The Big Picture

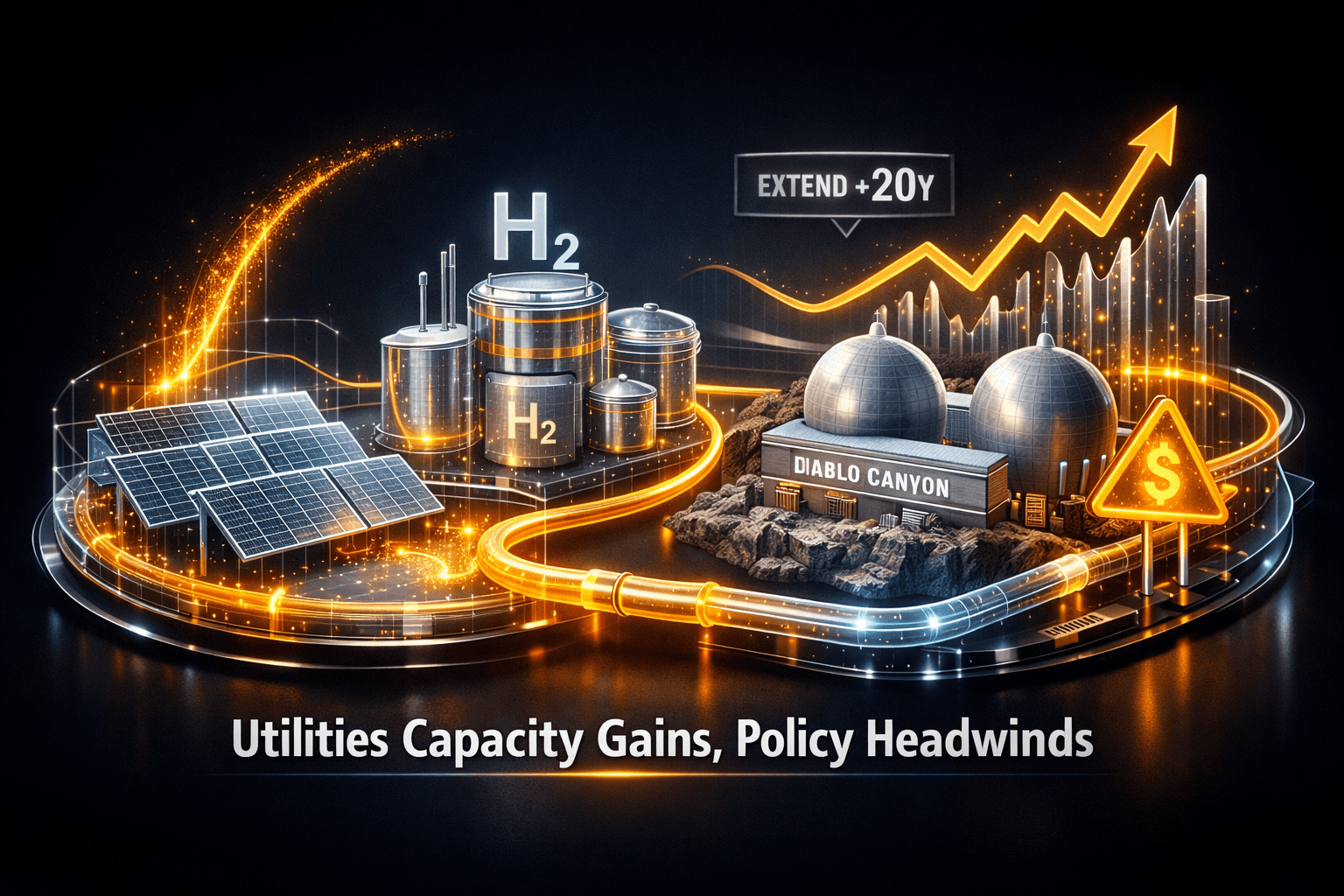

Clean energy capacity and long-term reliability took center stage in the utilities sector this weekend, even as U.S. equity markets were closed. Major developments include new large-scale solar projects and an NRC decision to extend California’s Diablo Canyon nuclear license for another 20 years.

These moves expand generation and practical decarbonization paths, but they arrive alongside fresh policy and cost pressures. You should note that U.S. markets were closed Saturday; the last trading day was Thursday, Apr 2, and the next session opens Monday, Apr 6.

Market Highlights

Key facts and figures to keep on your radar as you plan for Monday.

- Superfund repurpose: A New Mexico Superfund site is slated to host a 50 MW solar array paired with green hydrogen production for night-time clean power.

- Ohio solar online: Geronimo Power began commercial operations at the 117 MW Dodson Creek Solar Project, raising its Ohio operating portfolio to about 675 MW.

- Minnesota VPP: The MPUC approved Xcel Energy’s Capacity*Connect Phase 2, expected to spur 50 to 200 MW of new capacity, but renewables groups say the program “misses the mark.” $XEL is the utility behind Capacity*Connect.

- Tariff changes: New U.S. rules take effect Apr 6, keeping a 50% tariff on goods made almost entirely of steel, aluminum or copper, 25% on derivative products, and setting a 15% rate for some electrical grid equipment.

- Nuclear license: The NRC approved another 20-year operating license for Diablo Canyon, supporting long-term baseload capacity in California. Diablo Canyon is operated by Pacific Gas and Electric, $PCG.

- Regulatory friction: FERC was urged to reject TeraWulf’s planned power plant purchase over an undisclosed Google ownership stake tied to a data center plan, a development affecting $WULF.

- EV signals: Auto-market coverage showed a mixed picture for EVs, but Hyundai IONIQ 5 sales are up year to date, which suggests incremental electricity demand from EV uptake.

Key Developments

Repurposing contaminated sites for clean power

The New Mexico Superfund-to-solar plan combines a 50 MW solar array with green hydrogen production for night-time dispatch. The project illustrates a growing trend of using previously contaminated or constrained land for utility-scale renewables and energy storage solutions.

For you that follow capacity growth, this model could speed deployments where land availability and permitting are otherwise bottlenecks. It could also offer carbon and community benefits that matter to regulators and offtakers.

Grid equipment tariffs and localized supply chain wins

Federal tariff changes rolling in on Apr 6 will raise costs for many imported metals and related products, though some grid equipment will carry a lower 15% rate. Higher tariffs could raise capital costs for transmission, storage and generation projects.

At the same time the Dodson Creek project highlights the value of local manufacturing. Ohio-made modules were used on the 117 MW build, which can mitigate some tariff exposure and shorten supply chains. Could local sourcing become a bigger factor in project economics? It looks likely.

Baseload certainty vs regulatory scrutiny

The NRC’s 20-year extension for Diablo Canyon reinforces long-term baseload availability in California and reduces near-term reliability risk. That’s meaningful for planners facing seasonal peak pressures and for markets pricing long-duration capacity.

Yet regulatory friction is alive elsewhere. FERC was urged to block TeraWulf’s power plant purchase amid questions about undisclosed ownership links to a major cloud provider. That case shows how transactional transparency and data center strategies are now intertwined with grid approvals.

What to Watch

Focus on catalysts and risks that will affect project economics and utility strategies into next week and beyond.

- Apr 6 tariff implementation: New tariff rates take effect, possibly lifting equipment costs and affecting project-level margins. Track commentary from utilities and EPCs on immediate price impacts.

- FERC outcome for TeraWulf: The commission’s decision will offer signals on how regulators treat corporate ownership disclosures for power site deals, and whether data center-power pairings face tighter scrutiny.

- Minnesota VPP rollout: Watch how Capacity*Connect’s Phase 2 is implemented and whether criticisms from renewables groups lead to program changes or legal challenges. VPP design matters for developer returns and customer participation.

- Project supply chains: Keep an eye on how developers respond to tariffs with more domestic sourcing or renegotiated contracts. The Dodson Creek example suggests local manufacturing can blunt tariff effects.

- EV demand trends: If EV sales momentum, like the IONIQ 5 uptick, persists you could see increased utility load forecasts. How will your local utility plan capacity additions or managed charging incentives?

Bottom Line

- Capacity additions are tangible: new utility-scale solar and a long-term nuclear license point to more reliable, lower-carbon generation over the next two decades.

- Policy and cost headwinds are real: tariffs and program design questions could raise project costs and delay deployments, so margin pressure is likely for some builds.

- Local supply chains matter: projects using domestically manufactured components will be better positioned to absorb tariff impacts and schedule risk.

- Regulatory scrutiny has bite: transactions that touch large tech partners or data centers could face closer review, increasing approval risk and timelines.

- Stay selective and informed: analysts note the sector shows momentum, but execution and permitting risk will determine winners. That could move the needle for returns and reliability.

FAQ

Q: How will the new tariffs affect utility project costs? A: Tariffs effective Apr 6 raise duties on metal-intensive goods to 50% and derivatives to 25%, with some grid equipment at 15%. That will likely increase capex for transmission and storage projects unless developers shift to domestic suppliers or renegotiate contracts.

Q: What does Diablo Canyon’s license extension mean for grid reliability? A: The 20-year NRC extension keeps significant baseload capacity online in California, reducing near-term supply risk and helping meet demand during peak periods while other resources scale up.

Q: Should I expect more projects like the Superfund solar-hydrogen plan? A: The model is gaining traction because it uses constrained land and pairs generation with long-duration storage or hydrogen for night-time dispatch. Project frequency will depend on permitting, off-take contracts and economics under changing tariff and supply conditions.