The Big Picture

A blend of project approvals, policy rulings, and technology showcases left utilities watchers with mixed signals heading into the long weekend. Federal and private investment plans are racing to shore up generation and transmission, even as renewable project setbacks and operational cost questions raise fresh doubts.

Why does this matter for you? These developments will influence capacity mixes, regional grid reliability, and regulatory returns, and they shape where utilities and service providers may shift capital in the months ahead.

Market Highlights

Here are the quick facts and numbers investors should carry into Monday, with U.S. markets closed on Sunday.

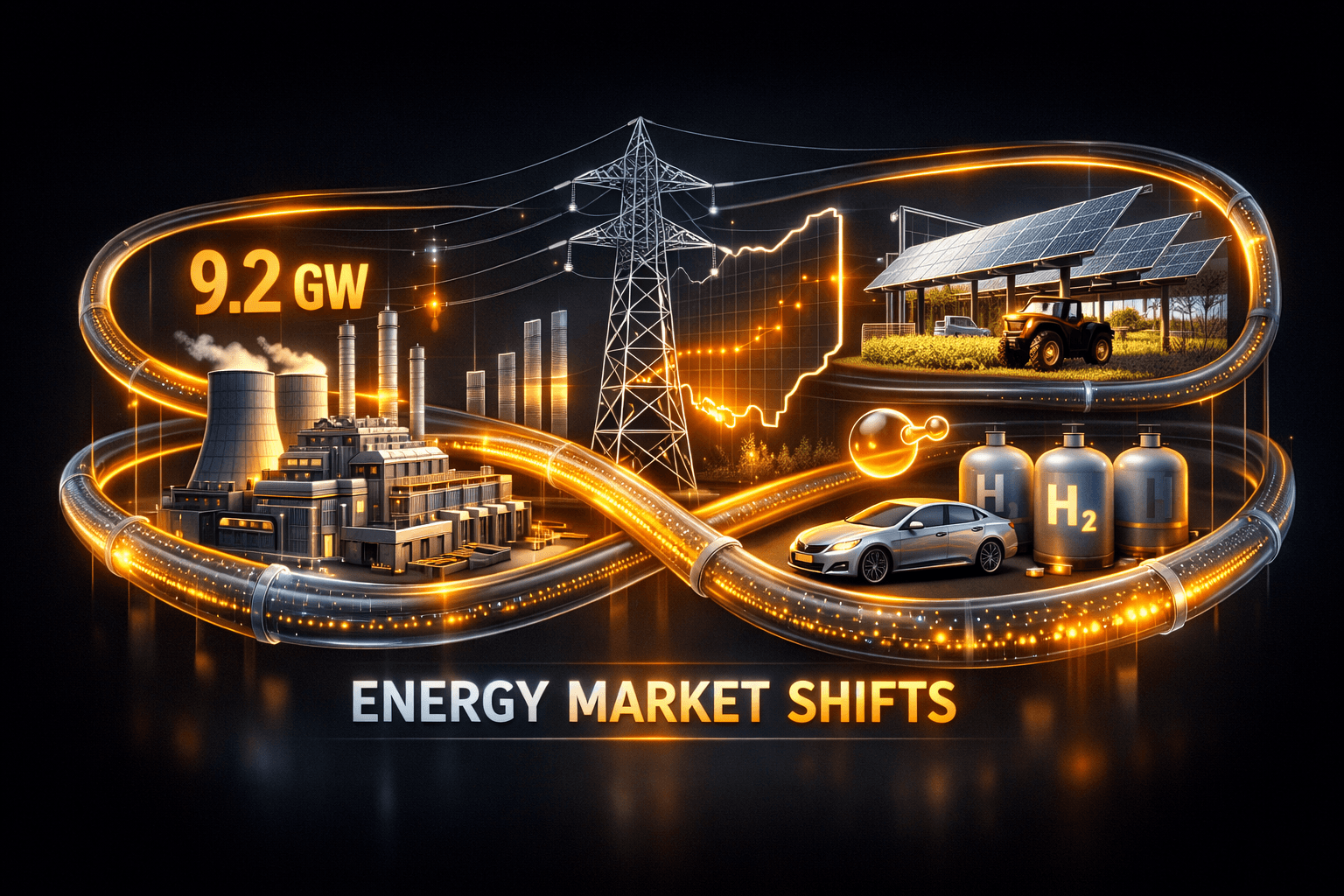

- DOE selects SB Energy, SoftBank Group’s renewables arm, to develop roughly 9.2 GW of gas-fired generation in Ohio, paired with a $4.2 billion transmission upgrade partnership with $AEP.

- CleanTech reports a battery-equipped induction range from Copper that combines electrification with on-site storage, pointing to growing distributed electrification devices hitting the market.

- Regulatory and project headwinds: Ohio denied a 94-MW agrivoltaic solar project in Morrow County; FERC rejected an $RWE complaint on PJM interconnection practices and cut New England’s transmission return on equity.

- Operational caution: CleanTechnica highlights high costs and emissions questions around SunLine Transit’s hydrogen fuel cell fleet, underscoring that hydrogen solutions still face economic hurdles.

Key Developments

DOE, SoftBank and $AEP Team on 9.2 GW Gas Push

The Department of Energy tapped SB Energy to help develop 9.2 GW of natural gas generation in Ohio and to co-invest in transmission upgrades with $AEP totaling roughly $4.2 billion. This is a clear, near-term federal-private effort to bolster capacity in a region where reliability and interconnection bottlenecks have been urgent issues.

For investors, the move suggests near-term demand for construction, engineering, and transmission services. It also raises questions about long-term fuel mix strategy, regulatory approvals, and how communities will weigh fossil generation against decarbonization goals.

Distributed Electrification: Battery-Equipped Induction Range

At the New York Build Expo, Copper showcased an induction range with an integrated battery in the base. The product signals how consumer-level electrification plus embedded storage could reduce peak grid draws and enable new behind-the-meter load shifting strategies.

Could this be the tip of the iceberg for more appliance-level storage? If such devices scale, utilities, muni programs, and vendors may need to rethink demand forecasts and interconnection rules for distributed energy resources, and you may see new commercial opportunities for companies that enable residential storage and controls.

Renewables and Regulation: Project Cancellations and FERC Rulings

Ohio’s Power Siting Board unanimously denied a 94-MW agrivoltaic solar project in Morrow County, a setback for developers targeting co-located solar-plus-agriculture models. Meanwhile, FERC rejected an $RWE complaint against PJM interconnection practices, lowered New England transmission ROE, and allowed some utilities to spread costs tied to DOE emergency orders keeping coal plants online.

These moves underscore a regulatory environment that can cut both ways for renewables and transmission investors. They also highlight that permitting, local opposition, and rate-setting remain central risks for project economics.

What to Watch

Expect the headlines to keep coming as stakeholders respond to federal and local decisions. Here are the catalysts and risk points you should monitor and questions to ask.

- Monday and next week, watch statements from $AEP and SB Energy for project timelines, permitting milestones, and contracting partners. What are the expected in-service dates and staged spending plans?

- Track FERC docket activity and state siting board appeals after the Ohio denial and the RWE ruling. Will developers take projects to court or refile with altered proposals?

- Keep an eye on technology adoption signals for distributed storage appliances. Will utilities update interconnection or rebate programs to account for battery-equipped devices?

- Monitor hydrogen program cost disclosures and lifecycle emissions analyses, especially for transit agencies. Are fuel sourcing and electrolyzer economics improving, or are gray hydrogen costs still dominant?

- Risk watch: permitting uncertainty, regulatory ROE actions, and community opposition can delay or derail projects, so factor regulatory risk into any thesis you’re following.

Bottom Line

- Federal and private funds are being directed at near-term capacity and transmission upgrades, which could ease short-term reliability concerns.

- Distributed electrification products that bundle storage are emerging and may change residential load profiles, creating new demand-side flexibility opportunities.

- Renewable project development faces persistent permitting and regulatory hurdles, as shown by the Ohio agrivoltaic denial.

- Regulatory decisions out of FERC and state boards will remain a key determinant of returns for transmission and generation businesses.

- Hydrogen use cases, especially for transit, still show cost and emissions questions, so timelines for widescale adoption remain uncertain.

FAQ Section

Q: How will the DOE-SB Energy plan affect local grid reliability? A: The planned 9.2 GW of gas capacity and $4.2 billion in transmission upgrades are intended to bolster regional capacity and relieve bottlenecks, but timing depends on permitting and construction schedules.

Q: Should you expect faster adoption of battery-equipped appliances? A: Early products like Copper’s range show market interest, and data suggests behind-the-meter storage adoption could accelerate if incentives and interconnection are clarified.

Q: What do FERC and state rulings mean for renewable projects? A: Regulatory rulings can change project economics quickly. You should watch appeals, ROE adjustments, and siting board outcomes because they influence developer returns and financing costs.