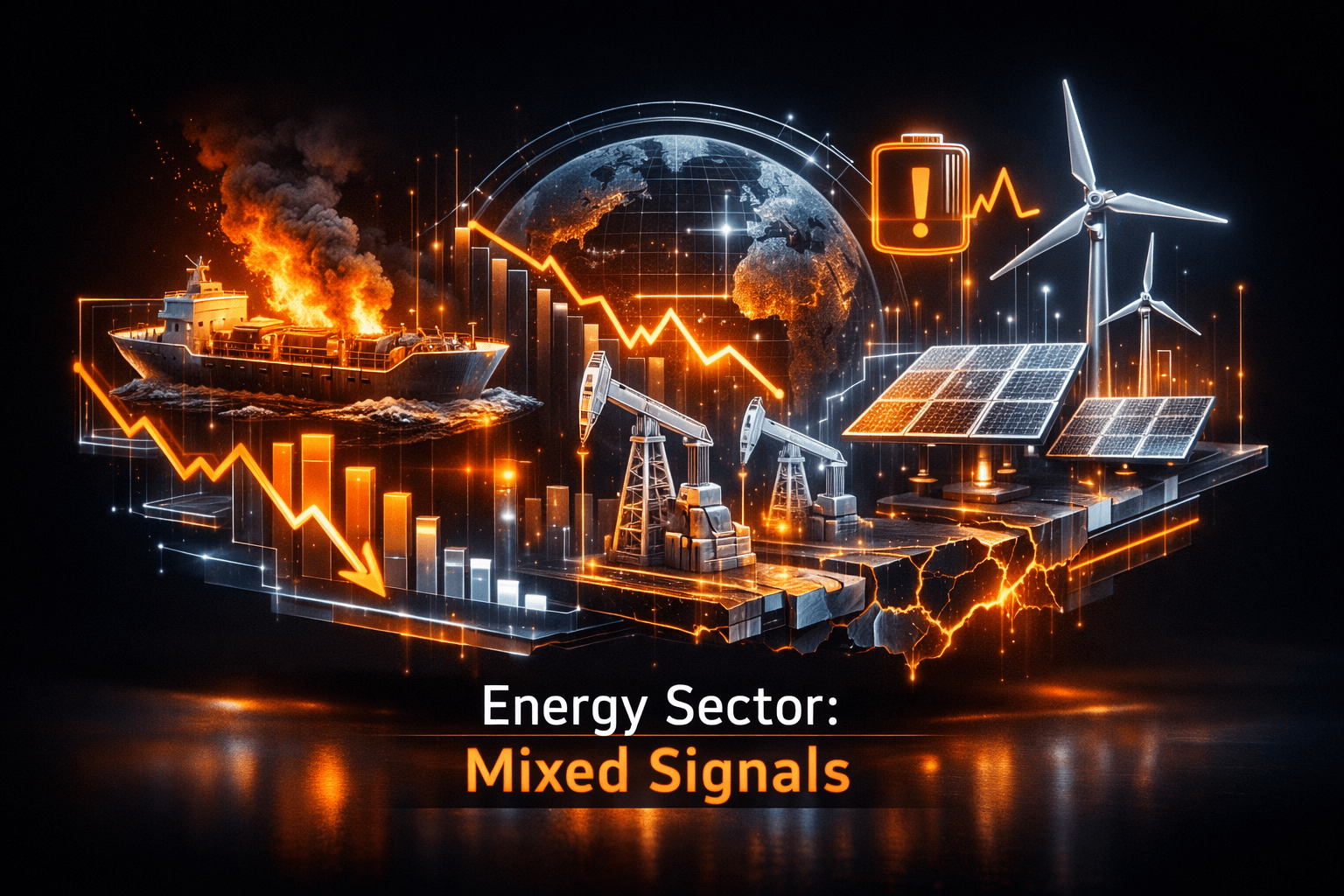

The Big Picture

Oil prices pushed higher today amid geopolitical tension and a maritime incident, but the broader Energy story is a mixed bag for investors. Short-term supply risk is supporting prices, while major agencies and industry data point to weaker capital spending that could reshape the sector over the next year.

That divergence between price action and investment plans matters for you because it affects where value, volatility, and opportunity may appear. Are energy companies planning for higher prices, or are they trimming back for structural change? The answer will shape returns and risks going forward.

Market Highlights

Here are the fast facts that moved markets and investor attention today.

- Oil prices rose after a warning from former President Trump toward Iran, and a tanker fire in the Gulf of Oman added supply concern, supporting crude benchmarks.

- Global oil and gas spending is set to fall, with BMI forecasting total sector capex of $636 billion for 2026, below 2025 levels.

- Automotive and EV headlines were upbeat, with the Kia EV2 delivering 105% of its official range in a real-world test, and Ford's low-cost EV pickup sighted in Long Beach, trading chatter around $F ahead of further testing news.

- Renewables and critical minerals headlines were mixed, from U.S. scrutiny of solar manufacturing capex to an auction of 10.2 MW of Longi panels from a failed Swedish PV project.

Key Developments

Oil prices supported by geopolitics and maritime incidents

Markets responded to rising geopolitical tension after a public warning to Iran and a reported fire on a tanker that previously carried Iranian oil in the Gulf of Oman. That combination tightened the narrative around short-term supply risk and helped push oil prices higher today.

For you that means near-term volatility may remain elevated in oil markets as political signals and maritime security reports get priced into futures and equity moves.

Investment trends point lower despite higher prices

The International Energy Agency's 2026 outlook and a separate BMI forecast both surprised markets by predicting declines in oil and gas investment this year. BMI put global spending at about $636 billion, down from 2025, indicating a disconnect between price levels and capital allocation.

Analysts note the gap suggests companies may be prioritizing balance sheets and shareholder returns over new capacity. That strategy could tighten supply later if demand holds, so you should weigh short-term price gains against longer-term capacity dynamics.

LNG, supply chains and critical minerals get complicated

Germany's big LNG deal with Canada is under scrutiny and may never deliver a cargo, highlighting how geopolitics and logistics are complicating Europe’s efforts to secure long-term gas supplies. That underlines continued market fragmentation for natural gas supplies.

At the same time Central Asia is moving onto the map for critical minerals, with U.S. and regional talks set in Astana on June 11 and 12 to push mining and processing projects. You should watch how these diplomacy-led deals evolve because they affect the clean energy supply chain over years, not months.

What to Watch

Here are the catalysts and risks to monitor heading into tomorrow and the coming weeks.

- Geopolitical headlines and maritime security alerts, which can move oil prices quickly. Expect traders to react to statements from regional actors and any updates on tanker incidents.

- Capital expenditure and guidance from large oil and gas producers. If majors revise capex further downward, it could support higher prices later by constraining supply growth.

- LNG contract implementation and delivery schedules, particularly the Germany-Canada framework. Missed deliveries or contract disputes would keep European gas markets tense.

- Solar manufacturing metrics and auction outcomes for failed PV projects, including the Swedish sale of 10.2 MW of Longi modules. These signal execution risk in the renewables buildout and could affect equipment suppliers and developers.

- EV and energy storage product rollouts, including real-world range data like Kia’s EV2 and sightings of low-cost pickups from Ford $F. Consumer acceptance and product performance will influence demand for grid charging and battery supply chains.

Bottom Line

- Short-term energy prices are being propped up by geopolitical risk and operational incidents, creating volatility you may see reflected in energy equities and commodity futures.

- Major forecasts from the IEA and BMI point to falling oil and gas capex, a trend that could tighten supply down the road even as prices bump higher now.

- Renewables show mixed signals, with manufacturing scrutiny and project failures on one hand, and progress in EV range and storage deals on the other.

- Critical minerals diplomacy in Central Asia could yield supply solutions for the energy transition, but these are longer horizon developments you should monitor.

- Stay selective and watch catalysts. Data suggests momentum is uneven across subsectors, so your focus should be on news flow and company-level execution.

FAQ

Q: How will lower oil and gas capex affect prices? A: Reduced capex generally implies slower supply growth, which can support higher prices over time if demand holds. Pricing will still respond to near-term events and economic signals.

Q: Should you worry about the Germany-Canada LNG deal collapsing? A: The deal highlights delivery risk in long-term LNG contracting. Market impact depends on alternative supplies and seasonal demand, so monitor contract and shipping updates.

Q: What do solar module auctions and manufacturing scrutiny mean for renewables investors? A: They signal execution and margin pressure in some parts of the solar supply chain. Analysts note capex intensity and production metrics will matter more than headline capacity numbers.