The Big Picture

Manufacturing momentum shows up in both corporate investment and sectorwide activity, but policy and cost pressures are keeping the outlook mixed for you as a retail investor. Today’s standout items were $CAT's major capacity expansion and new Senate legislation to tighten Buy America enforcement, balanced by fresh trade friction and rising input prices.

Why this matters, and why you should pay attention, is simple: demand-driven investments and adoption of AI could lift productivity, yet tariffs and supplier strains can squeeze margins and shift where production happens. That combination means selective opportunity, not a uniform rally or rout.

Market Highlights

Quick facts to scan before you dig deeper.

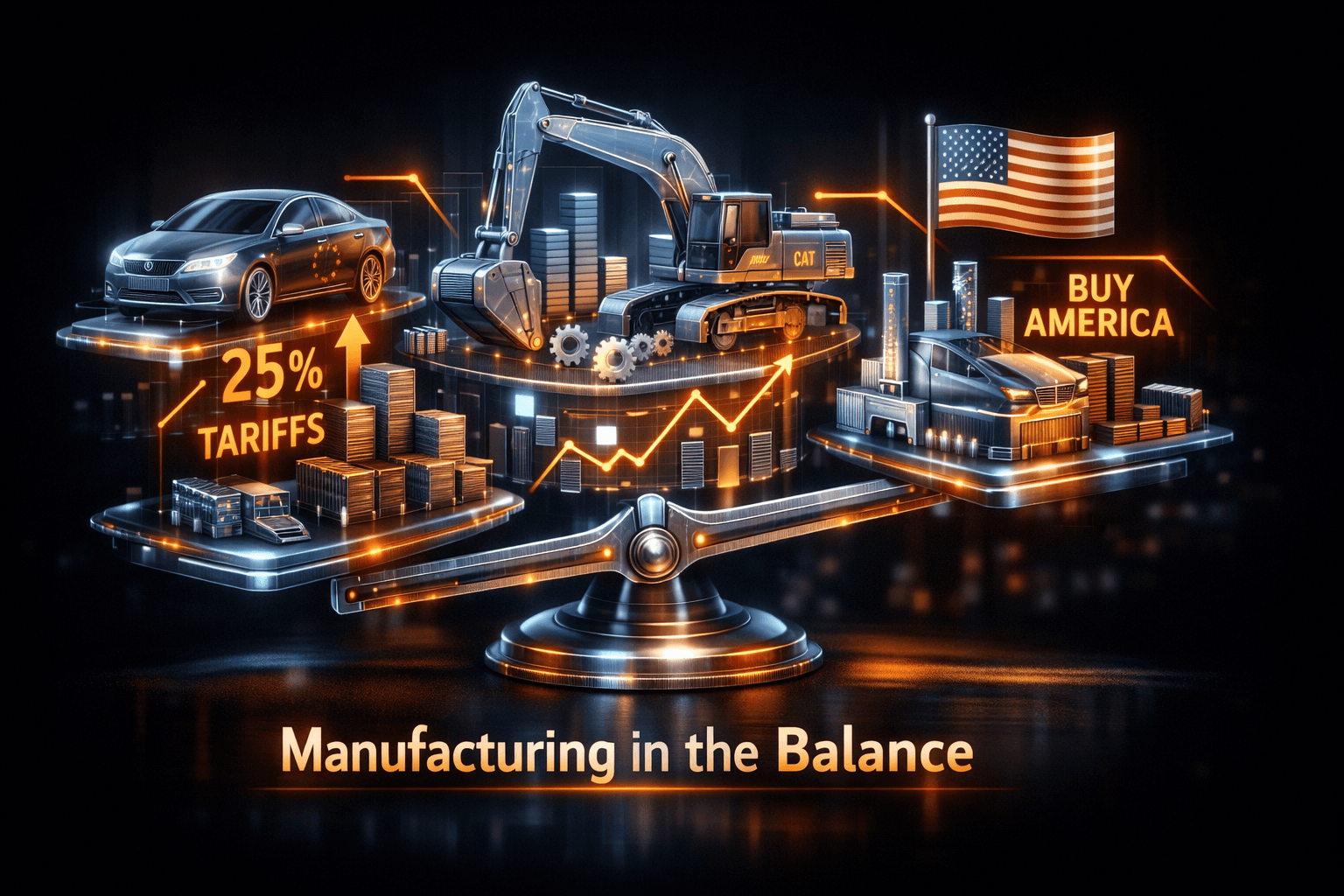

- Caterpillar $CAT said it will triple power generation capacity and raised its 2030 targets, citing data center and oil and gas demand.

- The Senate introduced a bill to enforce Buy America clauses after an OIG audit found the FAA omitted required Buy America language in IIJA-funded contracts.

- The White House announced a planned 25% tariff on EU cars and trucks, saying the bloc is not complying with a recent trade agreement.

- ISM data showed manufacturing expanded for a fourth consecutive month, while all six largest manufacturing industries reported price increases in April.

- Moody’s warned that software-defined vehicles could raise input costs and strain supplier relationships, a notable headwind for $F, $GM and $TSLA supply chains.

- Plant Engineering highlighted growing AI and ML use in heavy-asset industries, which could shift capital spending and operating models over time.

Key Developments

Senate pushes Buy America enforcement

Lawmakers introduced legislation aimed at enforcing Buy America requirements after an Office of Inspector General audit found the FAA failed to include buy-local clauses in contracts funded by the Infrastructure Investment and Jobs Act. That oversight prompted the bill, which would tighten compliance and reporting across IIJA programs.

For domestic manufacturers this could raise near-term demand for U.S.-made components and create more predictable contract pipelines, but it may also increase certification and administrative work for suppliers. If you follow suppliers with large federal contract exposure, you'll want to watch how agencies implement new rules.

Caterpillar bets on power generation growth

Caterpillar $CAT announced plans to triple its power generation capacity and raised its 2030 targets, pointing to stronger demand from data centers and oil and gas customers amid higher energy prices. The move signals confidence in long-cycle equipment spending and in markets that need resilient on-site power solutions.

This is a clear growth signal for heavy-equipment and industrial OEMs, and it ties into AI and automation narratives in plants and energy management. You may see increased aftermarket and service revenue for companies tied to heavy-asset deployment over the next several years.

Auto sector faces tariffs and software-driven complexity

The administration's plan to impose a 25% tariff on EU cars and trucks introduces immediate trade risk for automakers and suppliers that rely on transatlantic production. That policy could accelerate nearshoring or shift sourcing strategies, and it raises the cost of certain imported vehicles for U.S. consumers.

At the same time, Moody's noted that software-defined vehicles, which use updatable platforms and more complex software stacks, can increase input costs and stress supplier relationships. So you have trade policy on one side and structural cost increases on the other. What does that mean for margins and capital allocation at auto suppliers? It points to selective winners and losers depending on scale, software capability and supply flexibility.

What to Watch

Here are the catalysts and risks to track over the next week and quarter so you can stay prepared.

- Legislative and regulatory timelines for the Buy America enforcement bill, and agency guidance on IIJA contract clauses. That will affect federally related supply chains.

- Implementation details and exemptions for the announced 25% tariff on EU autos. Watch comments from auto OEMs and parts makers for supply-shift signals.

- Quarterly earnings from major industrials and auto suppliers for updated margin commentary and capital spending plans, especially any follow-up from $CAT's announcement.

- ISM follow-ups and inflation gauges, since price increases are persistent across industries. You should monitor supplier margin trends and passthrough ability to end customers.

- Technology adoption milestones for AI and ML in heavy-asset operations, including pilot results, cost savings, and productivity metrics from plant-level deployments.

Bottom Line

- Sentiment is mixed: corporate investment and AI adoption show upside, while tariffs and rising input costs create headwinds.

- Buy America enforcement could boost demand for U.S.-made parts, but will raise compliance work and could reshape supplier contracts.

- $CAT's capacity expansion signals strong equipment demand in power and energy markets, potentially benefiting OEMs and service providers.

- Auto sector risk is elevated because of a 25% tariff on EU imports and structural cost increases from software-defined vehicles.

- Stay selective, separate the wheat from the chaff, and watch regulatory and earnings updates that will determine near-term winners.

FAQ Section

Q: How will Buy America enforcement affect U.S. suppliers? A: It should increase demand for American-made components in federally funded projects, but it may also add compliance costs and contract administration for suppliers.

Q: Will the 25% EU auto tariff raise car prices here? A: Tariffs typically increase landed costs for imports, and some of that can be passed to consumers, though OEMs may alter sourcing or pricing strategies to limit passthrough.

Q: Can AI and ML meaningfully cut industrial costs soon? A: Data suggests pilots are producing predictive maintenance and efficiency gains, but broad rollout takes time and capital; you should watch measurable ROI reports from early adopters.