The Big Picture

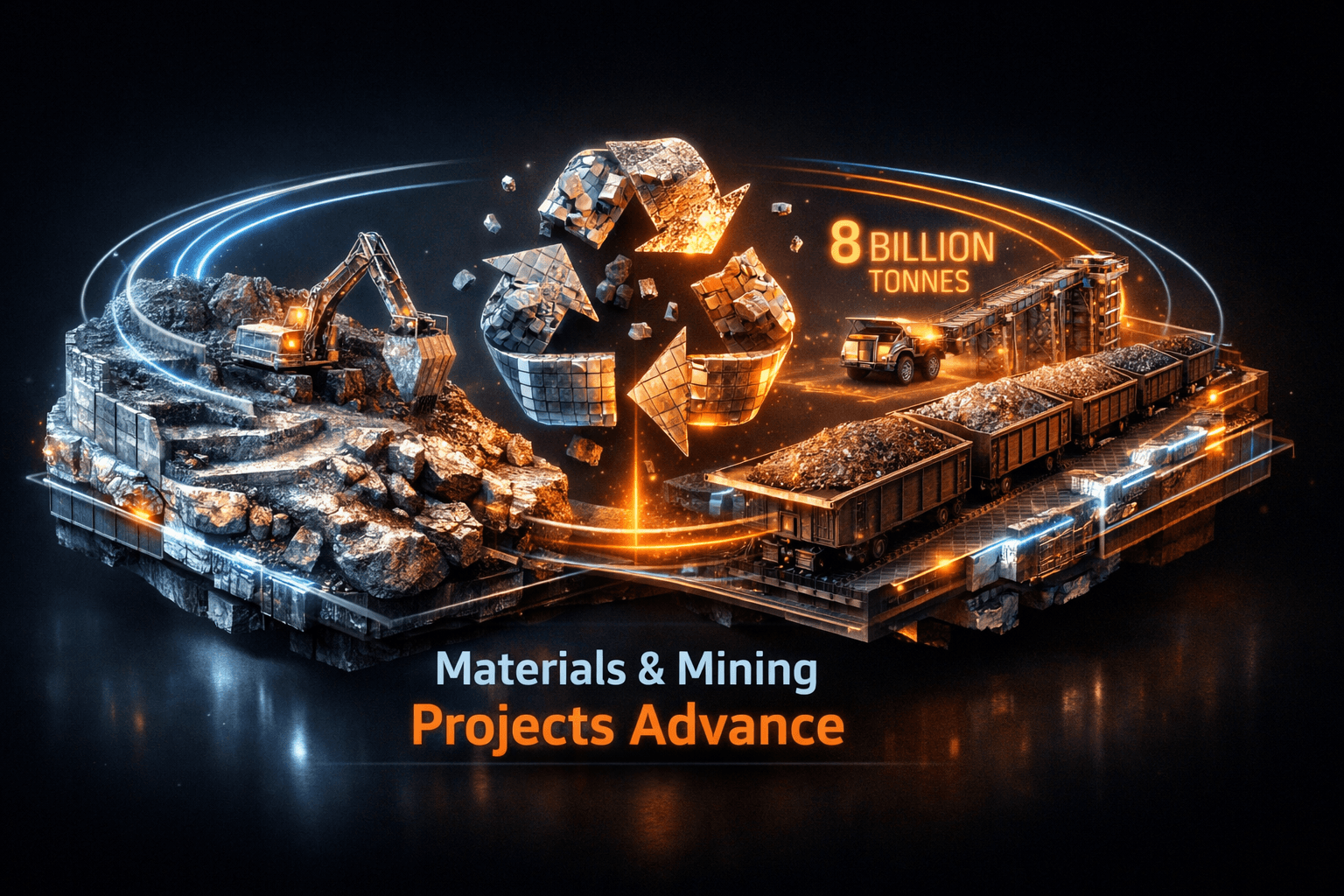

Core Lithium's start of mining at the Grants pit and Rio Tinto's eight-billionth tonne dispatch from Pilbara are the standout operational headlines this morning. These moves show project execution and steady production growth across key raw materials, and they matter because supply-side progress can influence pricing and investment flows in the weeks ahead.

At the same time you'll see technology and recycling advances aiming to ease material constraints, while junior exploration and metallurgical test wins keep the pipeline of future supply active. Taken together the news suggests momentum building across several parts of the materials chain, though you'll want to stay selective as markets absorb these updates.

Market Highlights

Quick facts to scan this morning.

- Core Lithium begins mining at the Grants open pit, part of the Finniss Lithium Operation in Australia, signaling first-stage production activity at the site, company reported.

- Rio Tinto marks a major milestone, dispatching its eight-billionth tonne of Pilbara iron ore to partner Nippon Steel, underscoring long-term scale of Australian iron ore exports.

- Kavango Resources completes metallurgical testing at its Hillside gold project in Zimbabwe, reporting significant test results that support the project's technical case.

- Recycling advances: Stena and partners report an improved method for separating wind turbine blade materials, which should boost blade recycling outcomes.

- Recycled steel prices in the United States remained essentially flat in May while steel output surged, leaving scrap markets poised for potential price adjustments in early June according to industry reporting.

- Commentary on copper highlights extreme volatility in the metal, a reminder that one key industrial input remains a major swing factor for manufacturers and miners.

- Legal note: The U.S. Department of Justice has filed charges alleging price fixing in new shipping containers, a development that could ripple into shipping and logistics costs for material flows.

Key Developments

Core Lithium starts mining at Grants

Core Lithium has commenced mining activity at the Grants open pit within the Finniss operation in the Northern Territory. This step moves the company from development to operations at Grants, a key component of its lithium strategy and supply contribution to battery markets.

For you that means an incremental source of hard-rock lithium entering the market, which could influence supply expectations for battery-grade spodumene later in the year.

Rio Tinto hits an eight-billionth tonne milestone

$RIO has dispatched its eight-billionth tonne of Pilbara iron ore, a milestone shipment bound for Nippon Steel. The figure highlights scale and longevity in iron ore supply from Australia to major steelmakers.

Volume milestones like this reinforce the structural role of major miners in seaborne iron ore markets, and they provide a measurable backdrop to demand-supply conversations for steelmakers and miners alike.

Recycling, metallurgical wins and exploration keep the pipeline active

Recycling and processing stories clustered around improved wind blade separation techniques and flat scrap prices versus rising steel output. Stena's progress on blade recycling could lower end-of-life disposal costs and recover more composite materials for reuse.

Kavango's metallurgical tests at Hillside returned encouraging results and Quantum Critical Metals reported a gallium-cesium discovery in Quebec at a recent industry symposium. These items show both near-term processing gains and longer-term exploration upside, so the sector is not just moving on production but on future feedstock and critical mineral fronts.

Meanwhile the DOJ's shipping container indictment is an outside-the-box risk that could feed through to logistics costs if it alters global container pricing and capacity over time.

What to Watch

Expect attention to follow the operational ramp timelines and market signals. Will Grants proceed to steady production on schedule and hit spodumene sales milestones? Watch Core Lithium's reported ramp metrics and shipment guidance for answers.

Iron ore demand indicators out of China will matter after Rio Tinto's milestone. Are seaborne volumes being absorbed or will inventory adjustments pressure prices? Keep an eye on Chinese steel output data and port inventories.

Scrap and steel dynamics deserve close monitoring. Scrap prices were flat in May even as steel output rose. If mills continue to step up production, scrap could firm in early June. How quickly that happens will shape margins for secondary steel processors and recyclers.

Copper volatility is another immediate risk for manufacturing chains. If you track industrial exposure, follow copper price moves, term spreads, and procurement signals because procurement teams are already feeling the effects of volatility.

Finally, watch regulatory and logistics headlines. The DOJ shipping container case could affect freight pricing and lead times. Also monitor any technical releases from Kavango and exploration drilling updates from juniors such as Quantum Critical Metals for possible re-ratings.

Bottom Line

- Operational progress is the dominant theme today, led by Core Lithium starting mining at Grants and $RIO's Pilbara milestone.

- Recycling and processing advances, including wind blade separation, support longer term supply resiliency and circularity in materials.

- Steel and scrap markets are showing a mixed bag, with flat scrap prices but rising output that could push scrap higher in early June.

- Copper remains volatile and could influence industrial sentiment and procurement costs in the near term.

- Keep an eye on logistics and legal developments, such as the DOJ container case, which could affect shipping costs for miners and processors.

FAQ Section

Q: What does Core Lithium starting mining at Grants mean for lithium supply? A: It signals a move from development toward production at that site, adding expected spodumene supply to the market later in the production ramp.

Q: Could flat scrap prices alongside rising steel output change steel margins? A: Yes, higher steel production with flat scrap pricing can pressure secondary margins if scrap tightens later, so watch scrap price direction into June.

Q: How should you follow copper and logistics risks? A: Track copper price volatility, procurement indicators, and shipping cost headlines because each can quickly affect input costs and margins across the materials chain.