The Big Picture

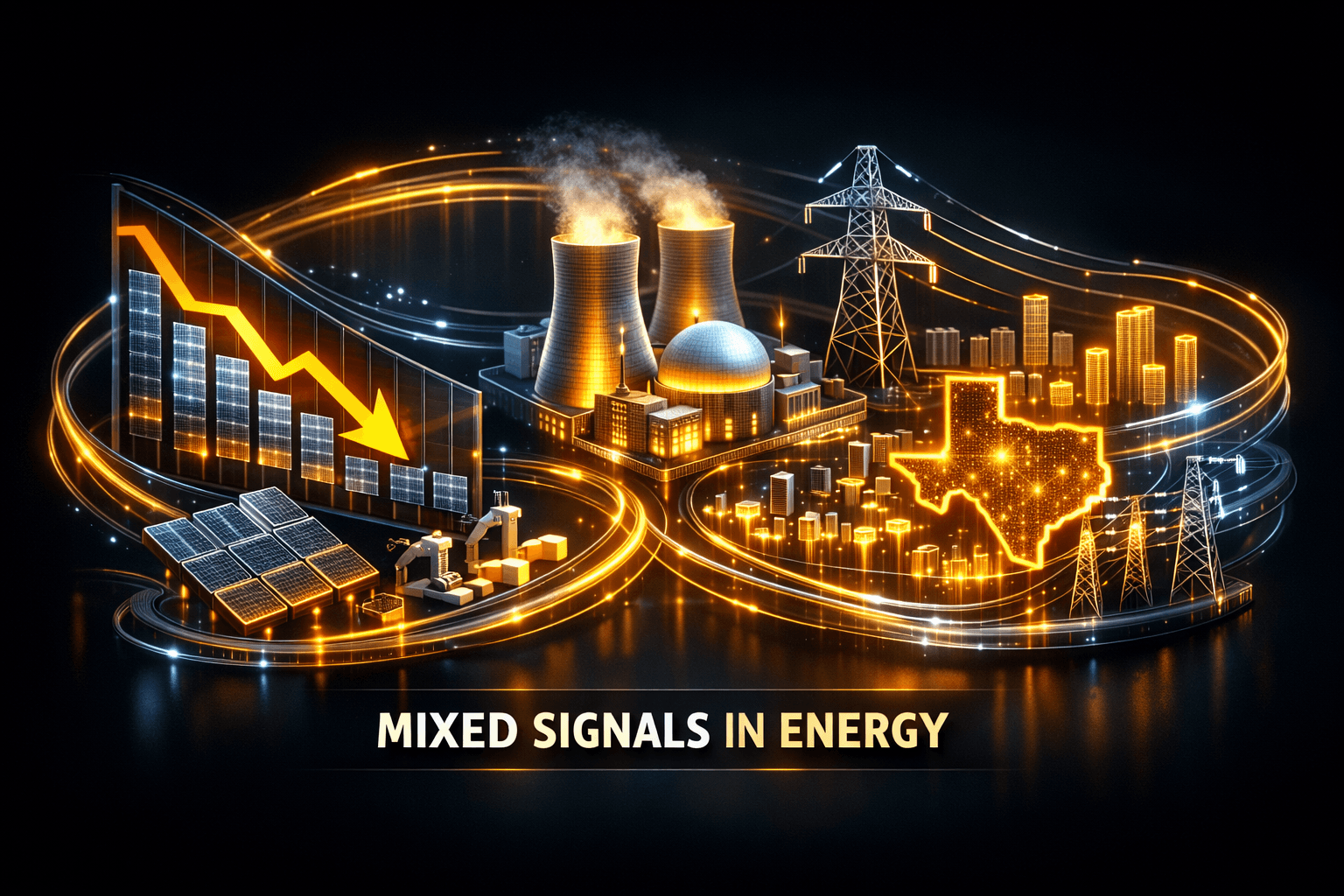

The utilities sector is sending you mixed signals this morning, with a striking 22% drop in solar installations reported for 2025 standing alongside fresh factory capacity, grid modernization plans and a sizable state push for advanced nuclear. That split matters because it shows supply chain and policy support exist, even as developers delay project buildouts and market dynamics change.

For investors who track power demand and capacity, the takeaway is straightforward. You need to weigh slower near-term renewable deployments against longer-term gains from manufacturing onshoring, grid upgrades and electrification trends that will keep structural demand intact.

Market Highlights

Quick facts and numbers to put today in context.

- Solar installations fell 22% in 2025, according to FERC reporting and industry commentary.

- U.S. coal exports declined from 108 million short tons in 2024 to 93 million short tons in 2025, a drop of 16 MMst; thermal coal exports fell 18% and metallurgical coal fell 11%.

- US Modules opened its College Station, Texas, solar panel assembly line with 400 MW annual capacity per line planned.

- Texas launched $350 million in advanced nuclear grants through the Texas Advanced Nuclear Development Fund, aimed at reactor builds and supply chain development.

- National Grid and GridCARE announced a partnership to reduce "time to power" for large loads in New York, improving grid utilization.

- Rivian and Volkswagen joint venture RV Tech completed winter testing of its zonal architecture for software defined vehicles, a step that could affect EV load profiles over time, involving $RIVN and $VWAGY.

Key Developments

Renewables: installation slump, but manufacturing and project-level support rise

FERC data and industry commentary show solar installations dropped 22% in 2025 as developers prioritized safe harbor strategies and deferred late-stage builds. That slowdown reduces near-term capacity additions and may squeeze growth metrics for utilities with aggressive distributed or utility-scale solar plans.

Meanwhile, US Modules started production in Texas with an initial 400 MW annual line that will supply its parent company projects. State-level backing of a 5-MW Hannacroix Solar project in New York shows local authorities are still deploying targeted support to keep projects on track for tax credit deadlines.

Grid and electrification: faster connections and transit electrification

National Grid's GridCARE initiative is designed to shorten "time to power" for large loads, which could reduce interconnection bottlenecks for data centers and manufacturers. Faster connections matter for you if you follow utility earnings and capex, because they influence revenue streams tied to system upgrades.

On the transport side, electric bus deliveries continued in Australia amid high diesel costs above AU$3 per litre, reinforcing the operational case for electrification. That shift can increase electricity demand in urban networks and change load shape for utilities over time.

Fuel mix and policy: coal press coverage and nuclear incentives

U.S. coal exports fell in 2025, prompting debate over coal's role in power generation and exports. Industry groups responded with rebuttals emphasizing reliability and cost competitiveness, so expect that narrative to shape regulatory and public discussion.

At the same time, Texas opened a $350 million grant program to accelerate advanced nuclear deployment and supply chain work. That program adds a new layer of state-level influence on long-term capacity planning for regional utilities.

What to Watch

Here are the catalysts and risks you should track today and in the coming weeks.

- Policy and funding: Watch application windows and award criteria for the Texas $350 million program, and how utilities respond to potential supply chain funding opportunities.

- Solar pipeline and tax credits: Monitor developer filings and interconnection updates tied to safe harbor strategies and tax credit deadlines, since delayed completions drove the 22% drop.

- Grid resilience and weather data: Severe weather season starts now, so utilities' use of improved weather data and operational analytics could affect outage frequency and cost. Are utilities prepared for an active season?

- Interconnection and "time to power": Track pilot results from National Grid and GridCARE for impacts on connection timelines, especially for large commercial loads and data centers.

- Electrification demand profile: Follow EV fleet rollouts and large-scale transit electrification, including implications for distribution upgrades and time-of-use pricing.

Bottom Line

- Solar installations falling 22% is a meaningful headwind for near-term renewable capacity, even as manufacturing capacity like the US Modules plant helps future supply.

- Grid modernization efforts such as National Grid's GridCARE could unlock demand and shorten project timelines, but improvements take time to feed earnings.

- State-level incentives for advanced nuclear in Texas add a new long-term supply option, while coal export declines are prompting industry pushback and debate about baseload roles.

- Severe weather season increases the importance of operational data and resilience investments, which may drive utility capex and outage-related costs this year.

- You're seeing a mixed bag in the sector, so stay selective and track catalysts rather than assuming a single trend will dominate.

FAQ Section

Q: How will a 22% drop in solar installations affect utility planning? A: Slower installations can delay distributed and utility-scale capacity additions, compress near-term growth metrics and shift investment timelines, but manufacturing and policy support may restore momentum over time.

Q: Does the decline in U.S. coal exports mean coal power plants will retire faster? A: Not necessarily. Export declines affect coal markets and some plant economics, but operators and industry groups are emphasizing reliability and cost arguments, so retirements will depend on local policy and market conditions.

Q: What does Texas' $350 million nuclear grant program mean for you as an investor watcher? A: The program signals state support for advanced nuclear supply chains and project funding, which could influence long-term capacity mixes and utility procurement decisions, but projects will unfold over many years and require monitoring of awardees and permits.