The Big Picture

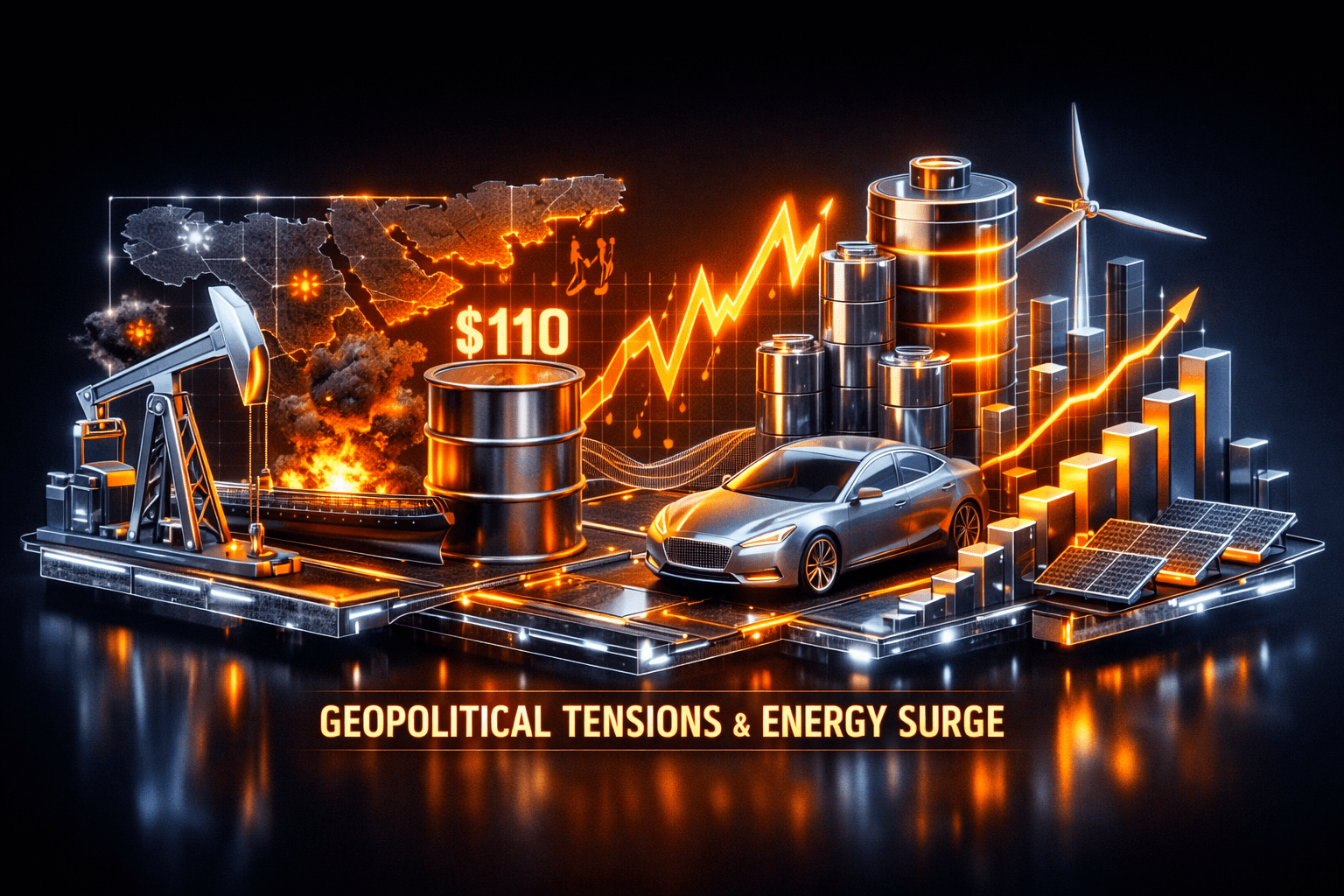

Geopolitical shocks and accelerating clean-energy investment are colliding, and the net effect is lifting the broader energy complex. Brent crude was trading near $114 a barrel as of Thursday, Apr 2, with the Strait of Hormuz effectively closed to commercial traffic and the IEA calling the disruption the largest in the history of the global oil market.

At the same time, the United States and global manufacturers are scaling batteries, electrified heavy equipment, and port electrification projects, which is reshaping demand patterns and supply chains. If you follow energy markets, this is a period where volatility meets structural change, and that combination matters for risk and opportunity alike.

Market Highlights

Here are the quick facts you need heading into the week.

- Oil: Brent near $114 a barrel as of Thursday, Apr 2, amid the US-Israel campaign against Iran and a de facto closure of the Strait of Hormuz.

- Producers: Continental Resources, $CLR, said it will boost output as prices soar, signalling producers are responding to the tight supply environment.

- Batteries and storage: U.S. battery manufacturing capacity is expanding rapidly, with industry forecasts saying supply may soon outstrip near-term demand; demand for energy storage is expected to rise roughly 21 percent this year.

- Ports and logistics: APM Terminals' electrification at the Port of Los Angeles cut terminal truck idle times by almost 85 percent, improving throughput and lowering fuel costs.

- Heavy equipment: Komatsu's new electric PC9000-12 excavator, listed in U.S. OTC as $KMTUY, can move about 80 tons per pass and more than 8,000 tons per hour.

Key Developments

Middle East conflict tightens oil supply

The ongoing US-Israel air campaign against Iran has had a tangible market impact, pushing Brent higher and prompting the IEA to label the event the largest supply disruption ever recorded. With the Strait of Hormuz effectively closed to commercial traffic, global crude flows are constrained and volatility is elevated. For you, that means energy price risk will likely drive headlines and prompt rapid re-pricing across oil-related names.

U.S. producers and fiscal responses

Continental Resources, $CLR, is publicly boosting output as prices climb, showing that producers are moving to capture short-term margins. Meanwhile, Russian oil tax receipts plunged roughly 48 percent year on year in March, highlighting how geopolitical shifts are reshaping national revenues and investment incentives.

Electrification and battery build-out accelerate

U.S. battery manufacturing is scaling fast, and Sungrow reported that storage overtook inverters as its top segment in 2025 with revenue up about 15 percent at the company. Ports, heavy equipment and utility-scale solar are also electrifying. The Port of Los Angeles experiment cut terminal truck dwell times by nearly 85 percent, and a new Ohio solar farm came online using state-made panels. These moves are lowering operating costs and tightening local supply chains, but analysts warn the industry may face near-term oversupply.

What to Watch

Expect the near-term narrative to be driven by geopolitics, policy moves, and capacity additions. How will you follow these risks and catalysts?

- Geopolitical updates: Watch for new IEA statements, shipping lane reports, and official comments from Tehran and regional actors. Any reopening of the Strait of Hormuz would matter instantly to prices.

- Producer actions: Track announcements from $CLR and other E&P names on output plans, plus any OPEC+ meetings or supply coordination that could affect crude balances.

- Battery and storage capacity data: New factory start-ups and utilization rates will determine whether supply outstrips demand and how pricing evolves for cells and storage systems.

- U.S. policy shifts: The auto industry proposal to replace the gas tax with a vehicle fee could reshape transport fuel demand dynamics over years, especially as EV penetration rises from its current roughly 2.5 percent share of light-duty vehicles.

- Local price moves: Turkey is weighing electricity and gas price increases, which could add regional inflationary pressure and affect natural gas flows and contracts.

Bottom Line

- Brent at about $114 as of Thursday, Apr 2, reflects a major supply shock centered on the Strait of Hormuz; watch IEA and shipping updates closely.

- U.S. producers like $CLR are increasing output to capture current margins, which could add near-term supply but may not offset the geopolitical squeeze.

- Electrification projects from ports to heavy equipment are lowering operating costs and creating new demand for batteries, even as rapid battery build-out raises short-term oversupply risk.

- Policy changes such as a proposed vehicle fee to replace the gas tax could reshape long-term road funding and fuel demand, an important structural trend for energy use.

- For you, selectivity matters: follow company-level capacity and utilization metrics, stay alert to news flow on shipping lanes, and watch policy shifts that affect demand.

FAQ Section

Q: How high could oil prices go from here? A: Price direction will hinge on geopolitics, shipping access and producer responses; with the Strait of Hormuz disrupted, upside risk is elevated but timing is uncertain.

Q: Will US battery oversupply hurt clean-energy companies? A: Oversupply risk may pressure margins and pricing for cell makers, but project-level demand for storage and electrification can still support growth for manufacturers that manage costs and contracts.

Q: What immediate data should I watch this week? A: Monitor IEA releases, shipping and maritime notices, producer production updates, and any factory start-up or utilization figures from battery makers and major equipment suppliers.