The Big Picture

Real estate investors start the day facing a string of headwinds that are more regulatory and credit related than cyclical. Consumer groups have asked federal enforcers to probe MLS practices, fraudsters are using AI to target property deeds in Florida, and data show older borrowers face higher mortgage denial rates.

These developments matter because they raise legal, operational and credit risks for brokers, lenders, title insurers and property owners. If you own REIT shares, hold mortgages or follow local markets, today's headlines increase uncertainty and could influence capital flows in the near term.

Market Highlights

Quick facts to start your trading day.

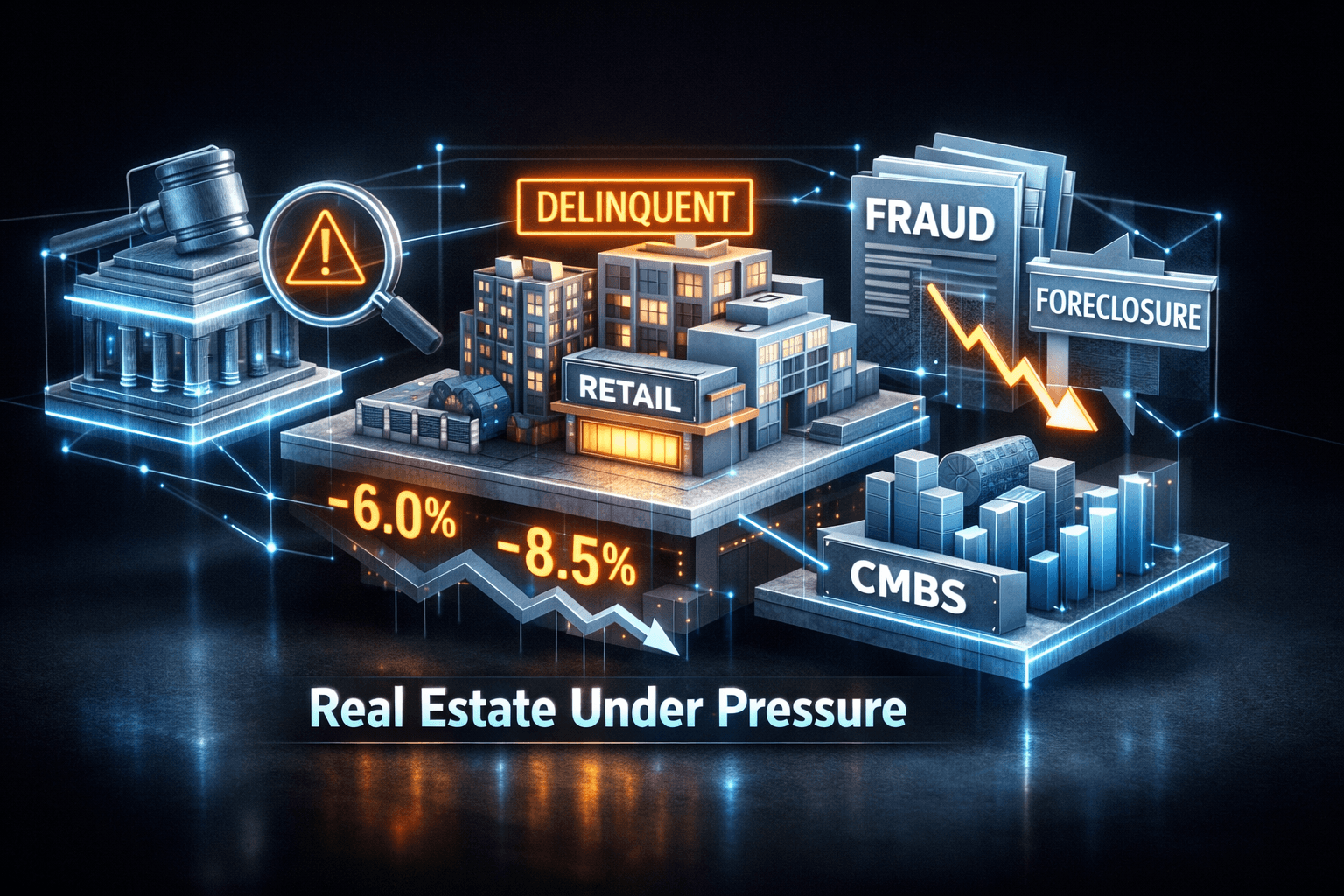

- Regulatory pressure: A consumer coalition asked the FTC and DOJ to probe Compass MLS deals, citing off-MLS pocket listings and competition concerns.

- Fraud risk: Florida fraud alerts highlight rising use of public records and AI to forge deeds, prompting recommendations for title insurance and county alert services.

- Mortgage access: Mortgage denials are running 1.5% higher for borrowers aged 60 to 69 and 2.7% higher for those 70 and up, according to HousingWire reporting.

- CMBS snapshot: Trepp's overall CMBS delinquency rate fell 20 basis points to 7.35% in June, but retail and multifamily delinquencies increased, with the five largest newly delinquent loans totaling $998.9 million of $2.64 billion.

- Weekly lender update: Connect CRE's Return to Lender highlights ongoing lender workouts and market monitoring ahead of summer refinancing waves.

Key Developments

Regulatory Probe into Compass MLS Deals

Consumer groups have formally urged the Federal Trade Commission and Department of Justice to investigate Compass's MLS practices, pointing to off-MLS pocket listings, limits on competition and potential fair housing risks. The request elevates scrutiny on brokerage behavior and could lead to enforcement action or changes in MLS rules and disclosure practices.

For you that means brokerage models and local listing flows could face disruption if regulators pursue remedies. Sellers and brokers may need to adjust how listings are shared to stay compliant and avoid fines.

AI-Driven Deed Fraud Surge in Florida

HousingWire reports a rise in deed fraud where bad actors use public records plus AI to impersonate owners and forge documents. The article outlines distinctions between void and voidable deeds and recommends protections including title insurance and county alert services.

This is a direct operational risk for title insurers, property managers and homeowners. If you're exposed to Florida markets, consider whether your title policies and monitoring services are current, because fraud cases can be costly and time consuming to resolve.

Mortgage Denials and CMBS Stress Signals

Data show older borrowers face higher denial rates, with a 1.5% increase for ages 60 to 69 and 2.7% for 70 and above, driven by debt to income and documentation rules. This suggests lenders are using tightened underwriting that may not reflect retirees' asset positions.

Separately, Trepp reports the CMBS delinquency rate fell to 7.35% in June, down 20 basis points, but three of five major property types saw higher delinquencies, and nearly $1 billion of newly delinquent loans were concentrated among the largest defaults. What looks like improvement on the surface may be masking pockets of stress.

What to Watch

Focus on these catalysts and risks as trading continues today and into the week.

- Regulatory action: Watch for any statements or filings from the FTC or DOJ about the Compass probe, and state real estate regulators' responses.

- Title and fraud mitigation: Expect increased demand for title insurance and county alert services in Florida. Check whether major title insurers comment on claims trends.

- Lending rule changes: Keep an eye on GSE guidance and non-QM lender announcements that could address asset depletion rules and documentation standards for retirees.

- CMBS surveillance: Monitor Trepp and servicer updates for any follow-on defaults or loan resolutions. Large newly delinquent balances can influence market pricing for CMBS tranches.

- Earnings and commentary: If REITs or mortgage servicers report this week, pay attention to loss reserves, credit commentary and any mention of litigation or regulatory costs.

How should you respond to this mix of risk? Be selective and insist on current data before you make allocation choices, because headlines may be the tip of the iceberg for longer term legal or credit implications.

Bottom Line

- Regulatory scrutiny of brokerage MLS practices raises legal and operational risk for brokers and sellers.

- AI-enabled deed fraud is a growing operational threat in Florida, increasing demand for title protections and monitoring services.

- Lenders appear to be disadvantaging many older borrowers through tighter DTI and documentation rules, which could pressure mortgage origination volumes.

- CMBS data show mixed credit trends, with overall delinquency down but concentrated new delinquencies totaling nearly $1 billion.

- Watch for agency statements, servicer updates and title insurer comments that could change market sentiment quickly.

FAQ Section

Q: What does a probe into MLS deals mean for local housing markets? A: A federal probe can change listing practices and disclosure rules, which may affect how quickly homes appear on MLS and how buyers access inventory.

Q: How can property owners protect against AI-driven deed fraud? A: Owners can maintain title insurance, enroll in county deed alert services and review recent county filings regularly.

Q: Why are older borrowers denied more often despite assets? A: Lenders often rely on DTI and income documentation that do not fully account for retirement assets or different depletion horizons, leading to higher denial rates.