The Big Picture

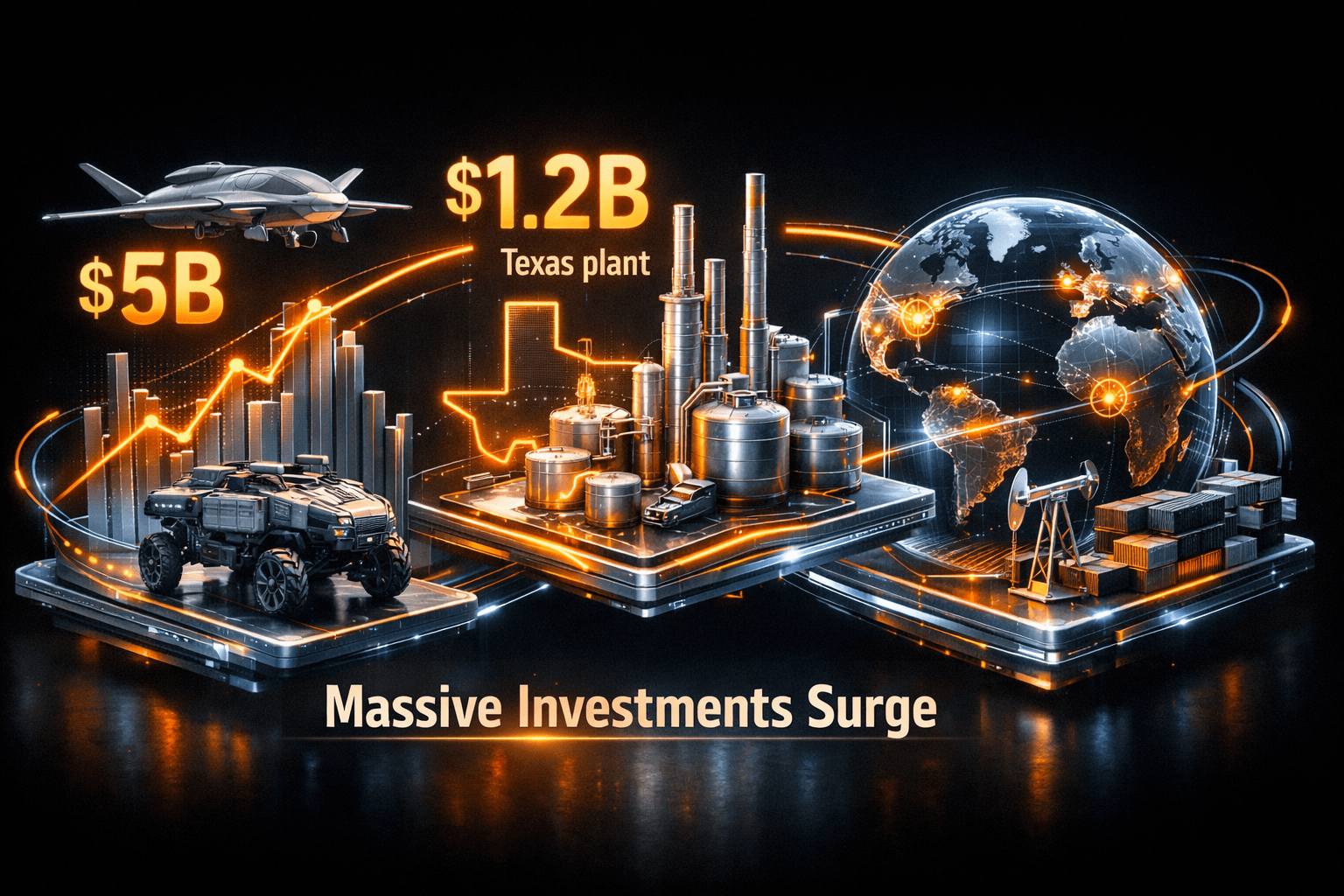

Today’s standout development was a wave of big capital commitments that underscore rising investment in U.S. manufacturing capacity. Anduril’s $5 billion financing and a $1.2 billion factory build by USG signal that companies and private capital are prioritizing onshore production and defense supply chains.

That momentum matters because it points to durable demand in defense and construction-related manufacturing, even as supply chain and geopolitical pressures keep costs and risks elevated. If you follow industrial names, you’ll want to weigh the near-term headwinds against these large, multi-year investments.

Market Highlights

Here are the quick facts from today’s top stories to keep on your radar.

- Anduril: Raised $5.0 billion and joined a multi-company agreement to help supply 10,000 missiles to the Defense Department over three years.

- USG ($USG): Announced a $1.2 billion investment in a new Texas factory in Orange, expected to create nearly 200 jobs and expand gypsum products capacity.

- NAM: The National Association of Manufacturers pushed for enhancements to the USMCA ahead of its six-year review, urging process improvements to favor U.S. manufacturing.

- O’Reilly ($ORLY): Broadening its private-label supply base to improve sourcing and product control amid emerging supply constraints.

- Packaging suppliers: Firms warned of Iran war-related disruptions and price pressures that may not normalize before 2027.

- USPS peak season report: Improvements in communication and processing were noted, though several services still fell short of targets.

Key Developments

Anduril’s $5B Raise and Missile Supply Agreement

Anduril secured $5.0 billion in financing and is part of a three-year consortium, with Leidos and other firms, to supply the Defense Department with 10,000 missiles. This is a rare, large private capital infusion aimed at scaling production and R&D quickly.

For investors watching defense supply chains, this looks like a bellwether moment for private-capital-led industrial scale-up. It should keep defense contractors and suppliers in focus, and it may accelerate subcontracting and component sourcing opportunities for public suppliers like Leidos $LDOS and other systems integrators.

USG Commits $1.2B to Texas Manufacturing

USG’s $1.2 billion expansion in Orange, Texas, aims to enlarge gypsum products capacity and create nearly 200 jobs. The project had been under consideration since early 2025 and represents a multi-year commitment to regional manufacturing capacity.

That kind of greenfield investment supports regional industrial ecosystems, and you’ll likely see follow-on activity in construction supply chains and local hiring. It also reinforces the trend that manufacturers are still willing to invest in U.S. footprint expansion despite cost pressures.

Supply Chain Strains, Tariffs and Policy Pushes

Several stories today highlighted ongoing supply and policy pressures. Plastic packaging suppliers warned that disruptions tied to the Iran war are driving price increases and that normal conditions may not return before 2027. Plant Engineering flagged tariff volatility as a material driver of sourcing and product-design decisions.

Meanwhile O’Reilly $ORLY is moving to broaden private-label sourcing to improve control amid those constraints. And the National Association of Manufacturers urged improvements to USMCA rules to make the pact more manufacturing friendly at its six-year review. Taken together, these items show firms and trade groups are adapting to a more complex global environment.

What to Watch

Expect capital spending and supply-chain resilience to be the dominant themes going forward. You should monitor near-term and medium-term catalysts that can move stocks in this group.

- Earnings and guidance from defense contractors and materials makers, where capital spending or margin pressure could appear in quarterly results.

- Follow-on contracting details from the missile agreement and any subcontract awards that could flow to public suppliers such as $LDOS.

- USG’s permitting and construction timeline, plus local hiring data that will indicate how quickly production ramps.

- Geopolitical developments tied to the Iran war and any new sanctions or shipping disruptions that would affect polymer and packaging inputs.

- Policy updates around USMCA and tariff actions, because trade rules can change sourcing economics and product design choices for manufacturers.

How will companies balance investing while managing higher input costs? Watch guidance and capital-expenditure commentary closely to get a read on priorities.

Bottom Line

- Major capital commitments like Anduril’s $5B raise and USG’s $1.2B plant are bullish signals for industrial capacity and defense-related manufacturing.

- Supply pressures from geopolitical conflict, particularly in plastics and packaging, pose material cost and delivery risks through at least 2027.

- Companies are responding by reshaping supply strategies, for example O’Reilly’s $ORLY private-label push and broader supplier diversification efforts.

- Trade policy and tariff volatility remain wildcards; NAM’s USMCA recommendations underscore industry desire for clearer, manufacturing-friendly rules.

- Watch earnings, contract awards, and project timelines for the clearest signals on how these stories translate into revenue and margins.

FAQ Section

Q: How will Anduril’s $5B raise affect public defense suppliers? A: Analysts note the funding may accelerate production and subcontracting, which could benefit component suppliers and systems integrators that win work under consortium agreements.

Q: What does USG’s $1.2B plant mean for regional manufacturing jobs? A: The project is expected to create nearly 200 jobs and expand local gypsum products capacity, supporting suppliers and construction-related demand in the area.

Q: How long will supply disruptions from the Iran war last? A: Industry sources suggest price and delivery pressures could persist into 2027, so companies are adjusting sourcing and inventory strategies accordingly.