The Big Picture

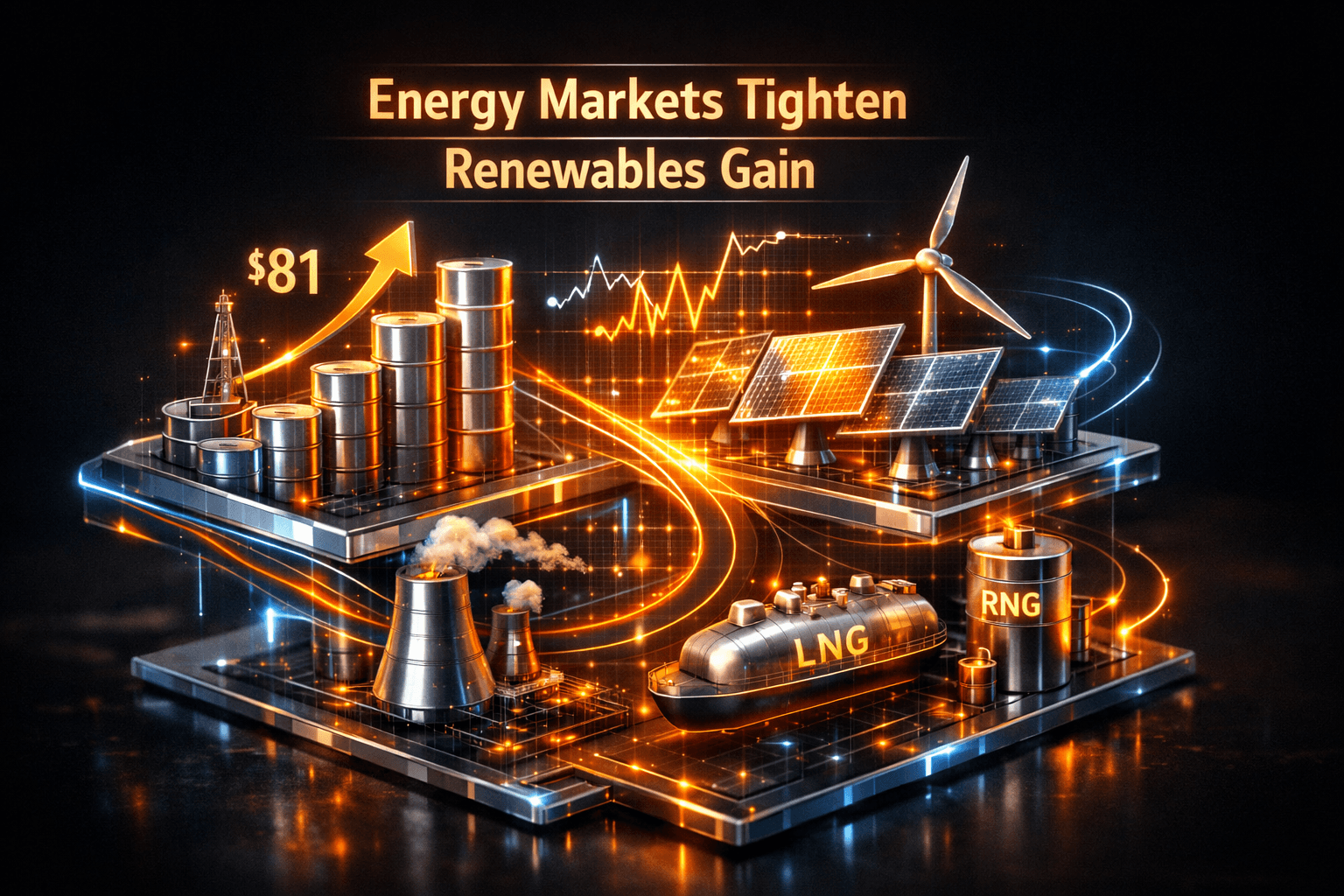

Oil market tightness and a persistent war risk premium have traders pricing crude well above $81 a barrel for the next 12 months, while renewables are making structural gains that are reshaping power markets. This combination matters because you could see higher near-term oil-driven volatility alongside accelerating clean-energy adoption that pressures gas demand.

Data and capital flows are lining up on both fronts. Analysts note extremely large inventory draws and survey expectations for sustained oil pricing, even as wind and solar collectively produced a record share of global power last month. How you weigh those trends will shape positioning across energy stocks and project-level investments.

Market Highlights

- Oil price expectations: Bloomberg Intelligence survey finds traders expect oil to average between $81 and $100 per barrel over the next 12 months.

- Inventory draws: Goldman Sachs reports global oil draws running at about 8.7 million barrels per day since early May, the highest rate on record.

- Renewables milestone: Wind and solar generated 22% of global electricity in April, surpassing gas at 20% for the first time on a monthly basis.

- European savings: Solar photovoltaics helped Europe avoid roughly €10 billion in gas imports since early March, an average of about €110 million per day.

- Policy target: IRENA proposed a global electrification target of 35% by 2035, underscoring grid investment needs with up to 2.5 TW of projects in connection queues.

- Corporate moves: Constellation is partnering to develop about 3.0 million MMBtu annually of additional RNG, and the Arab Energy Fund committed $120 million toward MidOcean LNG investments.

Key Developments

Oil tightness and inventory alarms

Goldman Sachs flagged accelerating global oil inventory draws, and a Bloomberg Intelligence survey shows market participants expect prices to remain well above $81 a barrel for the next year. Physical bottlenecks, low exports through key straits, and logistical re-routing are keeping a war risk premium priced into markets. For you, that means energy price volatility is more likely in the near term as markets respond to supply disruptions and inventory data.

Renewables hit critical mass

Wind and solar together produced 22% of global electricity in April, overtaking gas-fired generation for the first time on a monthly basis. SolarPower Europe estimates photovoltaic output cut European gas import bills by about €10 billion since the escalation of the Iran conflict. This is a clear signal that renewables are not just growing, they are changing trade flows and the economics of gas-fired power. If you follow utilities or power producers, watch how fuel mixes and merchant power margins evolve.

Policy, grid strain and project finance

IRENA’s proposal for a 35% global electrification target by 2035 highlights the need for grid upgrades, since as much as 2.5 TW of solar, storage and wind projects are queued for connection. At the same time, capital is moving into LNG and RNG: an Arab Energy Fund commitment of $120 million into MidOcean and Constellation’s framework to add about 3.0 million MMBtu per year of RNG production show private capital chasing both transition fuels and cleaner gas alternatives. These moves signal investment opportunities across midstream, RNG developers, and grid builders, though grid bottlenecks could slow project ramp-ups.

What to Watch

Watch weekly and monthly oil inventory data to gauge whether current draws persist, since $81-plus pricing expectations hinge on supply tightness. You should also track shipping and export flows through critical chokepoints, because logistics remain a key driver of the war risk premium.

On the power side, monitor announcements around grid interconnection approvals and transmission spending. If connection queues remain long, project developers could face delays even as demand for renewable capacity grows. Are policymakers going to accelerate permitting and grid builds to match the pipeline of projects?

Keep an eye on corporate partnerships and financing rounds in RNG and LNG, since fresh capital commitments, like the $120 million MidOcean investment and Constellation’s RNG deal, can speed project delivery. Finally, follow technology risk factors, including UNSW’s new findings about UV-induced degradation in PERC and TOPCon cells, because they affect module longevity and warranty assumptions for solar portfolios.

Bottom Line

- Global oil markets are tightening, and market surveys plus large inventory draws point to elevated crude prices for the next 12 months, which raises near-term volatility.

- Renewables are reaching scale, with wind and solar surpassing gas generation in April and materially reducing European gas import bills.

- Policy targets and grid constraints will be decisive for how fast queued renewable projects reach commercial operation, so grid investment news matters more than ever.

- Investment flows into LNG and RNG show capital is betting on transition fuels alongside renewables, creating diverse exposure opportunities across the energy value chain.

- Technology risks, such as UV-induced degradation in some solar cell types, are real and deserve attention when evaluating module suppliers and long-term project economics.

FAQ

Q: How will higher oil prices affect renewable power economics? A: Higher oil indirectly raises fossil fuel price narratives and can accelerate renewables adoption by widening the cost gap for imported fuels, but electricity markets are more directly tied to gas and coal prices.

Q: Does the IRENA 35% electrification target change project timelines? A: The target raises urgency for grid upgrades and could speed permitting and financing, but actual project delivery will depend on regulatory action and transmission buildout.

Q: Should I be worried about the UNSW solar cell findings? A: The research highlights a degradation mechanism that suppliers and developers need to address through materials and module design, so you should factor potential performance risk into solar project due diligence.