The Big Picture

Today’s top Energy stories paint a mixed picture for investors, with a major domestic lithium discovery and accelerating electric vehicle developments on one side, and persistent geopolitical strain on oil supplies on the other. You’ll want to weigh both the structural upside for batteries and EVs and the short term stress on oil logistics when you think about energy exposure.

The net effect is neither outright boom nor collapse, it’s a market in transition. How you position for that transition will depend on your time horizon and risk tolerance, so consider the catalysts and hazards below.

Market Highlights

Markets were closed on Sunday, May 3. The last trading day was Friday, May 1, so these items describe developments heading into the long weekend and operational metrics from the stories.

- $TSLA, Tesla: Full Self-Driving fleet clocked 10 billion supervised miles, and fleet data collection accelerated from about 14 million miles per day earlier in 2026 to roughly 29 million miles per day by late April, a rise of about 107% in daily miles logged.

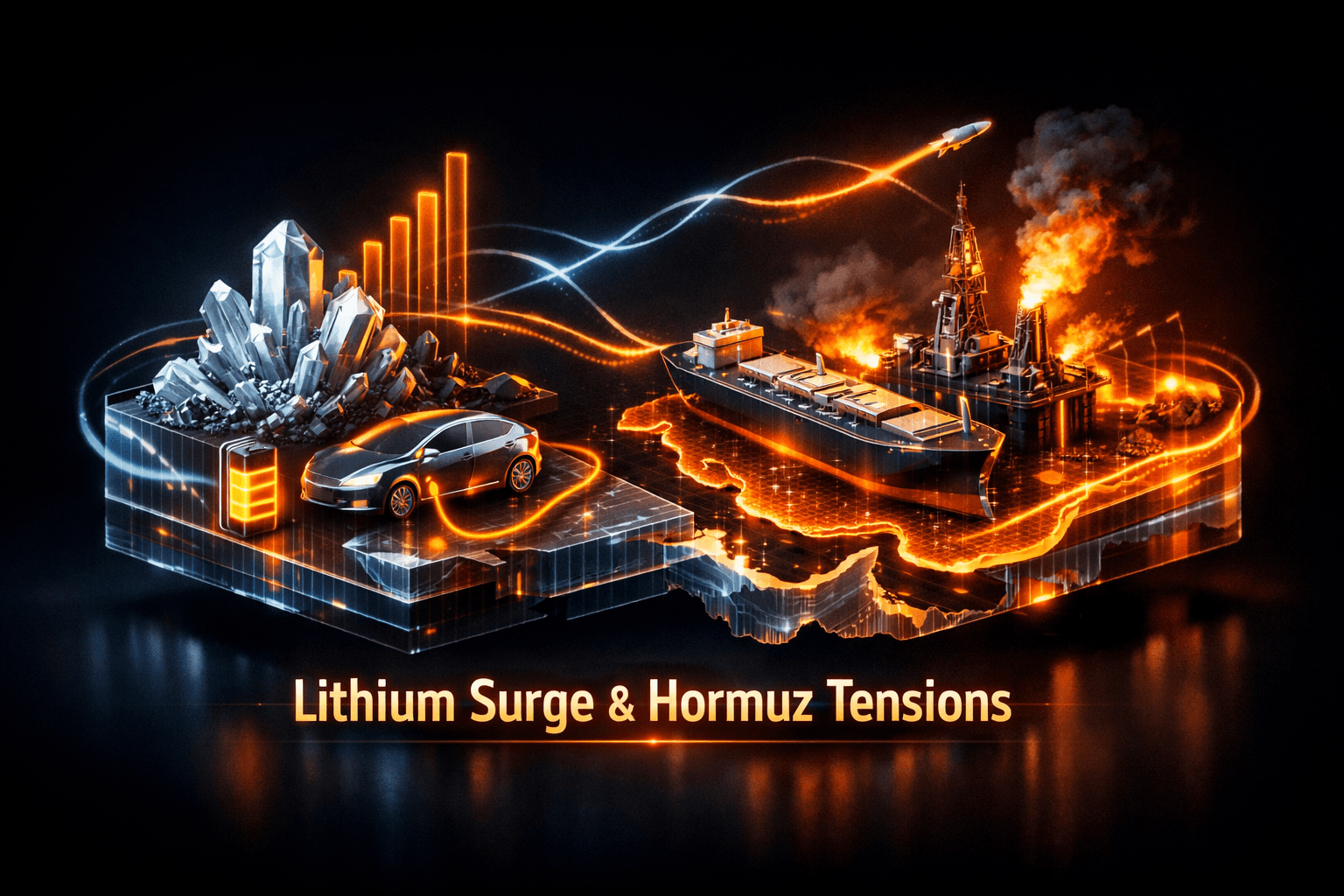

- $CVX, Chevron: CEO commentary flagged the global energy system as under "extreme stress" as the U.S.-Israel war with Iran stretches into its third month, a signal that oil supply risk premiums remain elevated heading into the week.

- $SEPLAT, Seplat Energy: The company raised its Q1 dividend citing a robust oil price outlook, reflecting near-term strength for some upstream players amid tightened tanker flows through the Strait of Hormuz.

- USGS lithium finding: The agency estimates roughly 2.3 million metric tons of recoverable lithium in Appalachia, equivalent to about 328 years of last year’s U.S. lithium imports, a material domestic supply implication for battery supply chains.

Key Developments

USGS Finds Massive Appalachian Lithium Resource

The USGS reported an estimate of about 2.3 million metric tons of potentially recoverable lithium in the Appalachians, which analysts translate to roughly 328 years of last year’s U.S. lithium import demand. This changes the supply narrative for U.S. battery manufacturing and could reduce strategic reliance on overseas sources over the long term.

For you, that means domestic miners, processors, and refining projects will merit closer attention as potential long-term beneficiaries, while permitting and development timelines will determine how fast this resource impacts markets.

Hormuz Deadlock and Industry Stress

The Strait of Hormuz remains constrained about two months into the Iran war, and U.S. naval actions have added friction to tanker movements. Chevron’s CEO warned the global energy system is under "extreme stress," highlighting inventory drawdowns and logistical bottlenecks.

That stress supports higher near-term oil price risk premia, which helps upstream cash flows and dividend policies for some producers, but it also increases volatility and geopolitical risk for you to monitor.

EV Momentum and Battery Supply Side Moves

Tesla’s FSD fleet reaching 10 billion supervised miles is a headline milestone, and the acceleration in miles collected suggests faster iterative training for autonomy software. Don’t expect Level 4 autonomy immediately, but data scale matters for software development and regulatory arguments.

At the same time consumer and powersports electrification expands, with Electrek highlighting top e-bikes for May and Segway launching the 60 MPH Xaber 300 electric dirt bike, signaling demand and product diversification within the broader EV ecosystem.

What to Watch

Upcoming catalysts and risks will shape energy sector direction as markets reopen on Monday, May 4. Here’s what you should track.

- Geopolitical updates out of the Middle East, especially any shifts in tanker traffic through the Strait of Hormuz, which will quickly affect oil risk premia and volatility.

- Permitting and project announcements related to the Appalachian lithium find. Watch federal and state regulatory timelines, potential private sector JV announcements, and near-term exploration results.

- Regulatory and legal outcomes affecting renewables. Recent court pushback against federal attempts to slow renewables signals that policy uncertainty is not settled, so follow related rulings and federal guidance.

- Corporate actions from producers, including dividend and capital allocation updates like Seplat’s Q1 dividend increase. These will indicate how companies are translating higher prices into shareholder returns or reinvestment.

- EV software and autonomy updates from $TSLA, including regulatory submissions and safety data releases, which could influence investor confidence in the autonomy roadmap.

Bottom Line

- USGS’s Appalachian lithium estimate is a potential long-term positive for domestic battery supply chains, but development will take years and regulatory approvals.

- Geopolitical disruptions at the Strait of Hormuz and industry warnings about supply stress are supporting oil price risk premia and corporate actions such as dividend increases.

- EV product launches and Tesla’s data milestone underline growing momentum for electrification, while regulators and safety milestones will determine the pace of autonomy adoption.

- Market signals are mixed, so your approach should be selective and focused on time horizon, exposure to commodities versus electrification, and tolerance for geopolitical volatility.

FAQ Section

Q: What does the USGS lithium find mean for battery prices? A: The USGS estimate points to a long term increase in potential domestic supply which could ease upward pressure on battery raw material prices over time, but immediate impacts depend on project permitting and buildout timelines.

Q: Should I expect oil prices to keep rising because of the Hormuz situation? A: Supply disruption risk supports elevated price risk premia, but prices will respond to news flow, inventories, and diplomatic developments, so volatility remains likely.

Q: Does Tesla’s 10 billion FSD miles mean self driving is here now? A: The milestone reflects scale in supervised driving data collection, which is important for development, but it does not signal an immediate switch to unsupervised Level 4 deployment.