The Big Picture

Utilities and the broader power sector got a clear vote of confidence overnight as financing, corporate offtakes and product rollouts accelerated deployment. Major financing for utility-scale solar and battery storage, plus milestones from manufacturers and grid operators, are nudging the industry from pilot phase into steady scale-up.

That matters to you because project-level capital, technology reliability and grid integration are the levers that convert policy and demand into revenue for developers, manufacturers and utilities. The ball is rolling, and today you should watch how public names tied to these stories react in early trading.

Market Highlights

Quick facts and numbers to scan before the open.

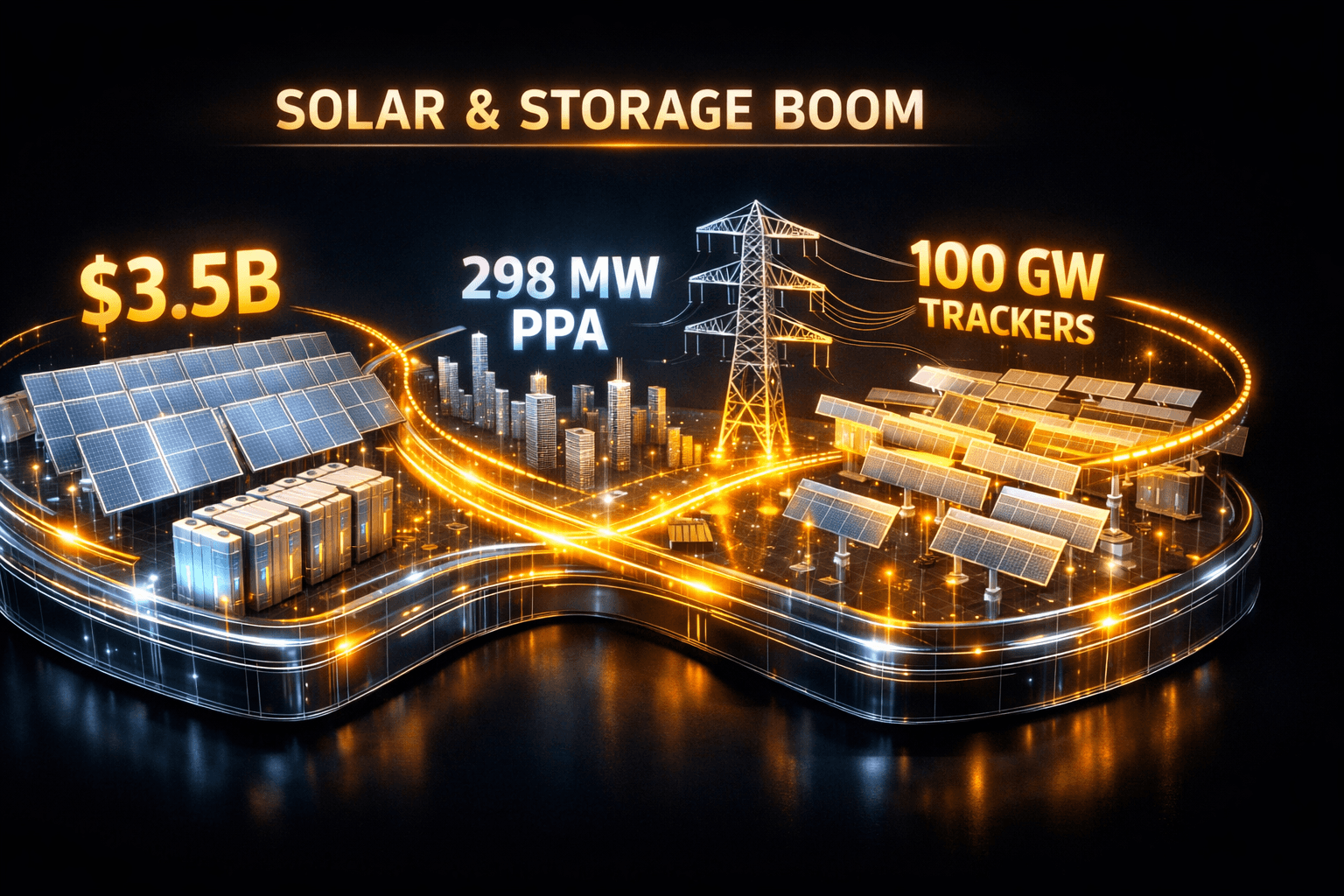

- Cypress Creek Energy closed $3.5 billion to build the first two phases of the Steel River Energy Center in Arkansas, a major utility-scale solar and storage play.

- RWE secured a long-term corporate PPA with Meta for the 298 MWAC Rabbit's Foot Solar project in northeast Texas, linking a major generator to a hyperscaler buyer.

- ARRAY Technologies said it has shipped 100 GW of solar trackers globally since founding, underscoring scale in solar balance-of-system supply, cited by $ARRY.

- PG&E reported more than 1 million customers have connected solar to its grid, a milestone for distributed resources and two-way grid dynamics, relevant to $PCG.

- Trina’s 620 W Vertex N Shield panel, now available in North America, offers 23% efficiency and hail resistance for harsh-weather sites.

Key Developments

Big project finance and corporate offtake

Cypress Creek’s $3.5 billion close for Steel River’s first phases signals robust capital flows into combined solar and battery storage. Corporate demand remains visible as RWE’s PPA with Meta for a 298 MWAC project ties generation to a large, long-duration buyer, illustrating how developer and corporate buyers are partnering to de-risk projects.

For you, that means more shovel-ready projects and clearer revenue streams for developers and utilities that host or interconnect plants. Watch construction and interconnection timelines closely, since delays are the main short-term execution risk.

Manufacturers and product scale

Hardware milestones matter for project economics. ARRAY’s 100 GW of shipped trackers shows manufacturing scale in racking, which can lower installation costs. Trina’s Vertex N Shield panel adds a 620 W, 23% efficient, hail-resistant option to North American supply chains, which helps lower levelized cost of energy for sites prone to severe weather.

These developments suggest supply-side improvements that could compress capital intensity per megawatt. If you follow module and tracker suppliers your focus should be on delivery schedules and warranty terms.

Grid integration, EVs and strategic M&A

PG&E surpassing 1 million connected solar customers highlights the shift to interactive grids where distributed resources matter. General Motors is pushing utilities to explore vehicle-to-grid, while also investing in sodium-ion for grid storage, signaling automakers’ growing role in grid services. These trends support a longer-term need for flexible capacity and two-way energy flows.

Corporate M&A also featured as MiCo’s HPS unit agreed to buy NEM Energy, a heat-recovery steam generator specialist. That deal broadens capabilities for utility-scale thermal and combined-cycle projects, which could be relevant to developers and OEM suppliers looking for integrated solutions.

What to Watch

Here are the catalysts and risks to monitor through the day and coming weeks.

- Project execution and interconnection: watch updates on construction milestones for Cypress Creek and the Rabbit's Foot project. Delays can affect cashflows and offtake start dates.

- Permitting and supply chain: module and tracker deliveries, and any reported bottlenecks for inverters and transformers, will influence near-term project timelines.

- Grid operations: PG&E’s integration experience is a signal for other utilities. Monitor filings on interconnection queue reforms and tariff changes that could alter project economics.

- EV-grid integration: follow statements from $GM and major utilities about pilots or incentives for vehicle-to-grid aggregation. Could V2G pilots scale into firm capacity offerings?

- M&A integration: watch HPS and NEM Energy integration plans, and any guidance on combined order books or service contracts that could change revenue mix.

Bottom Line

- Capital is flowing into large solar plus storage projects, shown by a $3.5B financing and long-term PPAs, which strengthens project pipelines.

- Supply-side scale from ARRAY and product rollouts from Trina help lower installation costs and improve resilience for harsh climates.

- Distributed resources are mainstream, with PG&E’s 1M connected customers showing the grid is increasingly interactive.

- EVs and V2G initiatives from automakers add a new grid resource that utilities and developers will need to plan for.

- Keep an eye on execution risks, interconnection delays, and policy changes that could shift project timelines and returns.

FAQ Section

Q: How will the $3.5B Cypress Creek financing affect project timelines? A: The financing should speed construction and lock in long-term financing, but timelines still depend on equipment deliveries and interconnection approvals.

Q: Does PG&E’s 1M solar connections mean the grid is ready for two-way power? A: It shows progress toward an interactive grid, but utilities still face challenges with voltage control, inverter settings and interconnection queue management.

Q: Will vehicle-to-grid (V2G) meaningfully change utility capacity needs? A: V2G could provide distributed flexibility if pilots scale and aggregators form viable markets, but commercial adoption depends on standards, compensation and battery degradation models.