The Big Picture

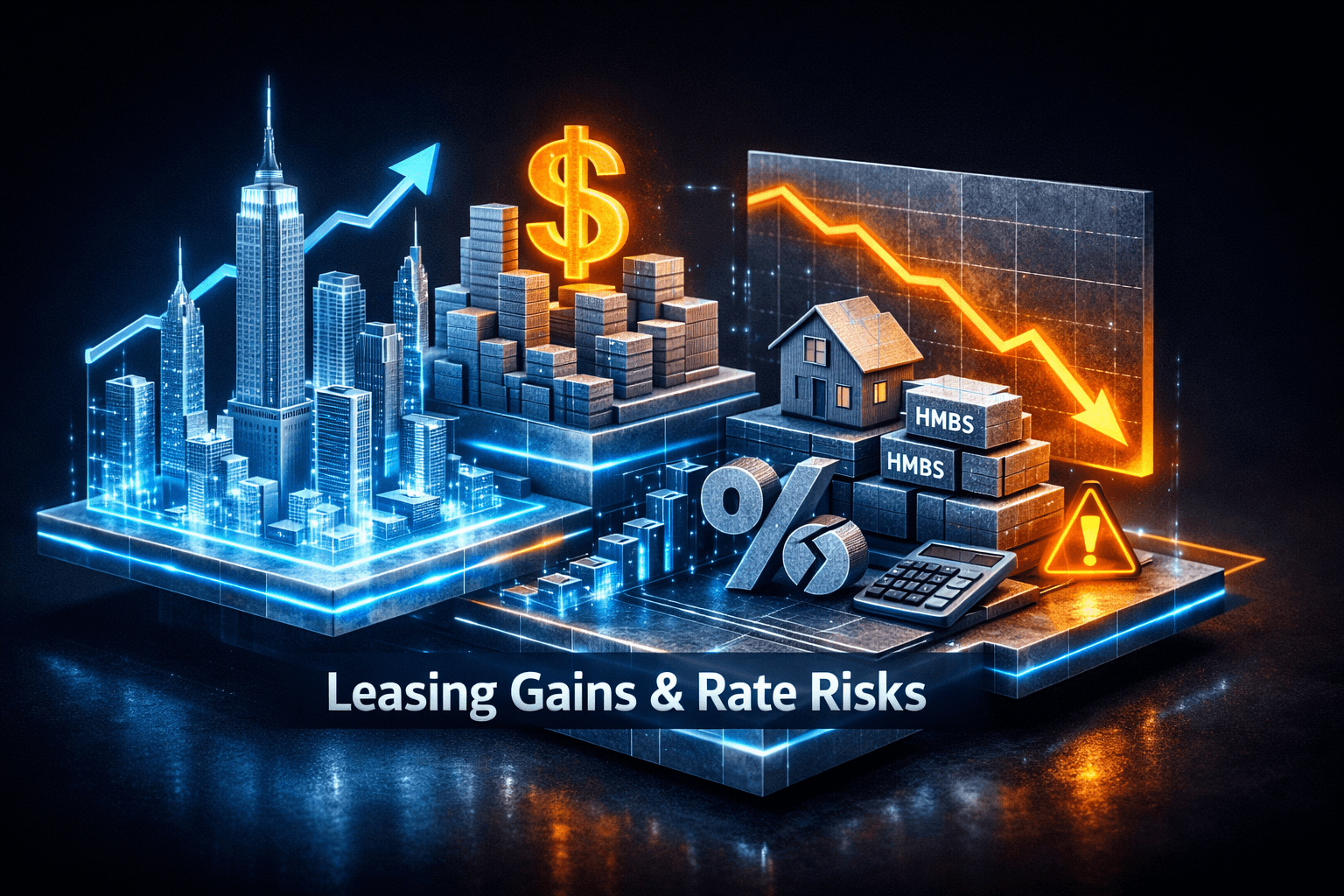

The Real Estate sector opened Monday with mixed signals, as strong commercial leasing and renewed investor interest compete with tightening mortgage conditions and liquidity concerns in housing finance. You can see the split: headline office deals and new brokerage launches point to demand, while higher mortgage rates and HMBS strains underscore financing risk.

This matters because what’s happening in commercial markets won’t fully offset pain in the mortgage and housing-finance pipes, and you need to follow both tracks to understand sector momentum. Where will demand go next, and what will funding look like if rates stay elevated?

Market Highlights

Quick facts and market moves to start your day.

- Office leasing strength: Soloviev Group reported a "record-setting" lease at $327.50 per square foot for a 5,063 sq ft office, a sign of premium pocket resilience.

- Park Ave. South activity: Olmsted Properties and Vertex signed over 67,000 sq ft of leases at 373 and 381 Park Avenue South, representing roughly 20% of the buildings.

- Mortgage rate pressure: Data show conventional mortgage rates climbed from 5.99% to 6.64% over five weeks, a headwind for affordability and buyer demand.

- HMBS and HECM concerns: Industry commentary flags HMBS liquidity strain around a 98% market control amount and hurdles from upfront MIP changes and servicing compliance.

- Industry confidence: AFIRE’s Gunnar Branson reiterated that U.S. commercial real estate is still seen as a safe global allocation, supporting cross-border capital flows.

Key Developments

Reverse mortgage rules and HMBS liquidity

HousingWire coverage highlighted industry leader Elly Johnson discussing HECM rule changes and HMBS liquidity strains, with HMBS trading near a 98% market control amount and new upfront MIP dynamics creating funding friction. Servicing compliance risk was also flagged, which could raise costs and slow product flow for lenders who rely on HECM and HMBS channels.

For you as an investor, that means mortgage-related securities and specialty lenders are the parts of the market most exposed if liquidity tightens further. Analysts note operational and regulatory risk may keep volatility elevated in those corners.

Office leasing shows selective strength

Commercial Observer and Connect CRE report sizable leasing wins in New York, including the Soloviev Group’s $327.50 per sq ft lease and Olmsted and Vertex locking in more than 67,000 sq ft at Park Avenue South. New deals include The Corcoran Group and AI firm Stuut Inc., and owners are starting active repositioning campaigns.

These transactions show localized demand for premium or well-located product, and they suggest a bifurcated office market where core trophy and well-repositioned assets outperform. If you own or track CRE ETFs or REITs with high-quality urban office exposure, earnings and rent-roll updates will matter more now.

Macro pressure: higher rates and global capital flows

HousingWire’s analysis of "war-time economics" points to rising gas prices and spillover to higher mortgage rates, which climbed to 6.64% from a recent 5.99% low. Higher borrowing costs are already squeezing affordability and could slow transaction volume in the housing market.

Counterbalancing that, AFIRE’s message is that U.S. CRE remains a go-to for international investors, which can support pricing and liquidity for commercial assets even as residential activity cools. You’ll want to watch how cross-border flows offset domestic demand declines.

What to Watch

Here are the specific catalysts and risk points to track this week and beyond.

- Policy and regulatory updates on HECM and HMBS: any clarifications on upfront MIP or servicing standards could materially affect HECM lenders and HMBS spreads.

- Mortgage-rate trajectory: a continued move toward or above 6.5% will likely depress single-family sales and refinance volumes, pressuring mortgage originators and some mortgage REITs.

- Leasing and occupancy reports: watch earnings and leasing updates from major REITs and landlords for signs that urban office repositioning is translating into sustained demand.

- Capital flow data: cross-border investment reports and capital-raising activity from global institutional investors will show whether U.S. CRE stays a safe-haven allocation.

- New entrants and regional brokerage moves: the launch of PIR Commercial Realty highlights competition and boutique specialization trends that can affect fee structures and local markets.

Bottom Line

- Commercial leasing in premium pockets is providing tangible upside, but gains are uneven across markets and property types.

- Rising mortgage rates and HMBS/HECM liquidity and compliance issues pose real near-term risks for housing finance and related securities.

- Cross-border investor interest remains a stabilizer for U.S. CRE, supporting capital availability for top-tier assets.

- Be selective. Data suggests you should watch funding channels, rate moves, and leasing metrics before drawing conclusions about broader recovery.

- Analysts note this is a mixed environment where opportunities exist, but funding and policy shifts can change the outlook quickly.

FAQ Section

Q: How do rising mortgage rates affect commercial real estate? A: Rising mortgage rates primarily depress residential affordability and transaction volume, but they can indirectly affect commercial markets through investor demand shifts and higher borrowing costs for owners.

Q: What is HMBS liquidity and why does it matter? A: HMBS liquidity refers to how easily HMBS securities can be traded. If liquidity tightens, spreads widen and funding for HECM-originating lenders can become more costly or harder to access.

Q: Should I expect office leasing to recover broadly? A: Recovery appears selective. Premium, well-located assets and properties undergoing strategic repositioning are seeing demand, while secondary offices face continued headwinds.