The Big Picture

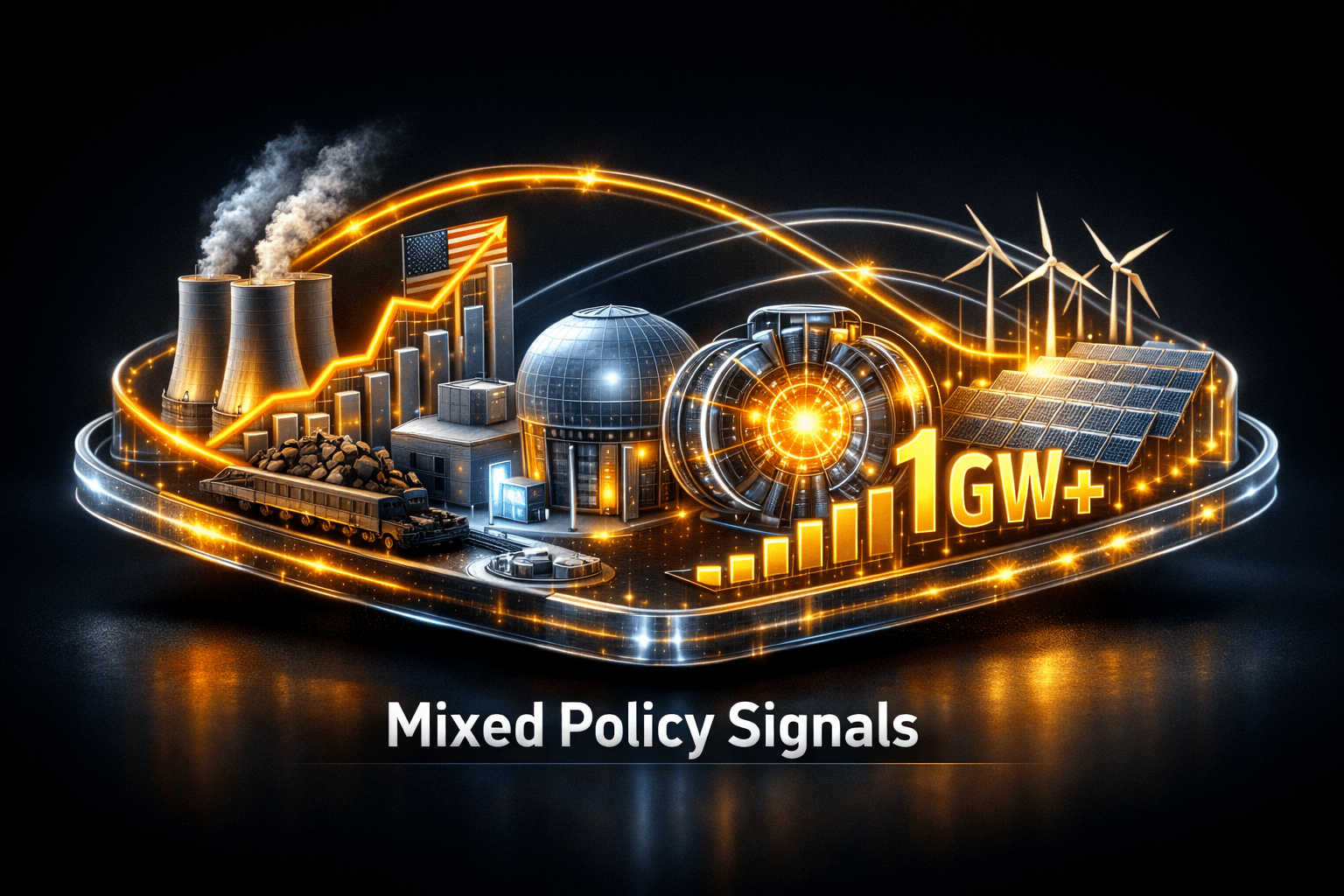

Heading into the long weekend, the utilities sector is sending mixed signals. Federal moves to shore up coal capacity and keep units online have collided with technical progress at advanced nuclear, fusion research, large-scale renewables plus storage projects and rising electrification demand.

That mix matters for your portfolio because it affects fuel risk, regulatory exposure and near-term grid reliability. Markets were closed Saturday, June 6, so price reactions are referenced as of Friday, June 5.

Market Highlights

Quick facts and figures from the top stories that will influence utility strategies and investor attention.

- Federal coal support: reporting highlights a new roughly $700 million subsidy for existing coal and a separate $850 million program to modernize coal capacity and build two new U.S. coal plants totaling about 2.85 GW.

- Coal dispatch and reliability: DOE ordered Orlando Utilities Commission's 465-MW coal unit to remain online, citing data center reliability needs in Florida.

- Advanced energy milestones: Antares Mark-0 achieved zero-power criticality under DOE’s Reactor Pilot Program, and Commonwealth Fusion Systems published five peer-reviewed physics papers validating ARC fusion work.

- Large-scale integrated projects: Google and Intersect launched the Meitner Energy Center, a co-located 1 GW-plus wind, solar and battery plus on-site gas complex in the Texas Panhandle, with $GOOGL involved through its recent acquisition.

- Electrification demand: Plug-in EVs reached a 33.0% share of new vehicle registrations in France in Q1 2026, up from 22.9% in Q1 2025; BEV share grew sharply while overall auto volume was down about 2.5% year over year.

- Biofuels pressure: A T&E study cited in reporting projects biofuel consumption could rise about 30% this year and approach a 70% increase by 2030, a dynamic that could press food and fertilizer markets.

Key Developments

Federal push for coal and short-term reliability

Policy announcements this week include a roughly $700 million subsidy for existing coal assets and an $850 million push to modernize coal and build two new plants in Anchorage and West Virginia totaling about 2.85 GW. The DOE also directed a 465-MW OUC coal unit in Florida to keep running, partly to help serve potential data center load.

For investors, that means near-term demand for thermal fuel and capacity services may stay elevated, and regulated utilities or merchant generators with coal exposure could see policy-driven cash flow support. But these moves add regulatory risk to clean energy planning and can shift capacity markets.

Advanced nuclear and fusion make tangible progress

Technical milestones are stacking up for non-fossil firming sources. Antares Nuclear’s Mark-0 microreactor reached zero-power criticality at INL under the DOE Reactor Pilot Program. Commonwealth Fusion Systems published five peer-reviewed papers supporting its ARC fusion physics basis.

These developments don't produce immediate revenue for public utilities, but they strengthen the long-term technology pipeline for reliable, low-carbon firm power. If these technologies scale, they could reshape planning assumptions over the next decade.

Renewables growth, integration projects and bottlenecks

Google and Intersect broke ground on the Meitner Energy Center in the Texas Panhandle, planning more than 1 GW of co-located wind, solar and battery storage with on-site gas for firming. Meanwhile EV penetration in France climbed to a 33.0% share in Q1, signaling rising electrification demand globally.

Still, project success depends on transmission and interconnection. Jefferies flagged transmission constraints for geothermal developer Fervo Energy in the West, showing that generation growth can be hamstrung by grid limits. So you should weigh project pipe dreams against realistic interconnection timelines.

What to Watch

Monitoring these variables will help you judge sector direction and company exposures over the summer.

- Policy shifts and funding rolls: watch departmental rulemaking and how the $850 million coal program is allocated, plus any state-level responses that affect renewables permitting.

- Transmission and interconnection updates: pay attention to regional transmission operators and any backlog relief measures. Can the grid absorb new generation at scale without major upgrades?

- Advanced tech milestones: follow operational tests for Antares and any roadmap updates from fusion groups; incremental technical wins can alter long-term capacity forecasts.

- Demand drivers: track EV adoption and large data center projects like Google’s Meitner center, which will increase localized demand and create new offtake patterns.

- Supply pressures from biofuels: rising biofuel use may push fuel costs and agricultural inputs, with knock-on effects for utilities that rely on biomass or municipal solid waste contracts.

Bottom Line

- Policy and reliability concerns are temporarily boosting coal and firming capacity, complicating the clean transition picture for utilities.

- Technical progress in microreactors and fusion is encouraging, but these remain multiyear plays rather than immediate replacements for thermal capacity.

- Large integrated projects and rising EV adoption point to growing long-term electricity demand, but grid bottlenecks are a real constraint you should watch closely.

- Expect selective opportunities, and keep an eye on regulatory decisions and transmission funding as catalysts that will sort winners from laggards.

FAQ

Q: How will federal coal funding affect clean energy investment? A: The funding shifts near-term economics toward keeping or modernizing coal capacity, which can slow retirements but does not remove longer-term incentives and mandates for clean energy expansion.

Q: Should I expect quicker adoption of advanced nuclear or fusion? A: Progress is meaningful, with Antares reaching criticality and fusion papers published, but commercial deployment timelines remain multi-year and depend on demonstration success and supply chains.

Q: What major risks should I watch in the next three months? A: Watch transmission backlog developments, DOE policy allocations, fuel price moves and any state-level regulatory shifts that change capacity markets or offtake commitments.