The Big Picture

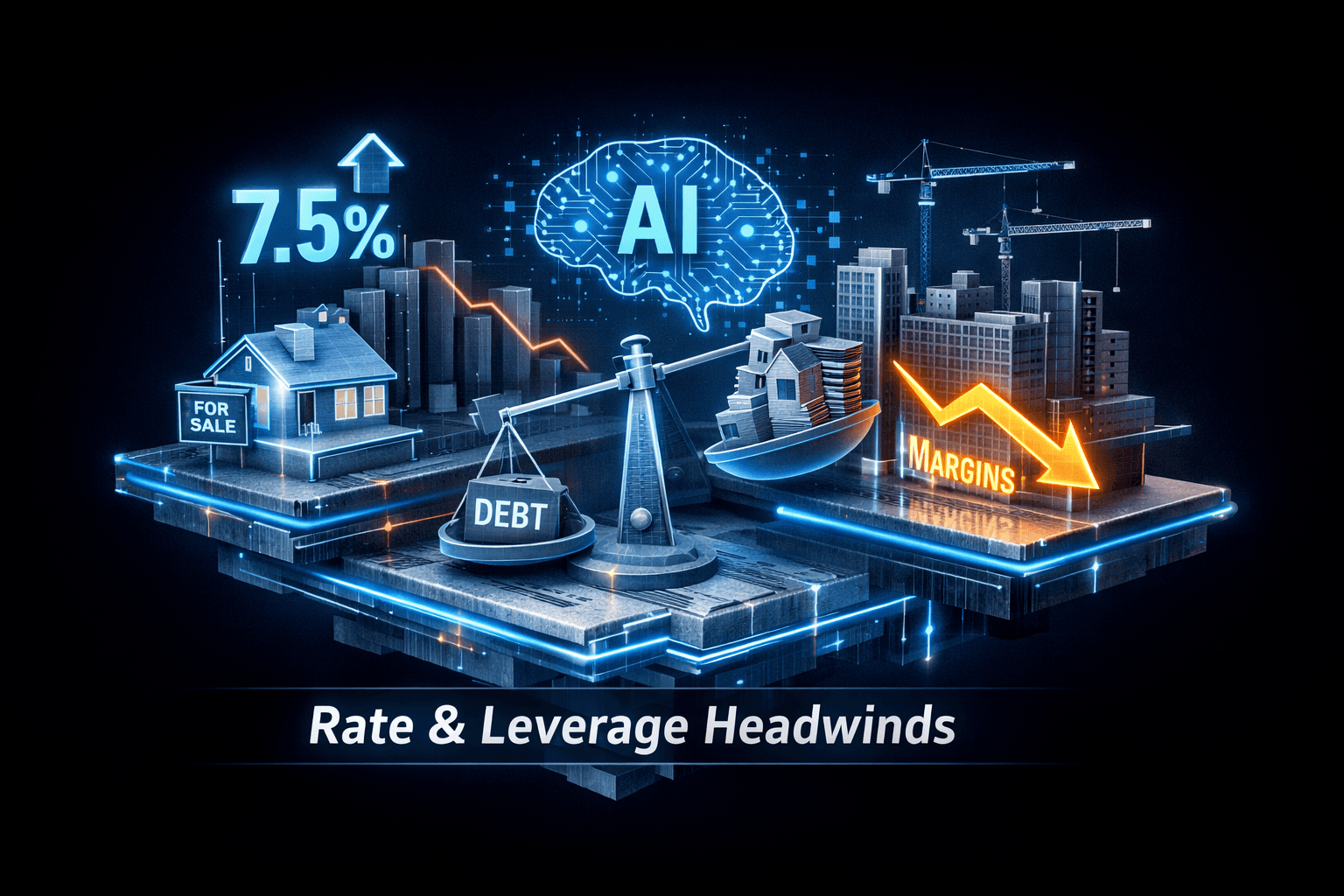

Real estate investors woke up to a cautionary script on Jun 30, as multiple industry voices warned that high rates, excessive leverage and rapid tech adoption are creating fresh headwinds. The most impactful takeaway is simple, but urgent: conservative underwriting and stronger governance are becoming prerequisites for portfolio resilience.

That matters to you because the market drivers this week are structural, not temporary. Mortgage rates that are likely to stay in the 6% to 6.5% band, governance gaps around AI in lending, and builders prioritizing margin recovery all point to slower volume and higher execution risk for the next several quarters.

Market Highlights

Here are the quick facts you should have at the top of your mind this morning.

- Mortgage rates: Industry commentary and lender guidance now suggest a 6% to 6.5% range over the next three years, which will constrain homebuying demand and refinance activity.

- Leverage risk: Analysts and industry experts are urging more conservative leverage and underwriting standards after recent volatility in financing costs.

- Homebuilders: Major public builders including $DHI, $LEN and $PHM are talking margin recovery through standardization and faster permitting rather than pushing for volume growth.

- Mortgage tech: Lenders are accelerating AI adoption, but HousingWire flags governance and compliance risks that could draw regulatory scrutiny if not addressed.

- Community activity: The Real Estate Board of New York’s Fellows continue local outreach with projects like the Fisher House Foundation volunteer day, underlining the sector’s community ties and ESG focus.

Key Developments

Hidden Cost of Leverage

HousingWire’s feature on leverage argues that today’s high-cost financing environment makes aggressive borrowing riskier than ever. The piece stresses conservative underwriting and steady cash flow over equity extraction and speculative bets.

For you, that means loans and properties that looked profitable under lower rates may no longer absorb shocks. Analysts note higher stress on interest-sensitive cash flows, so if you hold leveraged positions you'll want to review covenant buffers and refinancing timelines.

AI in Mortgages, Governance Gap

HousingWire also reports a rapid, industry-wide AI adoption spree in the mortgage sector. Lenders are deploying models to speed processing and cut costs, but the story warns these rollouts risk outpacing compliance and audit capabilities.

Regulators and capital markets will be watching for explainability, data lineage and decision accountability. If you follow mortgage lenders or mortgage REITs, pay attention to management commentary on AI governance and any disclosures about model risk frameworks.

Builders Pivot to Margin Recovery

Homebuilders are shifting strategy after a weaker-than-expected spring selling season. With rates likely to remain elevated for years, builders are prioritizing standardized design, tighter cost controls, faster permitting and connected workflows to cut rework and carrying costs.

The implication is clearer earnings compression control rather than top-line volume growth. For sector exposure through homebuilders or suppliers, expect a heavier focus on margin metrics, backlog quality and conversion efficiency in upcoming reports.

What to Watch

Watch these catalysts and risk factors that could move the sector in the coming days and weeks.

- Mortgage rate commentary and Fed communications, because rate expectations will determine refinance volumes and buyer affordability.

- Earnings and guidance from major homebuilders like $DHI, $LEN and $PHM, where management commentary on margins and backlog conversion will be telling.

- Disclosures by mortgage lenders and mortgage REITs on AI governance. You'll want to see documented model controls, audit trails and compliance investments.

- Credit spreads and CMBS performance, since tighter financing conditions would increase carrying costs for developers and owners.

- Local permitting and policy updates in large MSAs, because builders cited permitting speed as a lever for margin recovery. Faster approvals can cut carrying costs, and slower approvals will squeeze margins further.

How should you prioritize? Start with liquidity and underwriting quality for any exposure tied to leverage. Next, look for managements that are transparent about AI controls and margin-recovery tactics.

Bottom Line

- High mortgage rates and warnings on leverage set a cautious tone across the real estate sector.

- Rapid AI adoption in mortgage origination improves efficiency but raises governance and compliance risks to monitor.

- Homebuilders are shifting from volume to margin recovery, which implies a different earnings profile for the next several quarters.

- Review leverage, refinancing timelines and covenant buffers if you have exposure to leveraged property holdings or mortgage credit.

- Community and ESG initiatives remain a positive reputational factor, but they don't offset macro and financing headwinds.

FAQ Section

Q: How will sustained 6% to 6.5% mortgage rates affect housing demand? A: Higher rates reduce affordability and will likely depress transaction volumes and refinance activity, putting pressure on builders and mortgage originators.

Q: Should you be worried about AI in mortgage underwriting? A: Concern is warranted if firms can't demonstrate governance and auditability; reviewers say effective controls reduce regulatory and capital market risk.

Q: What should you check first in your real estate exposure? A: Start with leverage and liquidity, then review management commentary on margins and AI risk controls to understand near-term vulnerability.