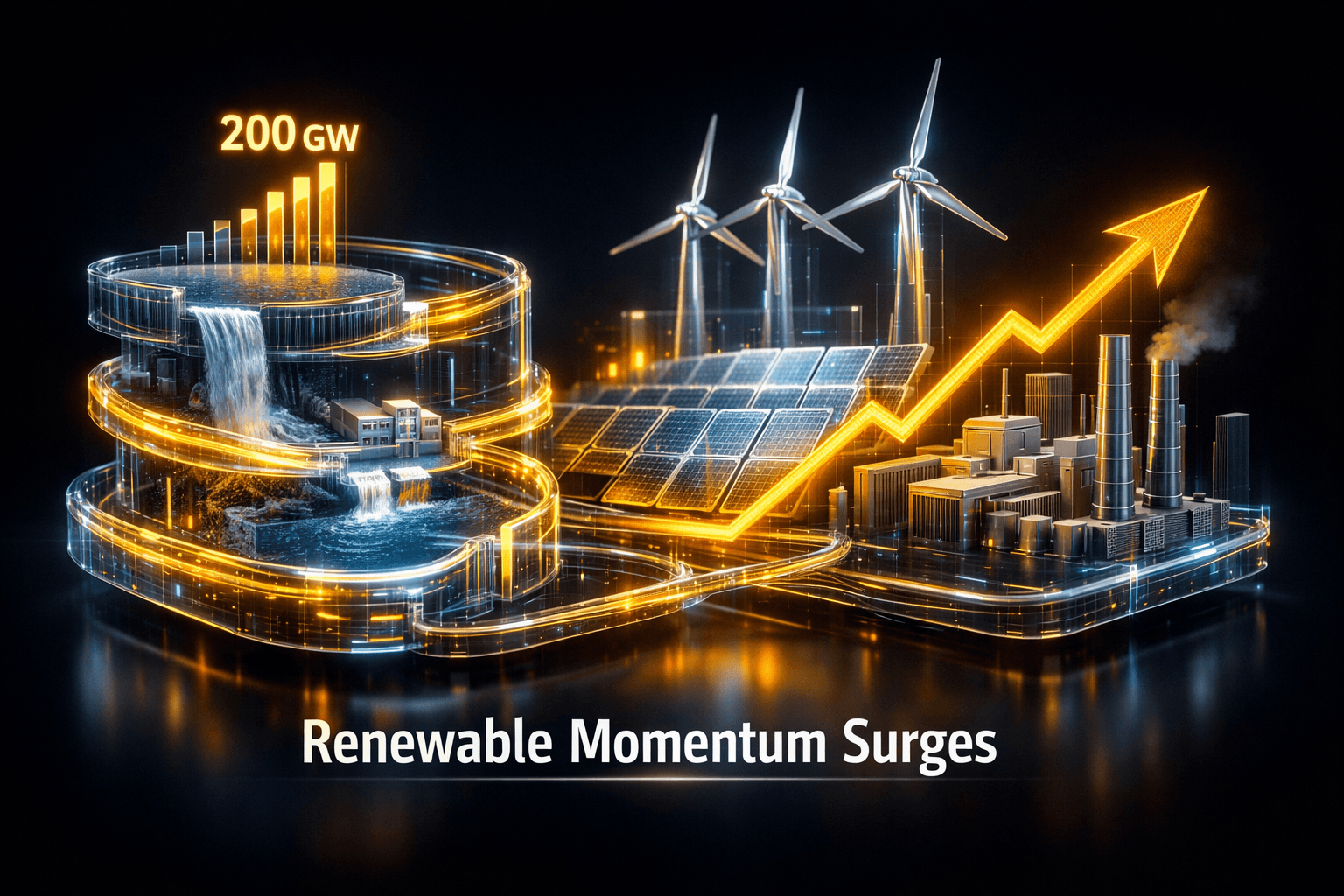

Renewables and flexible resources are taking center stage in the utilities sector, and the pace feels meaningful rather than incremental. From pumped storage topping 200 GW to small-scale solar shaving midday demand in New York, multiple reports released over the last 24 hours suggest a structural shift in supply and demand dynamics that investors need to follow as you plan for the coming months.

That momentum comes with tradeoffs, because grid operators are also reporting more conventional generation outages. What does that mean for your exposure to utilities and clean energy names heading into the long weekend? Read on for the developments that matter most, and items to watch when markets reopen as of Friday, June 26.

Market Highlights

Quick facts and figures from the latest coverage, useful if you want a rapid checkpoint before digging deeper.

- UK EV milestone: For the first time, new electric vehicles outsold petrol cars over a 12-month span in the UK, signaling consumer shift and charging demand growth.

- Solar growth: EIA-reviewed data shows renewables generation rose more than 10% in the first third of 2026, and utility-scale additions projected to add over 78.5 GW, with solar poised to surpass US natural gas capacity in 2027.

- Pumped storage capacity: The International Hydropower Association reports global pumped storage capacity topped 200 GW after a record year for new builds.

- Virtual power plants: New partnerships aim to unlock more than 16 GW of VPP capacity without new build, improving flexibility and resource aggregation.

- Grid strain: NERC warns conventional generation outages rose in 2025, with coal and some combined-cycle availability weakening and inverter-based resources adding operating variables.

- Commercial innovation: OpSun launched the SunRail Inverter Rack for rooftop commercial solar, and BYD is set to launch the new Seal 08 next week, a product news item that ties into EV charging demand forecasts.

Key Developments

Renewables and storage scale up, changing midday and peak dynamics

Small-scale solar in the New York ISO is already reducing metered midday demand in spring months, and national data points to double-digit renewables growth year to date. At the same time, pumped storage additions pushed global capacity past 200 GW, which supports longer-duration flexibility for seasonal swings. For you, that means afternoon duck curves are getting flatter in some regions, and storage plus VPPs can shift where and when value is earned on the grid.

Virtual power plants and grid flexibility move from pilot to scale

Planned VPP capacity above 16 GW, achieved through partnerships and aggregation, shows a shift from pilot projects to operational scale. VPPs that leverage distributed assets can provide non-wires alternatives and ancillary services, which reduces the need for new thermal peaker plants. If you're tracking utility capital allocation or service providers, watch which names win contracts to aggregate customer-sited resources.

Reliability pressures amid changing generation mix

NERC's report that conventional generation outages rose in 2025 is a clear cautionary note. As coal and some gas combined-cycle units show weaker availability, grid operators face a more systemwide reliability challenge while integrating inverter-based resources. That increases the premium on flexible capacity, transmission upgrades and firm low-carbon dispatchable resources such as pumped storage and geothermal.

What to Watch

Here are the forward-looking items that could move utility fundamentals or sentiment when markets reopen on Monday, June 29.

- Policy and regulation: The UK ZEV mandate debate could affect EV rollout timelines and charging infrastructure demand in Europe. Will regulators preserve or water down zero-emission targets?

- Project announcements and deals: Look for news on VPP partnerships scaling beyond the initial 16 GW and for pumped storage and battery procurement wins by utilities and developers.

- Grid reliability signals: Monitor NERC briefings, reserve margins and outage notices. Rising conventional outages increase value for fast-response storage and firm renewables.

- Commercial adoption: Data center flexibility negotiations could set operating rules that affect peak demand profiles. Watch announcements involving hyperscalers, utilities, and interconnection frameworks.

- Company product and launch events: BYD's Seal 08 launch and OpSun's new inverter rack are product-level cues that affect EV charging patterns and commercial rooftop project economics.

Want to prioritize your reading? Start with upcoming regulatory hearings and any Monday announcements on VPP contracts or pumped storage procurement.

Bottom Line

- Renewable capacity and distributed solar are reshaping midday load, and storage scale-up is following behind to manage variability.

- Pumped storage surpassing 200 GW and projected solar additions through 2027 point to structural growth drivers for flexibility assets.

- NERC's reliability warning means investors and utilities alike will focus more on dispatchable and fast-response resources.

- EV adoption milestones in the UK and new EV models like the BYD Seal 08 add to long-term electrification demand for utilities and charging infrastructure providers.

- Watch policy outcomes, large VPP contract wins, and grid operator notices for the next clear signals on capital flows and operational risk.

FAQ Section

Q: How will more small-scale solar affect utility revenues? A: Small-scale solar reduces midday metered sales and can compress margins on volumetric sales, but it also creates opportunities for utilities to offer grid services, aggregation, and distributed energy resource management.

Q: Should I be worried about NERC's report on outages? A: The report signals increased operational complexity, not imminent collapse. It suggests you should monitor reserve margins, outage trends and investments in flexibility and transmission upgrades.

Q: What does the UK EV milestone mean for US utilities? A: The UK milestone is a leading indicator of electrification trends and charging demand growth. For US utilities, it highlights potential load growth, new infrastructure needs and opportunities for managed charging programs.