The Big Picture

Today’s Energy headlines show a clear split between durable momentum in renewables and renewed geopolitical pressure on oil markets. You’ll see fresh capacity, R&D calls, and cross-border funding on the clean-energy side, while Middle East tensions and warnings about high oil prices keep the market on edge.

That mix matters because it affects where policy, capital, and price risk are flowing this week. Do you favor decarbonization winners or defensive oil exposures? The answer will depend on how these cross-currents evolve over weeks, not days.

Market Highlights

Quick facts and figures to keep you up to speed this morning.

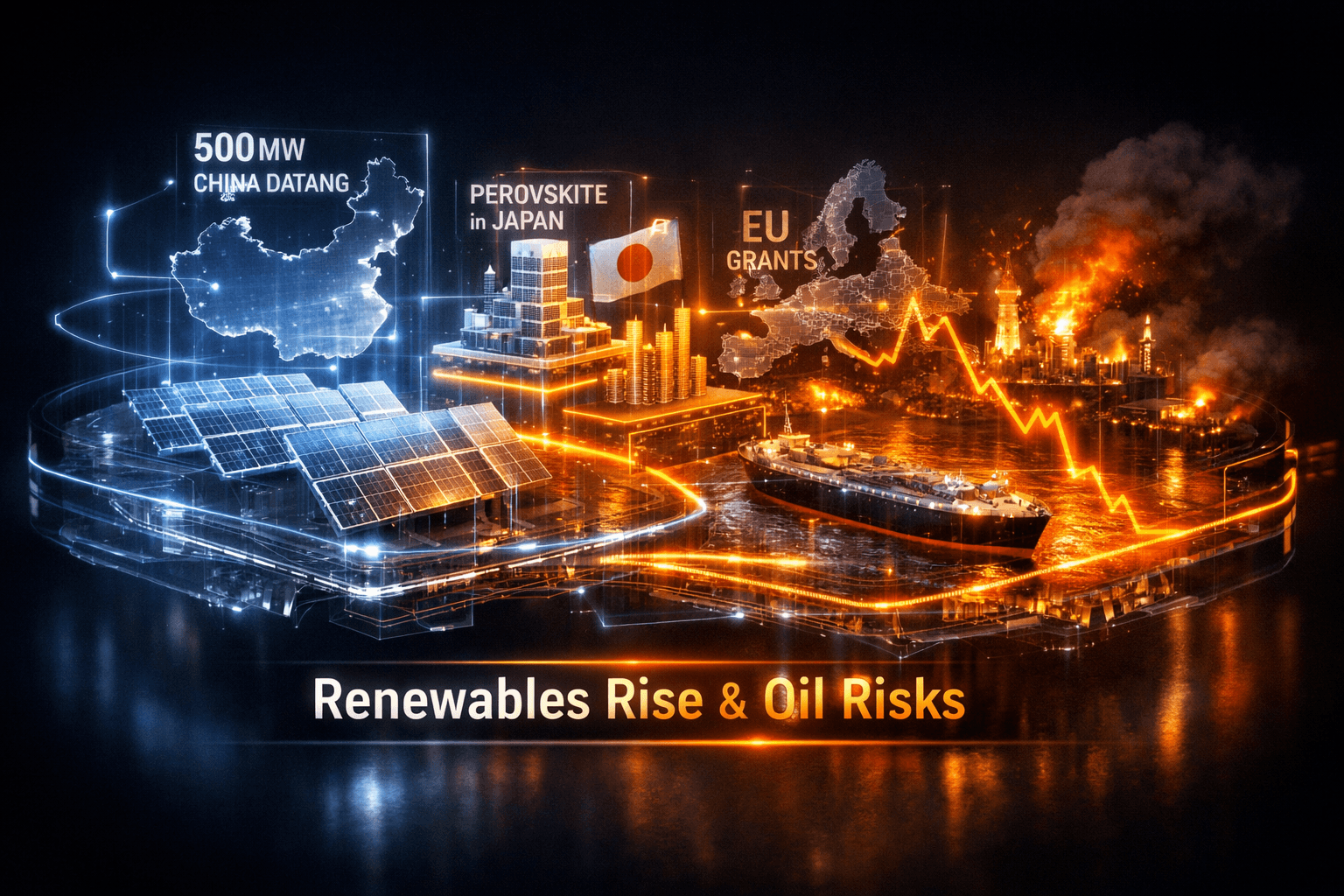

- China Datang brought a 500 MW solar farm online, part of a larger 2 GW first-phase build using solar, wind, storage, dedicated transmission and market trading to serve data centers.

- Japan’s NEDO reopened a supplementary call focused on single-junction perovskite solar cells, with submissions due by June 3, signaling continued government R&D support.

- The European Commission launched a new funding call totaling $704 million for cross-border energy projects under the Projects of Common Interest and Projects of Mutual Interest list.

- The IEA’s Global Methane Tracker 2026 notes methane emissions plateaued near record highs in 2025, but says widespread abatement could unlock long-term natural gas volumes comparable to major supply shocks.

- Geopolitical headlines pushed oil prices higher after Iran warned it could strike U.S. forces near the Strait of Hormuz and the U.S. said it would guide trapped ships through the strait.

- Moody’s Analytics warned that sustained Brent prices at $125 per barrel could tip the global economy into a shallow recession, highlighting macro downside risk from prolonged price spikes.

- On the mobility front, $TSLA’s Full Self-Driving fleet reached 10 billion supervised miles, with the fleet logging roughly 29 million miles per day as of late April.

Key Developments

China Datang’s 500 MW Solar, a Data-Center Play

China Datang’s new 500 MW solar plant is notable because it’s tied directly to data center supply and is nested within a 2 GW first-phase program that combines wind, storage and dedicated transmission lines. For you that means utilities and grid planners are increasingly building renewables with large off-takers in mind, reducing offtake risk and improving project bankability.

The integration with market trading mechanisms also shows how developers are combining physical contracts with market solutions to firm supply. That’s important if you own stocks or funds exposed to corporate offtake or grid-scale storage developers.

Policy and R&D: Japan’s Perovskite Push and EU Funding

Japan’s NEDO reopening a perovskite call focused on single-junction mass production keeps next-generation PV development on track. The June 3 deadline suggests short timelines for pilots and scale-up plans that may influence module makers and materials suppliers.

At the same time the EU’s $704 million funding call for cross-border projects signals sustained public capital for transmission, interconnectors and cross-border renewables. Public funds like these often de-risk projects and draw private co-investment, so policy momentum remains strong in Europe.

Methane Abatement and Gas Market Implications

The IEA says methane measures could unlock gas volumes equivalent to double the supply currently disrupted by an effective Strait of Hormuz closure. That’s a long-term structural observation, not a short-term fix, but it highlights how emissions policies and infrastructure can affect gas balances and pricing over time.

If methane abatement scales, you could see changes in gas market dynamics that matter for utilities, midstream companies, and regional gas-exposed equities.

What to Watch

Here are the catalysts and risks that could move energy names and sectors this week.

- Geopolitical updates out of the Gulf, and any U.S. naval or convoy activity near the Strait of Hormuz. These items will likely continue to move oil volatility and sentiment.

- Brent and WTI price action, and commentary around the $125 per barrel threshold Moody’s flagged. That level is a macro risk marker that you should monitor for broader economic impact.

- Follow submissions and award announcements from Japan’s NEDO and the EU funding call. Those decisions can shape supply chains and grant recipients over the next 6 to 18 months.

- Methane policy moves and implementation of abatement technologies. Will regulators or buyers accelerate mandates that shift gas flows? That could affect midstream and producer cash flows long term.

- Technical and calibration work from the solar metrology study. Differences in testing methods could influence module certification timelines and yield expectations for manufacturers.

Which sectors do you think will attract the most capital this year, renewables or traditional oil and gas? Watch funding and regulatory signals for the clearest answer.

Bottom Line

- Renewables showed concrete progress today, with China Datang’s 500 MW solar online and public R&D and funding moves in Japan and the EU reinforcing policy support.

- Geopolitical tensions around the Strait of Hormuz are boosting near-term oil volatility and keeping macro risk in focus, especially around the $125 Brent threshold.

- Methane abatement emerges as a potential structural gas supply story, with the IEA noting significant long-term upside if measures scale.

- Technical work on solar calibration highlights that accuracy and standards remain important as PV mass production ramps up.

- Overall the picture is mixed, so a selective approach and close monitoring of policy, funding awards and Gulf developments is warranted for your portfolio decisions.

FAQ

Q: How material is China Datang’s new 500 MW solar plant for global renewable capacity? A: It’s a significant project at the regional level and part of a 2 GW first-phase plan, showing industrial-scale integration of solar, wind and storage for large corporate offtakers.

Q: Could oil at $125 per barrel trigger a recession? A: Moody’s Analytics warns sustained Brent at $125 could tip the global economy into a shallow recession, so sustained high prices are a clear macro downside risk.

Q: What does the IEA say about methane and gas markets? A: The IEA’s Global Methane Tracker 2026 reports methane emissions plateaued near record highs in 2025, but notes that broad methane abatement could unlock long-term gas volumes comparable to major supply disruptions.