The Big Picture

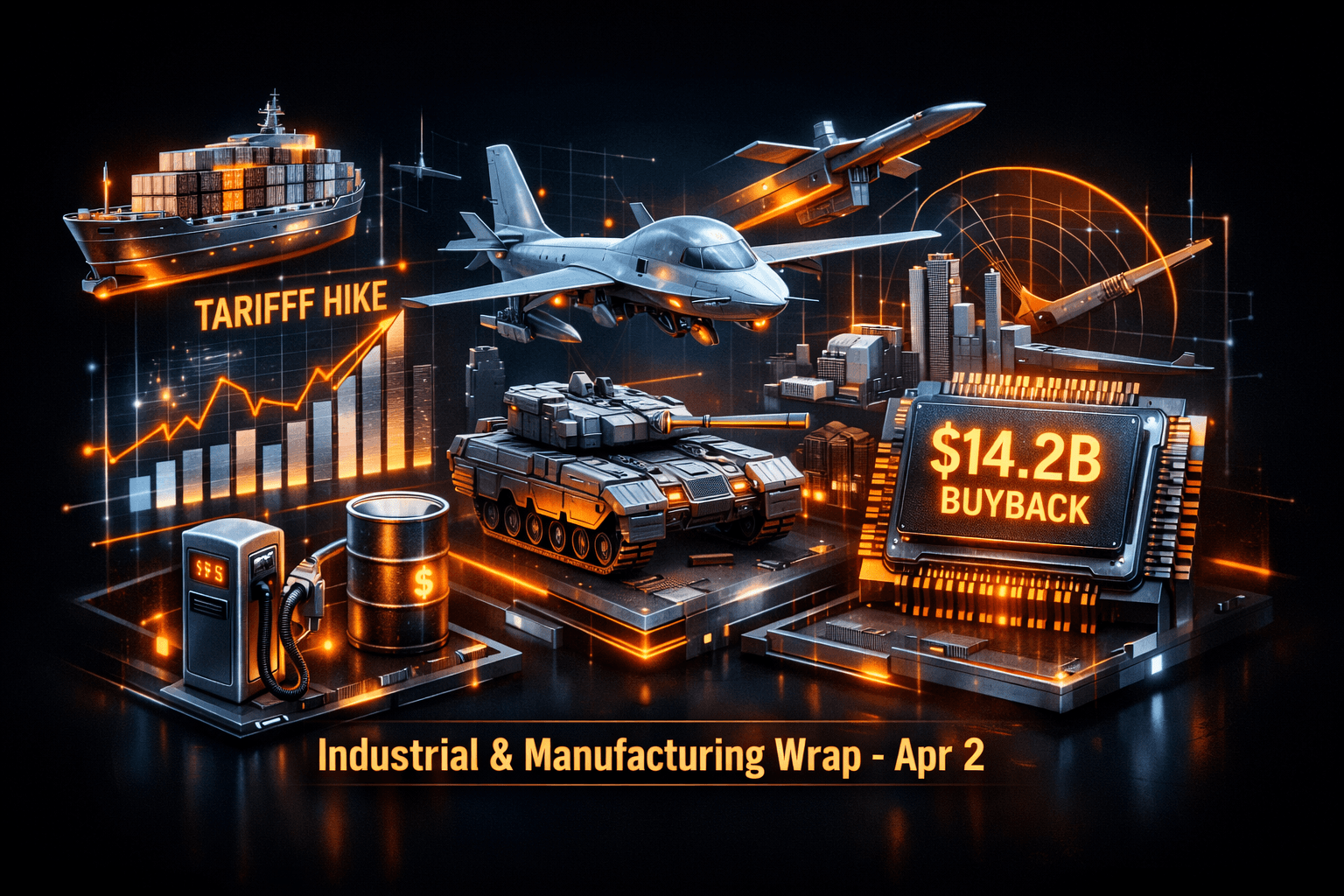

President Trump's tariff adjustments for steel, aluminum and copper dominated the headlines today, with new rules keeping a 50 percent levy on goods made entirely of those metals but cutting the rate to 25 percent for certain derivative products, effective April 6. That policy shift matters because it changes input cost math for a broad set of manufacturers and suppliers starting next week.

At the same time you saw demand-side and capital moves that offset the policy noise. Defense contractors including $BA, $LMT, $BAESY and $HON are ramping production after recent meetings with the administration, and $INTC is spending $14.2 billion to repurchase Apollo's stake in an Ireland chip fab. The net picture is mixed, so you'll want to be selective about where you look for durable upside.

Market Highlights

Key facts and numbers to digest from today:

- Tariff update: goods entirely made of steel, aluminum or copper remain at a 50 percent tariff, while certain derivative goods will see the levy reduced to 25 percent, effective April 6.

- $INTC agreed to pay $14.2 billion to buy back Apollo's stake in the Ireland fab, signaling heavier capital and operational control over Fab 34.

- Defense firms including $BA, $LMT, $BAESY and $HON reported new agreements with the Defense Department as production ramps amid the U.S.-Israel conflict with Iran.

- Diesel: California on-highway diesel averaged about $7.22 per gallon today, roughly 35 cents higher week over week, keeping transportation costs elevated.

- Retail signal: Williams-Sonoma said it is not planning to factor tariff refunds into 2026 guidance, suggesting retailers expect tariff uncertainty to persist.

Key Developments

Tariff Adjustment, Effective April 6

The administration's move preserves maximum protection on pure metal goods with a 50 percent levy, while trimming the rate to 25 percent for derivative items. For manufacturers that import semi-finished or fabricated components the change offers some cost relief, but raw producers and downstream firms that rely on fully metal-made goods will still face heavy levies.

What does this mean for you as an investor? Expect margin pressure to ease for some supply-chain exposed firms, but many companies told analysts they still plan for elevated input costs. How companies adapt pricing and sourcing will determine winners and losers.

Defense Production Ramps After Administration Meetings

$BA, $LMT, $BAESY and $HON signed deals with the Defense Department as part of a broader push to increase weapons output. These contracts should boost near-term backlog and provide revenue visibility for aerospace suppliers and parts makers.

Investors watching the defense supply chain should monitor order cadence and subcontractor capacity, since larger primes will need suppliers to scale quickly to meet higher output targets.

Intel Repurchases Stake in Ireland Fab, While Fuel and Retail Signals Tighten Margins

$INTC's $14.2 billion repurchase of Apollo's interest in the Ireland facility marks a strategic pivot back toward full operational control of chip manufacturing assets. That move signals commitment to capacity and could accelerate equipment orders across the semiconductor ecosystem.

At the same time diesel costs remain a drag on logistics margins, and Williams-Sonoma's comment that it won't assume tariff refunds in 2026 highlights ongoing retail caution. Taken together, the news suggests higher demand in pockets, while cost headwinds persist elsewhere.

What to Watch

Monitor these near-term catalysts and risks that will shape industrial sector earnings and supply chains.

- April 6 implementation of the tariff changes, which could produce immediate cost and pricing moves across import-reliant names.

- Defense order flow and subcontractor capacity updates, including production timetables from $BA and $LMT, which will indicate how quickly revenue ramps translate to supplier profits.

- $INTC guidance and subsequent capital spending plans, since fab consolidation often triggers equipment and services purchases across suppliers.

- Diesel and freight cost trends, especially in California where on-highway diesel sits near $7.22 per gallon. Rising fuel directly affects margins for manufacturers with heavy shipping footprints.

- Retail earnings updates and commentary on tariff impacts, given Williams-Sonoma's decision not to expect refunds in 2026. Which retailers update their assumptions next?

Bottom Line

- Tariff policy shifts provide partial relief but leave significant levies in place, so cost pressure will persist for many manufacturers.

- Defense contracts are a clear demand bright spot, creating near-term backlog for primes and suppliers.

- $INTC's $14.2 billion repurchase signals renewed capital commitment to manufacturing and could lift equipment and supplier demand over time.

- Elevated diesel and freight costs are an active margin risk, with California showing particularly acute pressure.

- Stay selective, watch April 6 for immediate pricing changes, and track order flow and guidance from large primes and chipmakers for clues about durable momentum.

FAQ Section

Q: How will the April 6 tariff change affect manufacturers? A: The cut to 25 percent for certain derivative goods eases input costs for some firms, but a 50 percent levy still applies to goods made entirely of metals, so impacts will vary by supply-chain exposure.

Q: Should I expect faster profit recovery from defense contractors? A: Analysts note additional contracts boost backlog and revenue visibility, but supplier scaling and execution will determine profit recovery speed, so watch production updates closely.

Q: Will $INTC's repurchase change chip supply dynamics? A: The buyback gives Intel greater control of capacity, which may accelerate capital spending and benefit equipment suppliers. Data suggests effects will unfold over quarters, not immediately.