The Big Picture

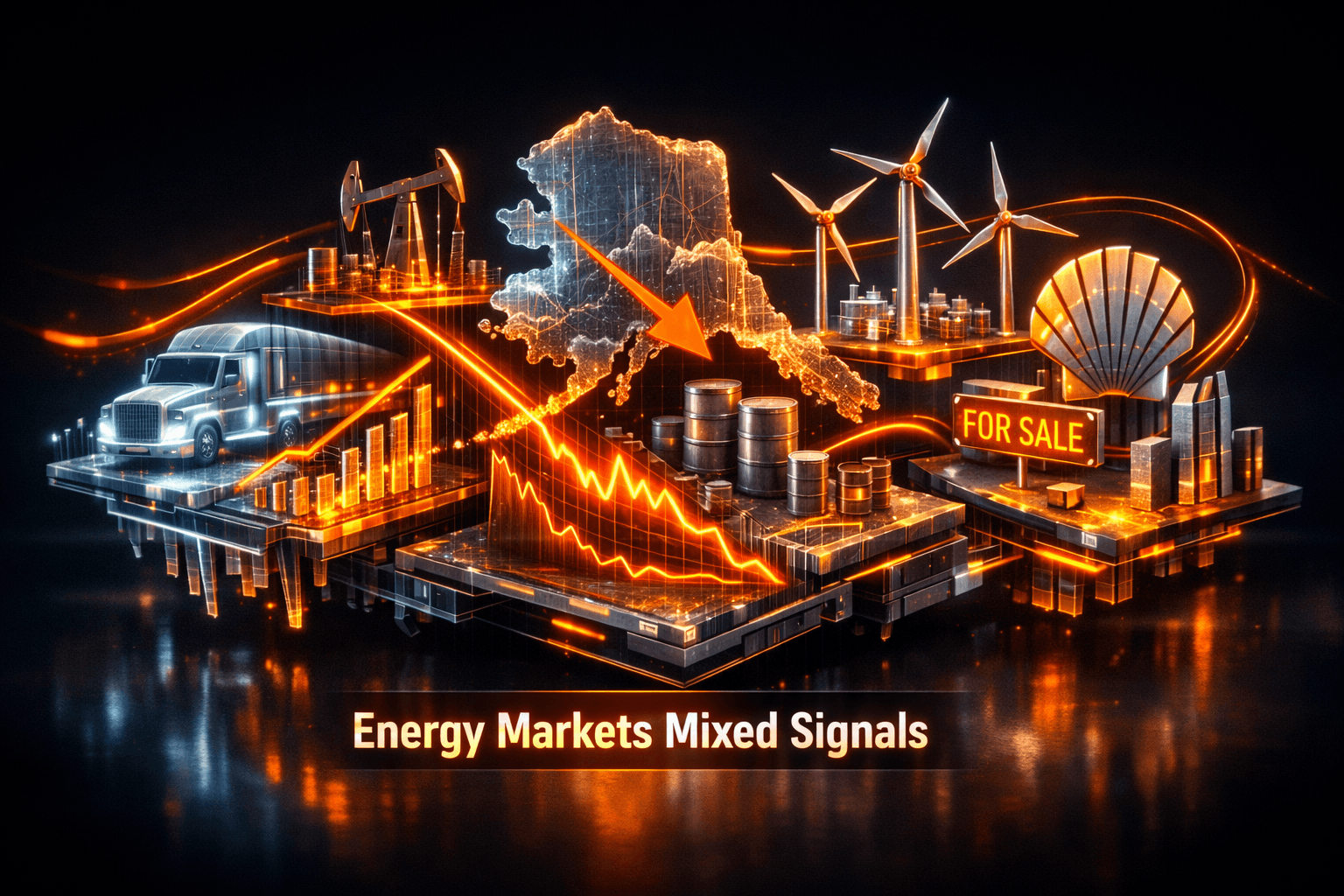

A string of contrasting stories left the energy outlook balanced rather than bullish or bearish. You saw demand-side momentum in electrified freight while traditional oil faces weaker near-term pricing and uneven investor interest.

That mix matters because it sets a selective backdrop for energy portfolios heading into Monday, Jun 15. Will majors pivot toward deals while renewables take a breather, or will low oil prices keep buyers cautious?

Market Highlights

Key facts and quick takeaways to watch as markets reopen on Monday.

- Scania/Traton: A 105-unit order of battery-electric semis from Wibax highlights growing demand for heavy-duty EVs, linked to Traton's Scania business, noted here as $TRATF.

- Oil: Prices dropped to a four-month low as of Friday, Jun 12, after reports of progress on a US-Iran reopening agreement affecting Strait of Hormuz risk sentiment.

- Shell: $SHEL is reportedly preparing to sell offshore wind assets in a deal around $1 billion, signaling a tactical pullback from some renewables investments.

- Exxon: $XOM has held early-stage talks about acquisitions including Australia’s Woodside, cited as $WDS, suggesting majors are exploring consolidation.

Key Developments

EV Trucks Gain Traction

Scania scored a "landmark" order of 105 battery-electric semis from bulk transporter Wibax. This is tangible demand for heavy EVs rather than pilot projects, and it underlines fleet electrification progress in Europe.

For you that means equipment makers and fleet tech players may see a clearer revenue runway if orders scale. Keep an eye on suppliers and fleet operators that supply charging, telematics and maintenance services.

Oil Weakness, Alaska Interest Lags, and M&A Buzz

Oil slid to a four-month low as of Friday, Jun 12, helped by diplomatic hopes around the Strait of Hormuz. At the same time Alaska’s recent auctions drew limited investor interest despite federal policy shifts and strong resource potential.

Those two dynamics help explain why $XOM is reportedly exploring acquisitions including $WDS. Majors may test M&A to secure reserves and returns while spot prices remain subdued. So what does this mean for you? It suggests strategic deal activity could pick up, but near-term price pressure adds execution risk.

Renewables Rebalance and Local Pushback on Waste-to-Energy

Shell’s planned $1 billion sale of offshore wind farms points to tactical portfolio reshaping, prioritizing higher-return oil and gas assets. Investors will want to separate company-level strategy from the health of the broader renewables sector.

At the same time Fiji’s rejection of an Australia-backed waste-to-energy incinerator shows local political and environmental pushback can stall energy-from-waste projects. Policy and permitting remain key risk factors for alternative energy developers.

What to Watch

Focus on catalysts and risks that will move the sector when US markets reopen on Monday.

- Oil price drivers, as of Friday, Jun 12: Monitor any firm confirmations on US-Iran discussions and supply disruptions that could reverse the recent four-month low.

- M&A headlines: Track any formal moves by $XOM or peers toward $WDS or other asset targets, since early-stage talks can accelerate quickly into bids.

- EV adoption signals: Look for additional fleet orders following Scania's 105-unit sale and for charging infrastructure contract announcements that could benefit suppliers.

- Policy and permitting: Watch for updates on Alaska leasing, and local opposition to waste-to-energy projects, because regulatory outcomes will affect project financing and timelines.

- Labor and build capacity: The AI and grid pieces story underscores a workforce bottleneck for electrification and grid buildouts. How will the sector fill those blue-collar gaps?

Do you need to reposition? That depends on your timeframe and risk tolerance. If you're focused on short-term market moves, oil volatility and M&A chatter matter immediately. If you have a multi-year horizon, electrification and workforce constraints will be more relevant.

Bottom Line

- Sentiment is mixed: tangible demand in electric heavy transport sits beside lower oil prices and uneven investor appetite for frontier projects like Alaska.

- $TRATF’s Scania order of 105 EV semis is a clear demand signal for fleet electrification, and you should watch related suppliers and charging infrastructure providers.

- $SHEL’s planned $1B wind sale and Fiji’s rejection of a waste incinerator show renewables and alternative projects face strategic and political headwinds, even as some majors seek better returns.

- $XOM’s early-stage acquisition talks, including potential interest in $WDS, indicate majors may pursue consolidation to secure reserves and returns while oil prices stay soft.

- Analysis is informational only. This article doesn't recommend buying, selling, or holding any security. Analysts note the landscape is mixed and you should monitor catalysts and risks before acting.

FAQ Section

Q: How should I interpret the oil price drop as of Friday, Jun 12? A: Oil’s slide to a four-month low reflects reduced geopolitical risk and soft near-term demand signals. Watch for any follow-up diplomatic news or supply disruptions that could move prices.

Q: Does Scania’s 105-truck order mean the EV truck market is ready? A: The order shows commercial-scale interest and deployment, but widespread adoption still depends on charging infrastructure, total cost of ownership and fleet economics.

Q: Will Shell’s reported wind sale hurt renewable momentum? A: It signals a tactical shift at one major toward higher-return assets, but broader renewable demand and policy support remain in place. Project-level outcomes will vary by region and developer.