The Big Picture

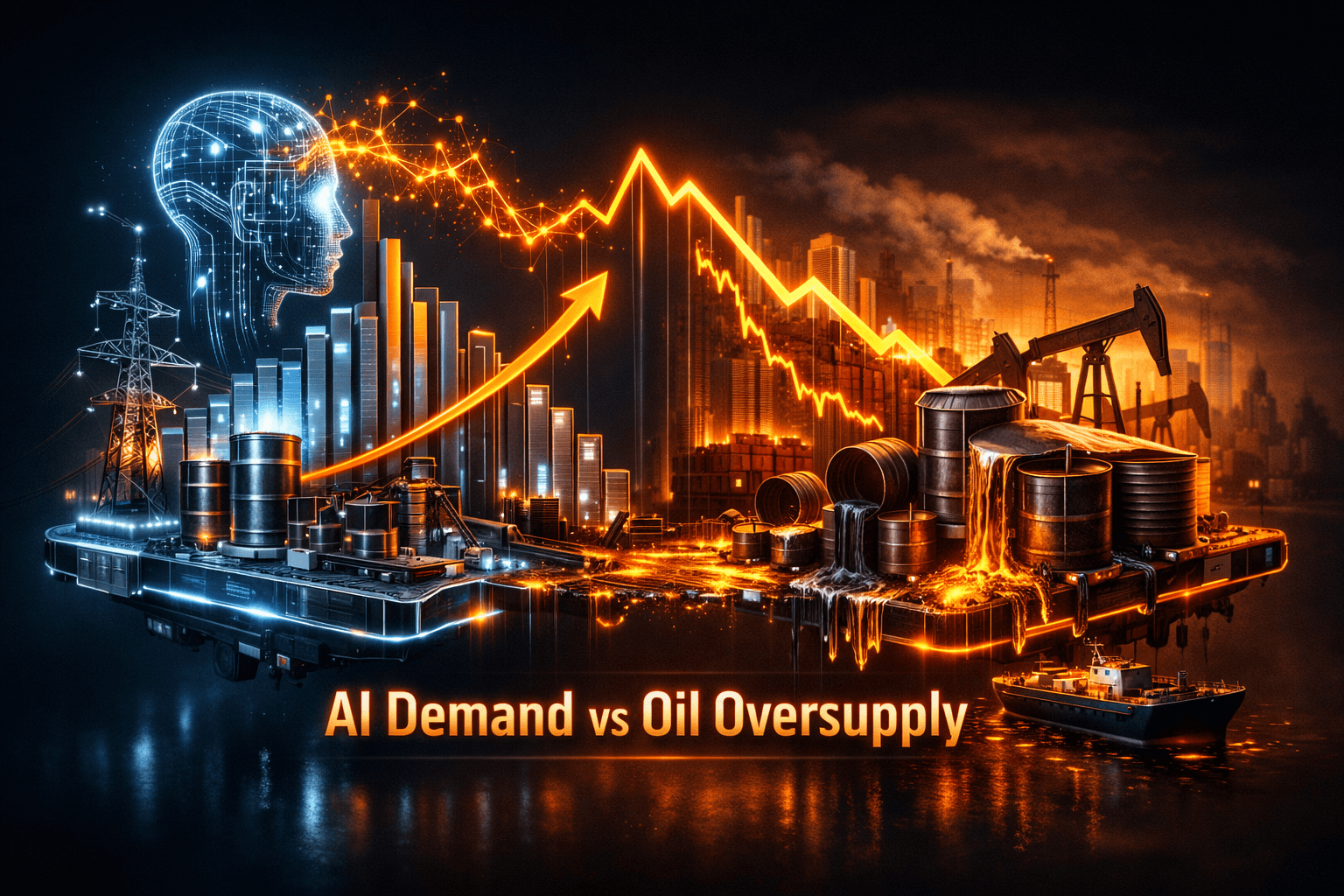

Markets were closed Sunday, June 28, but the weekend brought a clear tug of war for energy investors. On one side you have a surge in demand for power and infrastructure tied to AI and electrification. On the other side traditional oil markets face oversupply and legacy basin decline.

Why should you care? What happens next will influence power grids, commodity prices, industrial capex and clean-energy supply chains. With the next US trading day on Monday, June 29, you should be thinking about which trend will matter most for your positions.

Market Highlights

Quick facts and numbers to keep in mind as you prepare for the week.

- AI infrastructure boom: analysts and commentators have put the long-term AI infrastructure market in the multi-trillion dollar range, with headlines citing a $7 trillion AI boom and roughly $5+ trillion in required infrastructure investment.

- Company spotlight: Bitzero, cited as a play on AI power needs, trades as $AIBZ. The story frames it as an early mover in data-center power and infrastructure.

- Oil and shipping: crude prices fell sharply late Friday as Strait of Hormuz traffic increased and Persian Gulf exports rose, pressuring nearby benchmarks.

- Legacy field depletion: the U.S. Geological Survey estimates the Buda Limestone under the Eagle Ford has about 184 billion cubic feet of technically recoverable gas remaining, indicating constrained upside in one of Texas's oldest plays.

- Autos and EVs: Wall Street delivery consensus for $TSLA in Q2 2026 sits at 406,024 vehicles, about 5.7% growth year over year. Mercedes data on electric semis and new EV models like the Jeep Recon from $STLA highlight continued focus on EV commercialization.

- Panama Canal: operators expect revenue to exceed a $5.2 billion forecast for fiscal 2026 after rerouting caused by disruptions in the Strait of Hormuz.

Key Developments

AI Infrastructure is a Power Story

Weekend coverage framed AI as not just a software or chip mania but a massive physical build-out for power, cooling and data centers. Industry voices point to trillions in infrastructure needs and highlight companies positioned to solve power chokepoints.

For you that means opportunities tied to grid upgrades, industrial power providers, and data-center energy solutions could see sustained demand. Analysts note this is a structural tailwind, but it plays out over years rather than overnight.

Oil Market: Gulf Flows and a Depleting Basin

Crude fell late Friday after reports that Strait of Hormuz traffic and Persian Gulf exports rose, easing some short-term supply worries that arose earlier in the month. Rigzone coverage flagged a notable move lower in oil on the news.

At the same time the USGS analysis showing the Buda Limestone is largely tapped points to slower domestic growth from a long-standing Texas play. Put together, these items create near-term price pressure while tightening some regional long-run supply assumptions.

Clean Energy, EVs, and Grid Realities

China's growing dominance in clean-energy manufacturing is a recurring theme. Coverage shows Beijing controls large parts of solar panel and battery supply chains, and Chinese exports are expanding rapidly. That matters if you're watching manufacturing margins and global supply pricing.

On the demand side, Mercedes shared real-world efficiency data from electric semis hauling 36 tons, and a UK study found heat pump performance can improve materially with better commissioning. Those trends support electrification of transport and buildings, but grid warnings such as the UK supply alert show reliability will need to keep pace.

What to Watch

Here are the catalysts and risks that could move energy names when markets re-open on Monday.

- Oil fundamentals and geopolitics: watch Gulf export volumes and any new Iran-related shipping news. Oil price direction will hinge on flows through the Strait of Hormuz and OPEC statements.

- Announcements on AI data-center deals and utility capex: any large-scale build or corporate power purchase agreements will reinforce the AI-power narrative. You should scan company releases for new contracts.

- China export and tariff news: policy moves that affect solar and battery exports can change cost dynamics for developers and automakers worldwide.

- Grid stress signals: UK supply warnings and regional reliability notices are a reminder that electrification ramps will require investment in grid flexibility. Follow utility guidance and regulator statements.

- EV delivery and product updates: $TSLA delivery figures and new model launches from $STLA and others will shape investor expectations for EV demand and battery needs.

Ask yourself, are you positioned for rising power demand or a calmer oil market? Which of these trends matters most to your exposure?

Bottom Line

- Neutral near term: AI and electrification are powerful structural drivers, but oil oversupply and competitive clean-tech manufacturing from China create offsetting pressure.

- Power and grid names could benefit from multi-year AI-related capex, yet grid reliability and commissioning quality will affect realized gains.

- Legacy oil basins face depletion in some plays while global flows can push prices lower, so commodity-focused juniors may see pressure.

- Watch shipping and logistics, including Panama Canal revenue trends, as they signal demand shifts and freight cost impacts.

- Be selective and follow catalysts closely, since short-term moves will depend on geopolitics, corporate deals and supply-chain shifts.

FAQ Section

Q: How does the AI boom affect energy companies? A: Data centers and AI farms increase demand for reliable power, so utilities, grid service providers and companies that supply power systems could see higher long-term capex and demand.

Q: Should I worry about oil prices falling after Gulf supplies rose? A: Short-term price moves can be volatile and tied to shipping flows. Longer term, depletion in older fields can tighten supply, so both short and long factors matter.

Q: Does China’s dominance in clean-energy manufacturing change the investment landscape? A: Yes, lower-cost Chinese exports put pricing pressure on global manufacturers but they also accelerate deployment of renewables and storage, which can boost project development and service providers.