The Big Picture

Today the Energy sector served up a classic mixed bag, with long-term gas supply deals and a North Sea discovery standing up against cooling Asian crude demand and a sharp slide in lithium futures. You saw moves across oil, gas, metals and renewables that left the overall tone balanced rather than directional.

Why this matters to you is straightforward: the market is reacting to both structural shifts and near-term trade flows. That combination is creating selective opportunities and risks, so your lens needs to be specific to assets and themes, not the sector at large.

Market Highlights

Quick facts and numbers that defined the day.

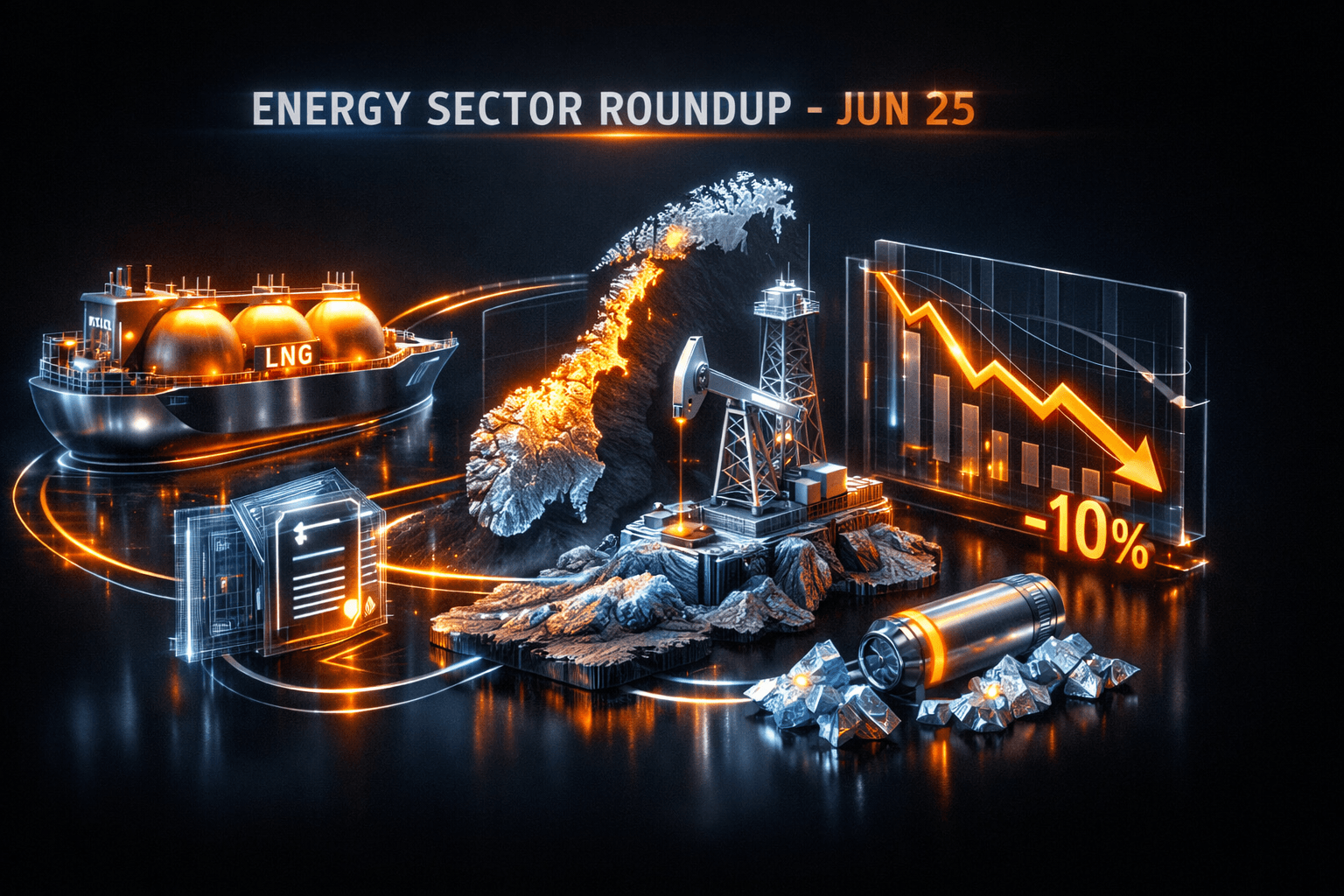

- Lithium futures in China fell about 10% over two sessions, down to roughly 157,000 yuan per tonne, about $23,175 per tonne, as traders anticipate a CATL supply surge.

- Vitol inked a 20-year LNG supply deal to deliver 1 million metric tons per annum to International Resources Holding, highlighting long-term gas commitments.

- Wellesley confirmed a gas and condensate find in the Norwegian North Sea with preliminary recoverable resources of 21 to 107 million barrels of oil equivalent.

- Asian refiners scaled back spot purchases of Middle East crude for July and August loading after a three-week buying spree, citing Strait of Hormuz navigation concerns and high freight costs.

- SpaceX filed to build an eight-mile natural gas pipeline to its Starbase launch site, expected online by January, to fuel Starship methane needs.

- Automakers and EV news: Range Rover’s upcoming EV may top $150,000, and EV-related product rollouts and Prime Day green deals continue to spotlight consumer adoption trends.

Key Developments

Asian Crude Demand Eases

After three weeks of aggressive spot buys from UAE, Saudi and Iraqi sellers, Asian refiners have pulled back on new spot purchases for July and August. The pullback stems from freight costs and lingering questions over Strait of Hormuz navigability, and it means near-term physical demand for Middle Eastern barrels is softer than it was earlier this month.

For you that raises a question, how long will spot demand remain muted and what will that mean for prompt oil prices? Traders and refiners will watch freight and geopolitical signals closely in the coming sessions.

LNG: Long-Term Contracts and Midstream Moves

Vitol’s new 20-year, 1 million metric ton per annum LNG agreement with International Resources Holding reinforces the appetite for long-dated gas supplies. The deal highlights that buyers are locking supply to manage volatility and secure feedstock for industrial demand.

SpaceX’s planned eight-mile pipeline to Starbase shows another facet of demand, where a single large consumer is vertically integrating midstream supply to secure methane for rocket launches. These developments point to steady structural demand for LNG and natural gas infrastructure.

Battery Metals and EV Supply: Price Shock and Capacity Signals

Lithium carbonate futures plunged roughly 10% after reports that CATL may restart its large Jianxiawo mine. Lower lithium prices relieve cost pressure for battery makers, but they also squeeze margins for upstream producers and miners.

Analysts note that the move is meaningful for majors involved in lithium, such as $ALB, $LTHM and $SQM, and it may change investment timelines for new mining projects. If prices stay lower, it could slow upstream capex while supporting EV battery cost deflation for automakers.

What to Watch

Tomorrow and the coming days will be about confirmation and flow. You should track a few specific catalysts and risks.

- Freight rates and Strait of Hormuz updates. Continued shipping disruptions or easing will materially affect crude prompt markets and refinery procurement patterns.

- Lithium supply confirmations from CATL and official permits or reopenings. More evidence of restarted capacity could keep downward pressure on prices and affect miner earnings.

- LNG contracting headlines and cargo nominations. Watch for more long-term deals or spot cargo movements that could shift regional gas balances.

- Wellesley and other exploration updates in the North Sea. Appraisal results will determine whether the discovery moves toward development.

- Policy moves on biofuel blending quotas in the U.S. House. A repeal push could change demand outlooks for ethanol and biodiesel and affect refiners and biofuel producers.

Which of these will move markets most? That depends on fresh news flow, and you’ll want to scan headlines and data releases early tomorrow.

Bottom Line

- Energy headlines today were mixed, with long-term LNG deals and a North Sea find counterbalanced by softer Asian crude buying and a sharp lithium decline.

- Lithium’s 10% drop could ease battery costs but will pressure miners and shift project economics; watch $ALB, $LTHM and $SQM for analyst commentary.

- Vitol’s 20-year LNG deal and SpaceX’s pipeline plan underline durable structural demand for gas and midstream infrastructure.

- Policy risks around U.S. biofuel rules add near-term uncertainty for refiners and biofuel producers, so regulatory headlines matter for pricing.

- This article is for informational purposes only and does not constitute investment advice. Analysts note these developments, and data suggests selective, not broad, positioning is warranted.

FAQ

Q: What does a 10% drop in lithium futures mean for EV battery costs? A: A sizable drop in lithium carbonate lowers a key input cost for batteries, which can ease pressure on automaker margins and support lower battery pack prices if sustained.

Q: Will reduced Asian spot buying push oil prices sharply lower? A: Softer spot purchases weigh on prompt oil balances, but broader crude prices also depend on OPEC supply decisions, freight rates and geopolitical risks.

Q: How important are long-term LNG contracts like Vitol’s deal? A: They lock supply and revenue over decades, reducing short-term price volatility for buyers and underpinning investment in liquefaction and shipping capacity.