The Big Picture

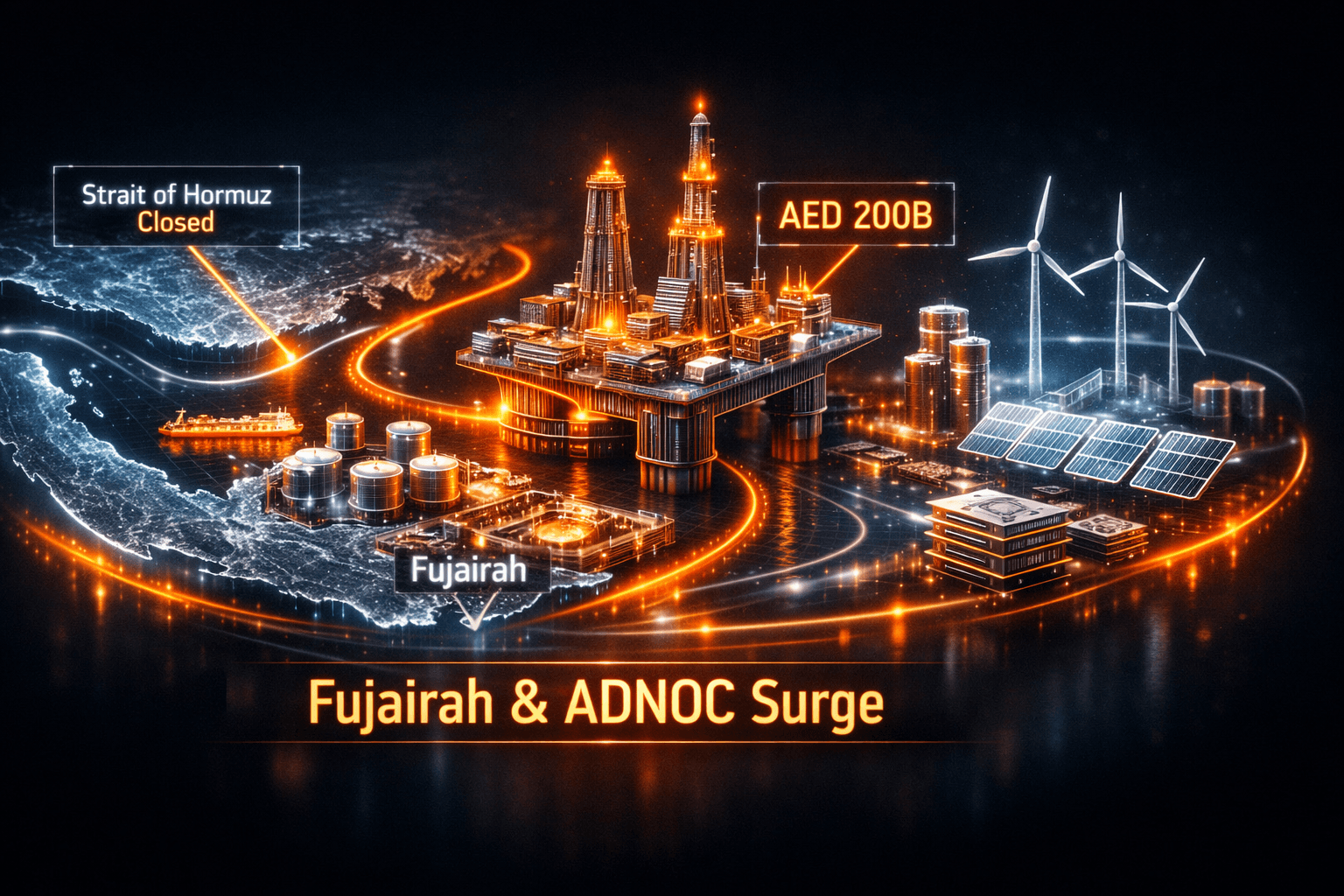

The nine-week closure of the Strait of Hormuz continues to reshape global oil logistics, funneling crude and bunkering activity to Fujairah and keeping shipping risk premiums elevated. At the same time, Abu Dhabi's ADNOC announced AED 200 billion, roughly $55 billion, in new project awards for 2026 to 2028, signaling strong Gulf capex despite the geopolitical strain.

These twin themes matter to you because they combine near-term market disruption with long-term investment and development activity. You should expect more rerouted cargoes, continued caution from shipowners, and sustained project spending across oil and gas and select energy infrastructure projects.

Market Highlights

Quick facts and moves to note from today's headlines.

- Strait of Hormuz closure has entered its ninth week, pushing exports and bunkering toward Fujairah and making the port a heightened target in the region.

- ADNOC announced AED 200 billion in project awards for 2026-2028, about $55 billion in new contracts and spending.

- Scatec's Obelisk project drew a 20 percent equity stake from Egypt's National Bank for a 1.1 GW solar plus BESS development, reducing Scatec's economic interest to 40 percent, ticker $SCATC.

- Shell and INEOS plan more joint tiebacks in the US Gulf, with INEOS taking roughly 21 percent working interests in select assets, while Shell operates the hub, ticker $SHEL.

- European offshore wind is confronting concentrated turbine supply after GE paused new offshore orders, leaving Siemens Gamesa and Vestas, tickers $SGRE and $VWS, as dominant suppliers.

- EV and charging tech stayed in focus: Kempower unveiled a Mega Satellite Flex charger offering CCS up to 560 kW and megawatt charging up to 1.2 MW, and Hyundai's IONIQ 5 remains an affordable EV option starting near $35,000.

- On consumer tech, EcoFlow ran a Mother's Day promotion with discounts up to 64 percent, including a flash sale price of $829 on a 2,048Wh unit.

Key Developments

Hormuz Crisis and Fujairah's Growing Role

With the Strait of Hormuz still effectively closed, Fujairah has become the central export and bunkering hub outside the strait. That shift is sustaining demand for storage, lightering and onshore logistics at Fujairah, but it's also raising security risk and insurance costs for vessels using nearby waters.

Shipowners remain cautious despite diplomatic chatter about peace prospects, and today's reporting shows they're not rushing back through Hormuz. What does that mean for oil and freight costs, and for regional refiners and traders who rely on reliable transit routes?

Gulf Spending Accelerates, Shell and INEOS Expand Tiebacks

ADNOC's AED 200 billion program is a clear statement of growth intent. Those awards are aimed at accelerating delivery of capacity and infrastructure between 2026 and 2028, and they'll support engineering, procurement and construction activity across the region.

Meanwhile, $SHEL and INEOS activity in the US Gulf through joint tiebacks and working interest swaps underscores continued basin-level investment. For contractors and service firms, near-term work will likely stay firm. For you, that means watching tender pipelines and contractor margins.

Renewables and Electrification: Mixed Signals

Renewables posted selective wins today, like the National Bank of Egypt taking a 20 percent stake in Scatec's 1.1 GW Obelisk solar and BESS project, supporting project financing and regional deployment. At the same time, Rystad and others flag growing supply constraints in European offshore wind after GE paused new offshore orders, concentrating available turbines with $SGRE and $VWS and pushing up per-megawatt costs.

EV and charging technology continued to progress, illustrated by Kempower's high-power charger and Hyundai's value EV. Biomethane markets also tightened their rules as ISCC updated mass balance guidance, elevating traceability and audit expectations for traders and offtakers. Can developers and traders adapt fast enough to avoid project delays or cost creep?

What to Watch

You'll want to track a handful of near-term catalysts and risks that could move markets tomorrow and in coming weeks.

- Shipping lanes and insurance: Monitor announcements about Strait of Hormuz reopening or changes in war risk premiums, as those drive freight and crude route economics.

- ADNOC delivery schedule: Watch how the AED 200 billion awards are parceled across 2026 to 2028 and which contractors win work, because that affects supply chains and regional cash flow.

- Offshore wind supply signals: Look for updates from GE or alternative turbine makers, and keep an eye on auction timelines that may be delayed by equipment scarcity.

- Project financing and offtake: Follow Scatec milestones and financing terms, and check for similar bank or institutional stakes in utility-scale renewables that can de-risk pipeline projects.

- Technology rollouts: Track megawatt-class chargers and heavy-duty charging deployments, because charging scale will influence heavy EV economics and freight electrification plans.

Bottom Line

- Geopolitics and logistics dominate near-term risk, with Fujairah a focal point as oil and bunkering flows reroute away from Hormuz.

- Large Gulf capex, led by ADNOC's AED 200 billion in awards, signals continued upstream and midstream investment through 2028, supporting service-sector activity.

- Renewables momentum is intact, but supply-chain constraints in European offshore wind and tighter biomethane rules add execution risk for developers and traders.

- EV and charging tech progress is tangible, with heavy-duty charging entering megawatt territory, yet commercial rollout and grid readiness will be key variables.

- You should watch shipping insurance, turbine supply updates, and ADNOC contract rollouts to gauge market direction and project delivery timelines.

FAQ

Q: How is the Strait of Hormuz closure affecting oil flows and prices? A: The closure has rerouted exports toward Fujairah, increasing bunker and storage demand and keeping shipping risk premiums elevated, which can support regional freight costs and price volatility.

Q: Does ADNOC's AED 200 billion in awards mean more supply for global markets? A: The awards fund capacity and infrastructure through 2028, but project timelines, sanctions or logistics disruptions will determine when new output or services reach markets.

Q: Should I be worried about offshore wind project delays? A: Supply concentration and paused orders have raised the risk of cost increases and schedule slips for European projects, so watch turbine availability and developer guidance.