The Big Picture

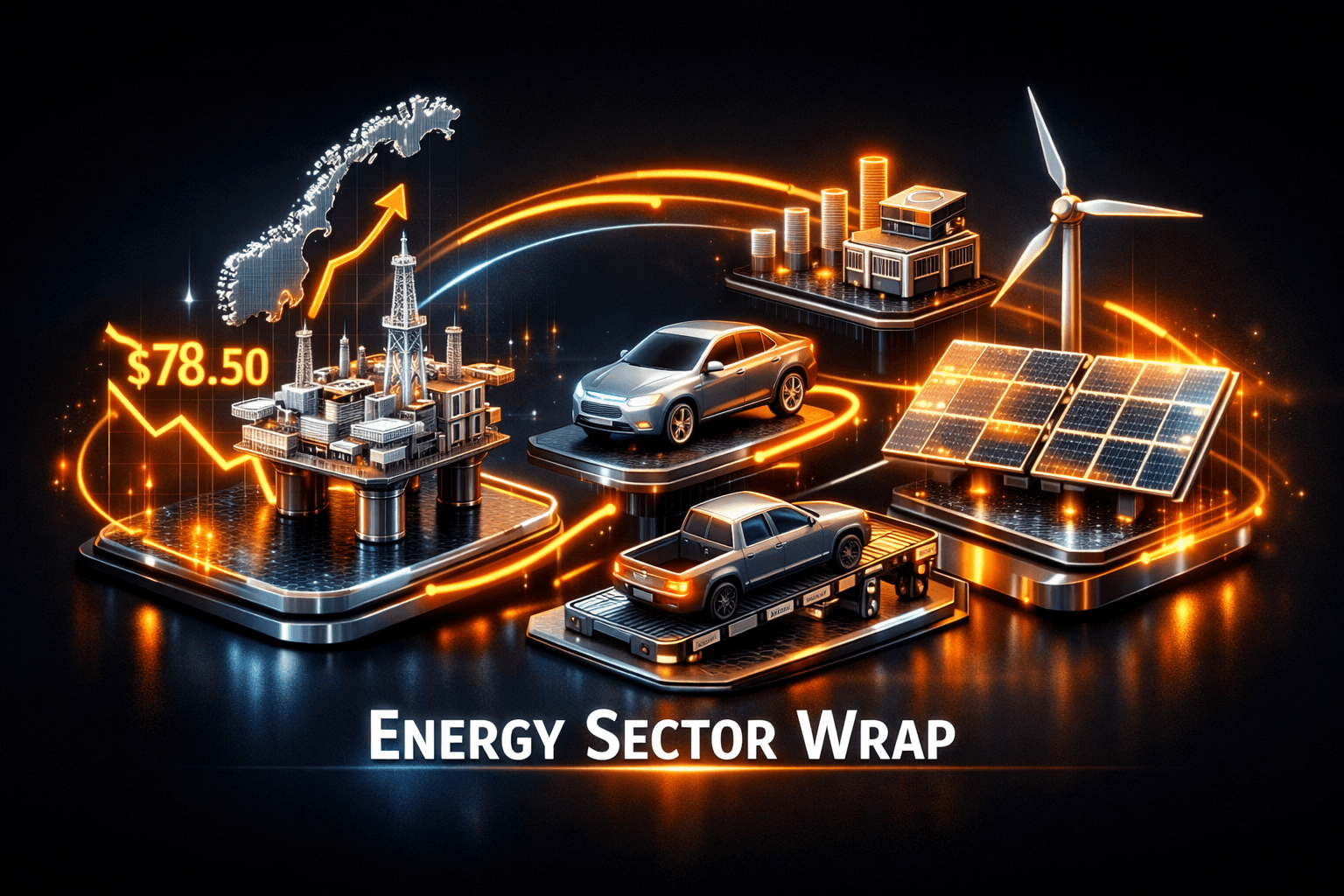

Today brought a mixed bag for the energy complex, with a major geopolitical development sending oil prices sharply lower while industry players pushed ahead on long-term projects and clean-energy manufacturing. Brent crude traded below $79 a barrel after a U.S.-Iran agreement to reopen the Strait of Hormuz, and that near-term supply relief is colliding with longer-term moves to extend production and expand clean-energy capacity.

That combination matters because your exposure to the sector will be tested by price volatility in the near term and structural shifts over the next several years. You need to weigh shorter-term demand signals against strategic investments in renewables and energy infrastructure.

Market Highlights

Key market moves and quick facts from today.

- Brent crude fell below $79 per barrel, its lowest level since March, after the United States and Iran digitally signed a peace agreement that includes reopening the Strait of Hormuz.

- Norway's Equinor says new discoveries support Phase 4 development at the Johan Sverdrup field, with preliminary resources around 20 million barrels of oil and roughly 30 million barrels of oil equivalent, production targeted to start in 2029, $EQNR.

- Rivian confirmed layoffs affecting several hundred staff, under 2% of its workforce, a week after R2 deliveries began, $RIVN.

- BYD unveiled a detachable magnetic smart device that lets owners control their EV remotely, an incremental consumer feature that could affect customer experience, $BYDDY.

- China's refining throughput hit its lowest level in nearly four years in May, raising questions about fuel demand recovery even as shipping lanes reopen.

- Hundreds of offshore well workers in Norway went on strike, a potential short-term disruption to services and maintenance on North Sea platforms.

Key Developments

Norway advances Johan Sverdrup Phase 4

Equinor and partners are moving forward on a new phase of the Johan Sverdrup development, citing newly discovered volumes that should extend field life. The preliminary resource estimates are modest by super-giant standards, about 20 million barrels of oil plus 30 million barrels of oil equivalent, with production expected in 2029.

For investors, this is a reminder that producers are still investing in mid-life field extensions to sustain production and cash flow. It won't offset major price swings, but it supports the oil supply base in Europe over the medium term.

Oil rout after Hormuz agreement

Traders reacted decisively to the U.S.-Iran agreement intended to reopen the Strait of Hormuz and return Iranian oil to markets. The selloff pushed Brent to its lowest level since March, as the market priced in eased shipping risk and a likely increase in short-term supply.

Will demand keep pace? That's the question markets face now. Weak Chinese refining and structural demand shifts from electrification mean prices could stay sensitive to signs of recovery or further supply disruptions.

EVs and renewables: BYD, Rivian and Solarge

In EV land, BYD announced a detachable magnetic device that enhances remote control and convenience for drivers. It's a product-level win for consumer experience, but not a game changer for fleet economics.

Rivian's layoffs, small as a percentage of staff, come as the company begins R2 deliveries and seeks a path to profitability. On the clean manufacturing front, Solarge's automated PV module plant in the Netherlands highlights a push for lightweight, recyclable modules, something you should watch if you're following the solar supply chain.

What to Watch

There are several near-term catalysts and risk factors that will shape the sector over the coming days and months.

- Oil price volatility, inventory data, and shipping updates: monitor weekly EIA and IEA reports and any developments around Hormuz patrols and demining plans from G7 partners.

- Norway labor actions: strike developments among offshore well workers could affect maintenance schedules and output in the near term, so track union talks and service-company announcements.

- Project timelines: Johan Sverdrup Phase 4 targets 2029, meaning capital allocation and sanctioning milestones will be worth watching for $EQNR and partners.

- EV makers' execution: Rivian's post-launch staffing moves and delivery cadence for the R2 will be key metrics to follow for $RIVN, and you should watch upcoming production and cost guidance.

- Demand signals out of China: refining throughput trends and monthly consumption figures will tell you whether transport electrification or cyclical weakness is driving lower fuel demand.

Bottom Line

- Energy markets are sending mixed signals, with geopolitical de-escalation pushing prices down even as producers extend field life and renewables add capacity.

- Short-term risks center on price volatility and labor disruptions, while medium-term themes include electrification, solar manufacturing scale-up, and project sanctioning.

- You're likely to see continued headline-driven swings. Be selective and keep an eye on earnings, supply updates, and policy decisions that affect infrastructure planning.

- Analysts note that structural demand change and regional policy will matter as much as near-term supply moves, so balance your view between cyclical and secular drivers.

FAQ Section

Q: How will the Hormuz deal affect oil prices? A: The agreement reduced immediate shipping risk and prompted a decline in Brent below $79, suggesting markets expect more supply to return in the near term.

Q: Should I worry about offshore strikes in Norway? A: Strikes can create short-term service and maintenance delays that affect timing of output, but they don't usually cause long-term production losses unless they escalate.

Q: Is BYD’s new device a material business driver? A: The magnetic control device improves customer experience and product differentiation, but it is more of a consumer feature than a major revenue driver for the company.