The Big Picture

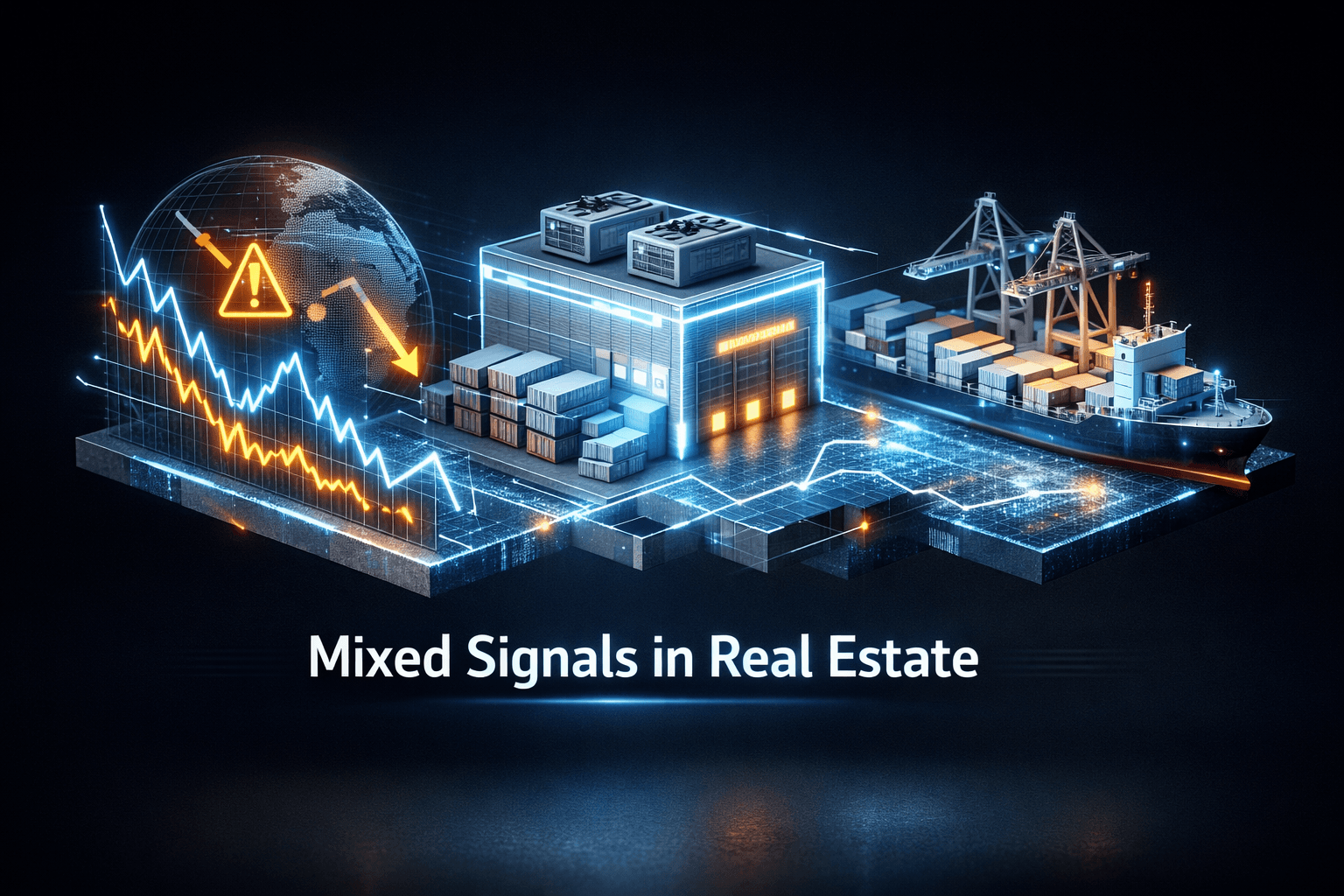

Real estate markets opened with a mix of signals this morning, as industry reports point to both resilience and fresh headwinds for investors. Cold storage users are chasing newer space even as deliveries hit record levels, while port cargo slipped only marginally despite trade policy uncertainty.

This matters because you need to balance sector-specific demand pockets against broader macro forces, including inflation, interest rates, labor and trade. The interplay of those factors will shape rents, absorption and cap rates in coming quarters.

Market Highlights

Quick facts and numbers from today’s reports, for investors who want the headlines at a glance.

- Cold storage: Newmark’s report finds absorption at about 3.5 percent in key markets, even as deliveries reached all-time highs and food inventories softened.

- Ports and trade: Cushman & Wakefield estimates cargo activity at ten major North American ports fell only 0.3 percent year over year, suggesting demand held up despite policy uncertainty.

- Macroeconomic watchlist: Marcus & Millichap senior VP John Chang flags four macro factors investors should track now, including inflation and rates, which remain central to CRE valuation.

- Notable industry names mentioned in coverage include Americold for cold storage, logistics landlord Prologis, and brokers such as Newmark, cited in the report; see company tickers $COLD, $PLD, $NMRK and broker commentary from Cushman & Wakefield $CWK.

Key Developments

Macro factors to track for CRE

Connect CRE summarizes a Marcus & Millichap take that says inflation, interest rates, labor markets and trade policy are the four macro levers CRE investors should be watching. Each affects cash flow projections and cap rate negotiation, and together they influence portfolio strategy.

Why should you care now? Because readings on inflation and yields determine financing costs and tenant affordability, and that in turn affects occupancy and rent growth across office, industrial and retail sectors.

Cold storage demand shifts toward newer facilities

Newmark’s cold storage report shows a split market. Occupiers prefer newer, high-spec facilities even as the sector faces an elevated level of new supply and softer consumer spending. Absorption was reported at roughly 3.5 percent, signaling continued leasing activity in selective markets.

For you that means location and specs matter more than ever. Temperature-controlled real estate with modern infrastructure is commanding a premium, while older stock may see longer vacancy spells.

Ports, trade policies and different investor responses

Cushman & Wakefield’s trade update notes that 2025 brought a slew of policy changes, but cargo volumes at ten major North American ports were down only 0.3 percent year over year. That muted decline suggests trade flows adapted, even if uncertainty prompted different strategies among owners and occupiers.

So what’s the implication? Port-adjacent industrial and intermodal assets remain strategically important, but investors and occupiers are taking divergent approaches to capex and lease terms as they hedge policy risk.

What to Watch

Here are the catalysts and risks that could move real estate names and valuations in the near term, and what you should monitor in your portfolio or watchlist.

- Macroeconomic data: Keep an eye on upcoming CPI prints and Fed commentary. Changes in inflation or rate outlook will influence cap rates and financing cost assumptions.

- Supply metrics for cold storage: Track monthly deliveries and absorption in major metros, plus food inventory trends. Data suggests newer, purpose-built facilities will outperform legacy assets.

- Trade and port throughput reports: Regular updates from port authorities and shipping indexes will show whether cargo volumes keep holding up or begin to decline more sharply.

- Earnings and guidance from key public names: Watch results and commentary from $COLD, $PLD and large logistics REITs for leasing trends and rent growth data that reflect real demand.

- Risks to monitor: elevated new supply in specific niches, sticky inflation that pressures operating costs, and tariff or policy shifts that alter trade flows.

Bottom Line

- Data suggests a mixed market, with pockets of resilience in cold storage and port-adjacent logistics, while macro uncertainty keeps underwriting cautious.

- Analysts note absorption in cold storage at about 3.5 percent even as deliveries accelerate, so you should focus on asset quality and location when evaluating exposure.

- Port cargo down roughly 0.3 percent year over year indicates trade flows have been resilient, but policy shifts could change that quickly.

- Watch inflation and rate signals closely, because financing costs remain a primary driver of valuations and cap rate movement.

- In short, take a selective approach, watch near-term data, and be ready to adjust assumptions if macro readings move unexpectedly; weather the storm by focusing on quality assets.

FAQ Section

Q: Which macro indicators matter most for commercial real estate now? A: Inflation, interest rates, labor markets and trade policy are the four primary indicators analysts cite because they affect financing, demand and operating costs.

Q: Is cold storage still a growth area? A: Yes, but growth is uneven; newer high-spec facilities are attracting occupiers while older inventory faces more vacancy, according to Newmark.

Q: Should I watch port throughput data? A: Absolutely. Port cargo volumes are a near-real-time indicator of trade demand and can signal changes for industrial real estate near logistics hubs.