The Big Picture

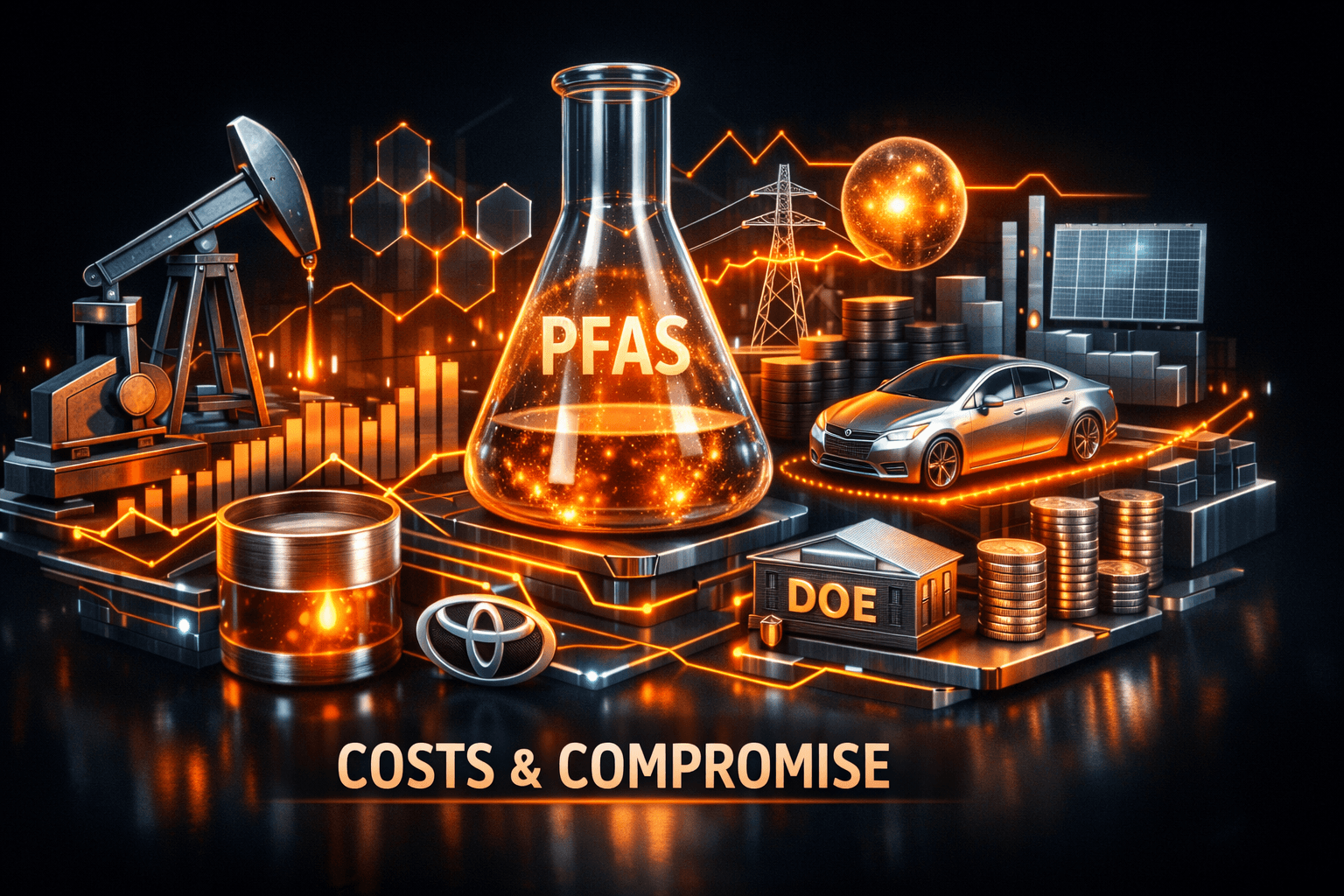

The Industrial & Manufacturing sector closed the day with mixed signals that leave short-term risks elevated but longer-term investment momentum intact. Sharp commodity-driven input-cost spikes and renewed PFAS regulatory pressure are pressuring margins, while $1 billion in fresh Toyota investment and a $500 million DOE program aim to shore up U.S. capacity.

If you follow supplier chains or industrial names, today’s developments matter because they affect both costs and where capital flows next. How large a hit to margins could this be, and which companies will adapt fastest?

Market Highlights

Price action and company moves today reflected the dual forces of cost inflation and strategic re-shoring. Here are the quick facts to keep on your radar.

- Tightening commodity costs: crude oil has surged about 47% so far this month, while polypropylene prices jumped roughly 24%, pressuring plastics, packaging and transport costs across the sector.

- Toyota investment: $TM is investing another $1 billion in U.S. manufacturing, part of a broader $10 billion five year commitment focused on Kentucky and Indiana facilities.

- Retail chain inventory move: $DG cut roughly 1,500 SKUs to simplify its supply chain and boost in-stocks, a sign retailers are leaning into leaner assortments.

- Rail opportunity: Norfolk Southern CEO Mark George noted that higher fuel costs could lift intermodal and coal volumes, a potential tailwind for $NSC freight volumes.

- Federal support: the Energy Department unveiled a $500 million program to scale critical minerals production, with $50 million to $100 million targeted at projects that support advanced battery manufacturing.

Key Developments

PFAS accountability bill resurfaces

Democratic lawmakers reintroduced a bill to ban nonessential uses of PFAS and expand reporting and recordkeeping requirements for manufacturers, building on Minnesota's Amara's Law. For you that track compliance exposures, this means companies using PFAS in components or coatings face heightened regulatory and disclosure risk and may need to accelerate substitution or remediation plans.

Commodity shock from Strait of Hormuz closure

Manufacturers are bracing after crude climbed roughly 47% this month and polypropylene rose about 24%, following disruption in the Strait of Hormuz. Higher energy and petrochemical costs will hit transportation and plastics-heavy supply chains first, squeezing margins for producers and assemblers until either inputs or prices normalize.

Capital and policy support offsets some headwinds

Toyota's additional $1 billion commitment to U.S. plants, part of a $10 billion plan, reinforces onshoring trends and could support regional suppliers in Kentucky and Indiana. At the same time, the Energy Department's $500 million program, including $50 million to $100 million for battery supply projects, aims to reduce critical minerals bottlenecks that have constrained EV and battery manufacturing capacity.

What to Watch

Expect volatility as you monitor input costs and policy developments. Oil and petrochemical price moves will be the immediate transmission mechanism to margins and procurement plans.

Key near-term catalysts:

- Further developments on the PFAS bill and any state-level enactments, which could change compliance timelines for manufacturers.

- Weekly oil inventories and shipping updates tied to the Strait of Hormuz, which will influence crude and feedstock price direction for plastics and chemicals.

- DOE funding announcements and award recipients, which will indicate which domestic projects and regions receive priority for critical minerals and battery supply chain buildouts.

- Retail and logistics signals from chains like $DG and freight carriers like $NSC, which will show whether inventory discipline is amplifying or easing demand for suppliers.

Which suppliers will feel the pinch most, and which will benefit from nearshoring and federal dollars? Watch margins, backlog and guidance updates in earnings that arrive next few weeks for answers.

Bottom Line

- Sentiment is neutral overall, because fresh investment and federal funding offset meaningful near-term cost and regulatory headwinds.

- Rising oil and petrochemical prices are the biggest immediate risk to margins across plastics, packaging and transportation exposed firms.

- New PFAS regulation raises compliance risk and potential replacement costs for manufacturers using these chemicals.

- Toyota's $1 billion U.S. spend and DOE’s $500 million program support longer term capacity and supply chain resilience.

- If you track industrial names, focus on companies' input-cost pass through, inventory strategy and exposure to PFAS and petrochemical inputs.

FAQ

Q: How will higher oil and polypropylene prices affect manufacturer margins? A: Higher oil and polypropylene raise input and transport costs, squeezing gross margins until companies can pass costs to customers or find cheaper inputs.

Q: What does the PFAS bill mean for manufacturers? A: The proposed ban on nonessential uses and expanded reporting would increase compliance work, could raise substitution or remediation costs, and will likely accelerate product reformulation for affected producers.

Q: Will Toyota and DOE funding offset cost pressures? A: Capital investments from $TM and federal funding can support regional capacity and long term resilience, but they are unlikely to fully offset near-term margin pressure from rising commodity costs.