The Big Picture

Deal activity in commercial real estate picked up late last week, and housing metrics showed surprising resilience, giving the sector a constructive tone heading into the long weekend. You should note that U.S. markets were closed on Sunday, Jul 5, so the last market prices are as of Thursday, Jul 2.

Why does this matter to you as an investor? Better mortgage spreads and a string of transactions suggest both financing conditions and buyer confidence are improving, which could support earnings for lenders, homebuilders and REITs as we move into the second half of 2026.

Market Highlights

Here are the quick takeaway facts you can use for screening and watchlists.

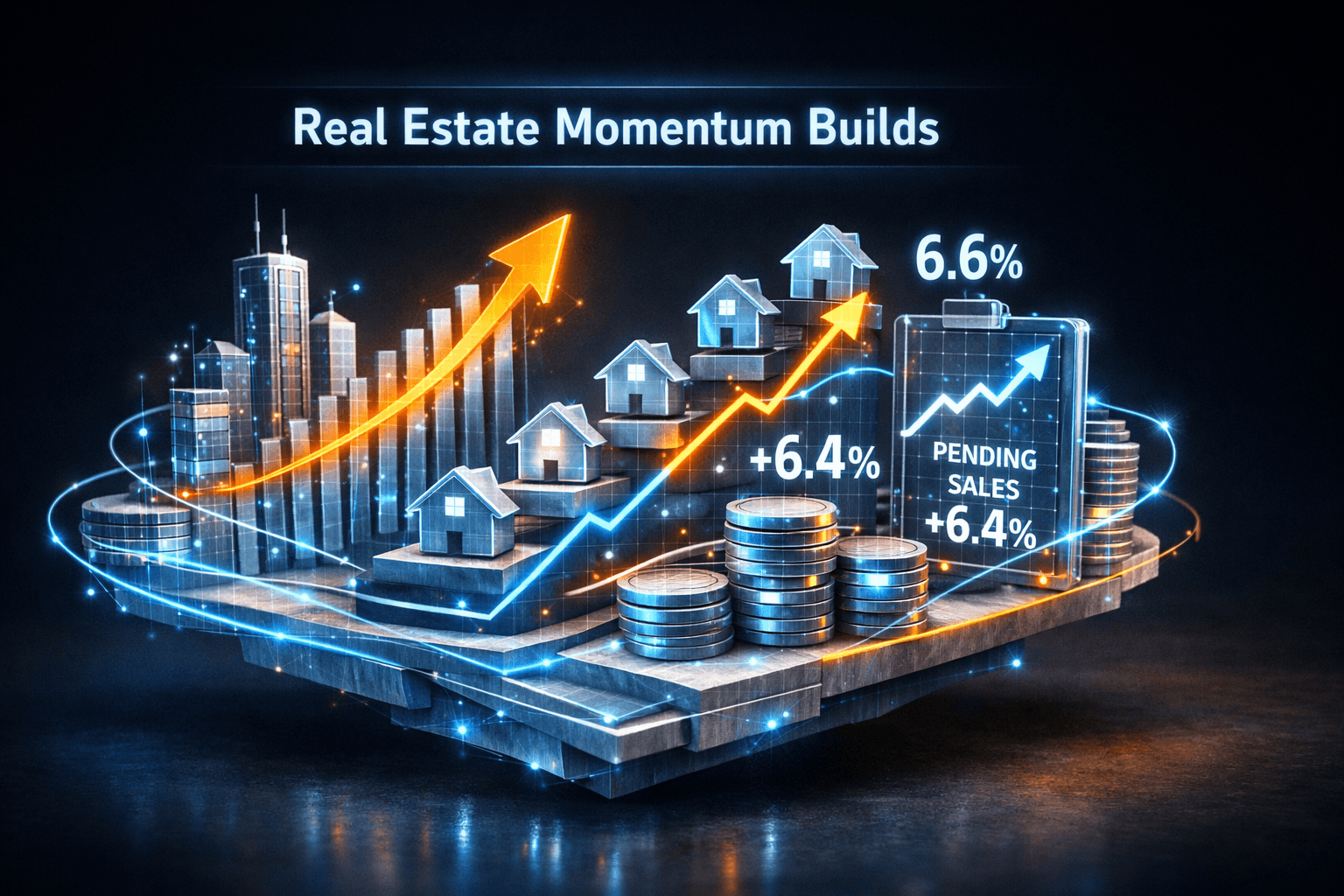

- Mortgage spreads improved to 2.01%, keeping benchmark mortgage rates near 6.60% as of the HousingWire report.

- Pending home sales rose to 422,120 from 396,652 a year earlier, a roughly 6.4% year over year increase, signaling continued demand.

- Commercial deal activity accelerated last week, led by major investors including Bridgepoint Group, with multiple transactions reported and market participants describing the pace as "lit up like a fireworks display."

- Public proxies for the sector, such as the real estate ETF $VNQ and mortgage REITs like $NLY, are likely to be sensitive to these moves in spreads and transaction volumes heading into trading on Monday, Jul 6.

Key Developments

Deal Flow Back on the Table

Commercial Observer described a busy week of dealmaking, highlighting a surge in transactions across office conversions, logistics and mixed use assets. Investors like Bridgepoint Group and other institutional players were active, which suggests fresh capital is finding use cases in both core and opportunistic strategies.

For your portfolio, that means liquidity for larger assets is available again, and pricing debates may shift from defensive to selective expansion. Are undercapitalized owners going to benefit? If you're tracking REIT holdings you may want to review disclosures for new asset purchases or capital raises once markets reopen.

Mortgage Spreads Narrow, Home Sales Hold Up

HousingWire reported mortgage spreads narrowing to 2.01% and overall mortgage rates sitting near 6.60%. That helped pending home sales rise to 422,120, up about 6.4% from last year. The data suggests mortgage market friction eased enough to keep buyer activity positive despite still-elevated rates.

What does this mean for builders and mortgage lenders? Homebuilders and regional banks that underwrite mortgages may see steadier demand in the near term. You should monitor upcoming monthly sales data and builder guidance for signs the trend is sustainable.

Cross-Asset Implications

Improved spreads and active commercial deals tend to lift related sectors unevenly. Mortgage REITs often respond to tightening spreads, while timber, industrial and residential REITs feel the effects of transaction volume and consumer demand differently.

Keep an eye on announcements from listed lenders, homebuilders and REITs when markets reopen. Earnings and balance sheet moves will tell you if this momentum is translating to revenue growth or just transient activity.

What to Watch

Here are the catalysts and risks you should track before markets open Monday, Jul 6.

- Earnings and guidance from major homebuilders and mortgage lenders, which could confirm whether sales growth is sustainable into the summer.

- Weekly mortgage application and pending sales updates, which will show if the 6.4% year over year gain persists.

- Any filings or press releases from big private equity and real estate investors detailing large acquisitions, dispositions or capital raises announced over the holiday weekend.

- Macro data and Fed commentary due this week, which could shift borrowing costs and affect both mortgage spreads and cap rates.

- Liquidity trends in commercial markets, especially pricing for logistics and multifamily assets, which determine near-term valuation trajectories.

Are you watching specific tickers? Consider tracking sector ETFs like $VNQ and mortgage-sensitive names such as $NLY to see how the market prices this mix of improved spreads and deal activity when trading resumes.

Bottom Line

- Deal activity accelerated late last week, signaling renewed capital deployment in commercial real estate.

- Mortgage spreads narrowed to 2.01% and mortgage rates hovered near 6.60%, supporting a 6.4% year over year rise in pending home sales.

- These developments suggest momentum building in both commercial and residential segments, but the durability of demand is still the key question.

- Monitor upcoming sales data, earnings and any deal disclosures once markets reopen on Monday, Jul 6, for clearer signals.

- Data suggests opportunity and risk coexist, so a selective approach toward listings, REITs and mortgage-sensitive securities is warranted.

FAQ

Q: How did mortgage spreads affect home sales? A: Narrower mortgage spreads lowered effective borrowing costs, keeping average rates near 6.60% and helping pending sales rise about 6.4% year over year.

Q: Should you expect more commercial deal announcements? A: Reports show active dealmaking and institutional interest, so additional transactions and capital raises are likely to surface as market players finalize trades.

Q: Which metrics should you monitor this week? A: Watch weekly mortgage applications, pending and existing home sales, earnings from homebuilders and lenders, and any large transaction filings that reveal pricing trends.