The Big Picture

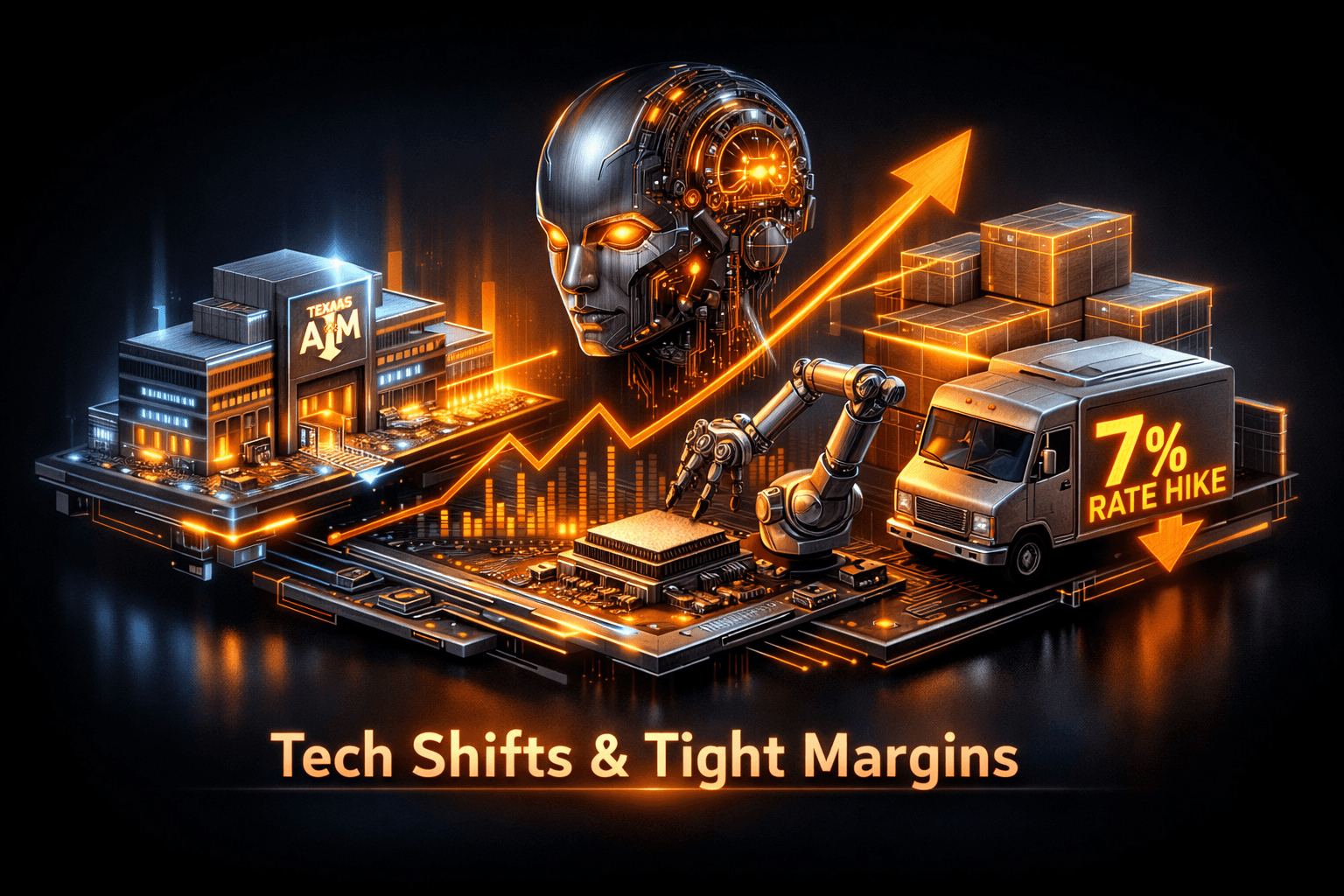

Texas A&M’s announcement of a $226 million Semiconductor Institute is the day’s biggest development, signaling continued public and private momentum behind domestic chip R&D and talent pipelines. That investment matters because it helps funnel federal and state CHIPS Act dollars into university-driven commercialization and could accelerate supplier partnerships and workforce development in the region.

At the same time you saw technology adoption and logistics moves that point to structural change across manufacturing operations, yet geopolitics and higher shipping rates are creating near-term cost pressure. What does this mean for your exposure to industrial names? It suggests a selective approach, as opportunity and risk are appearing side by side.

Market Highlights

Key facts and figures that shaped the sector today.

- Texas A&M breaks ground on a $226 million Semiconductor Institute, part of the state-level CHIPS initiative meant to attract investment and expand academic-industry collaboration.

- Manufacturers are piloting physical AI and robotics in testing centers run by Deloitte, Tata Consultancy Services and $MSFT among others, as firms look to validate automation before large capital outlays.

- Packaging supply chains remain strained by tariffs and the Iran war, and many consumer packaged goods companies say near-shoring all sourcing isn’t feasible.

- $NSC expanded local switching operations via a partnership with Jaguar Transport Holdings to boost freight capacity for truck-to-rail shippers at a Georgia facility.

- $FDX is raising One Rate prices in April, with increases generally around 7 percent, a development that will matter to shippers and manufacturers with tight margins.

Key Developments

Texas A&M Semiconductor Institute: a long-term industrial bet

The $226 million facility is designed to fund semiconductor R&D, training and collaboration with industry partners. For you that means a clearer pipeline for skilled graduates and an R&D hub that could attract suppliers and startups, especially as states compete for CHIPS Act-related projects.

Analysts note that university-led facilities often serve as anchors for regional ecosystems, but commercialization and supply-chain integration take time. Expect multi-year implications rather than immediate revenue shocks for listed chip suppliers.

Physical AI pilots and systems modernization

Manufacturers are increasingly using neutral testing centers to trial robots, vision systems and closed-loop automation before committing to full deployments. $MSFT and large consultancies are part of that trend, offering environments that simulate factory floors and logistics flows.

If you follow capital expenditure themes, this reduces implementation risk and may accelerate adoption. Data suggests firms that test first tend to see faster ROI and fewer disruption events during rollout.

Supply-chain strain: tariffs, conflict and shipping costs

Packaging supply chains are being reshaped by tariff policy and the Iran war, making simple near-shoring impractical for many CPGs. Companies are adopting blended sourcing strategies, more flexible supplier contracts and inventory buffering instead of single-country reshoring.

At the same time $FDX’s One Rate price rises, roughly 7 percent, will squeeze margins for firms that can’t pass costs to consumers. How will manufacturers absorb higher shipping costs, and will price increases slow demand? Those are open questions that could affect margin outlooks this quarter.

What to Watch

Near-term catalysts and risks that will drive headlines and moves in the sector.

- CHIPS Act follow-through and state-level incentives, including partnership announcements and grant recipients tied to the Texas A&M build. Watch for vendor deals and supplier commitments that signal ecosystem scale.

- Physical-AI pilot outcomes and adoption rates. You should monitor case studies released by testing centers and early adopters for evidence of productivity gains and payback timelines.

- Shipping and logistics cost trends, including carrier pricing moves beyond $FDX and contract renewals that will come up in supplier negotiations. Shipping price volatility is a key margin risk.

- Geopolitical developments tied to tariffs and the Iran conflict. Any escalation could force further supplier rerouting and inventory cost increases for packaging and CPG companies.

- Rail and local switching partnerships similar to the $NSC–Jaguar deal. Additional capacity agreements could relieve bottlenecks, but execution matters.

Bottom Line

- Major public investments like Texas A&M’s $226M center boost long-term capacity and R&D, but benefits arrive over years, not weeks.

- Testing-first approaches to physical AI and modern systems are reducing implementation risk and may accelerate productivity improvements for manufacturers.

- Geopolitical friction and higher carrier pricing, with $FDX’s One Rate up about 7 percent, create real near-term margin pressure for packaged-goods suppliers.

- Rail partnerships that expand switching capacity are positive for freight flow, analysts note, though they're not a complete fix for broader logistics stress.

- Overall the sector shows mixed signals, so a selective approach is warranted as you evaluate exposure to industrial and manufacturing names.

FAQ

Q: How will the Texas A&M semiconductor center affect supply chains? A: The center should strengthen the local talent pipeline and R&D collaboration, which can attract suppliers over time, but it will not instantly resolve component shortages.

Q: Will higher FedEx One Rate pricing directly hit manufacturers? A: Yes, manufacturers and shippers that rely on parcel services will likely see higher logistics costs, and some will try to pass those costs to retailers or consumers.

Q: Should I expect faster automation adoption after these testing initiatives? A: Testing centers aim to lower deployment risk, so adoption could speed up for firms that validate ROI. You should look for published pilot results to assess timing.