The Big Picture

Global energy markets opened today under starkly mixed signals, with a supply shock tied to the Strait of Hormuz pushing crude sharply higher while renewable power and storage activity accelerated across multiple regions.

That split matters because it’s changing near-term price dynamics and long-term investment priorities at the same time. You’ll want to track both the geopolitical headlines that are keeping oil volatile and the policy and procurement moves that are speeding up solar and battery deployments.

Market Highlights

Key numbers and moves to know as trading begins:

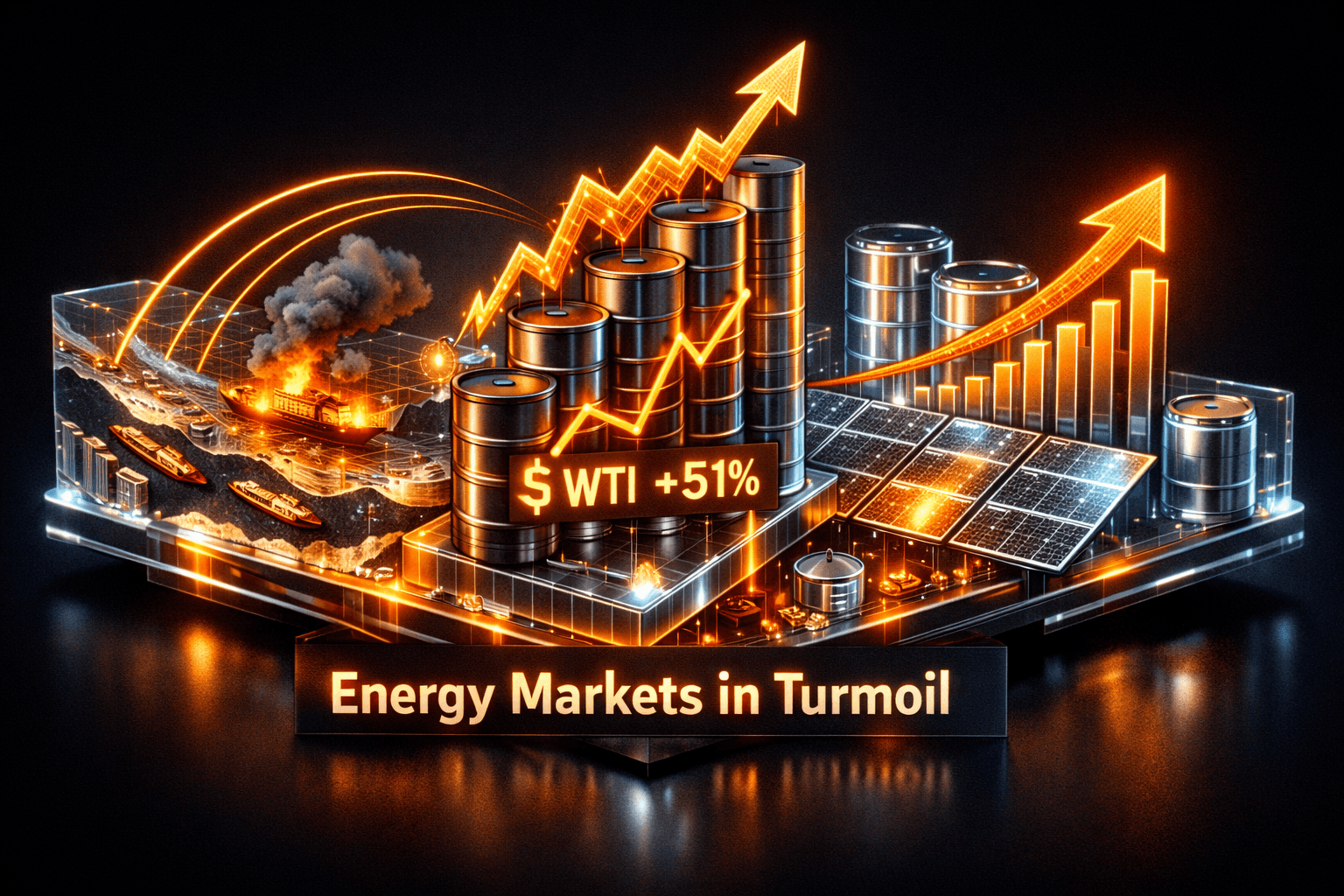

- Crude surge: West Texas Intermediate gained about 51% over the past month, trading above $100 per barrel, according to reporting on the price jump.

- Fuel costs: Gasoline averages topped $4 per gallon and diesel sits near $5.50 per gallon, raising consumer and transportation cost pressures.

- Renewables scale: IRENA data shows 692 gigawatts of renewables were added in 2025, bringing global capacity to roughly 5,149 GW.

- Storage deal flow: Swiss consultancy Pexapark logged more than 1 GWh of European storage PPAs in March, signaling stronger commercial interest in batteries paired with solar.

- Grid projects: Australia’s Transgrid shortlisted nine battery projects totaling about 2 GW for New South Wales grid services later this year.

- Policy actions: The UAE has urged the UN to consider measures including force to reopen the Strait of Hormuz, and ADNOC’s CEO called for global action as transit has been near standstill for over a month.

Key Developments

Hormuz blockade raises short-term supply risk

Traffic at the Strait of Hormuz has been severely restricted for more than a month, and regional governments are pressing for international steps to restore passage. The UAE asked the UN to authorize measures, including force, and the Group CEO of ADNOC described Iran’s actions as economic extortion.

That disruption is a direct driver of the oil spike and it’s keeping market risk premiums elevated. If you follow energy markets, you should expect headline sensitivity to escalate until shipping lanes normalize.

WTI surge and immediate market effects

West Texas Intermediate’s roughly 51% month-on-month jump has already translated into higher pump prices for consumers and heavier cost burdens for freight and industrial users. The rise is the biggest monthly move since WTI futures began trading in 1983, underscoring how acute the current supply shock is.

Major oil producers and integrated energy companies such as $XOM and $CVX are getting attention as traders price in sustained supply uncertainty and the potential for stronger upstream cash flows, although corporate-level impacts will vary by asset mix and hedging.

Renewables and storage momentum, and supply-chain pressure

At the same time, the clean-energy transition is not slowing. IRENA’s 2025 numbers show a record build of 692 GW of renewables, while Pexapark reports more than 1 GWh of European storage PPAs in March. Australia’s Transgrid shortlisting of 2 GW of batteries for the NSW grid is another sign of accelerating deployment.

But supply chains remain a wildcard. Reporting on defense supply chains shows China’s late-2025 restrictions on processed rare earth metals are pushing the U.S. and partners to rebuild domestic processing and sourcing. Those same materials are vital to wind turbines, electric motors, and some battery components, so constraints in critical minerals could slow project build-outs or raise costs even as demand rises. What should you infer from that? It means renewable growth is strong, but component availability and geopolitical friction are shaping project timelines and margins.

What to Watch

Here are the catalysts and risks that could move energy names and the broader sector today and in the coming weeks.

- Geopolitical headlines, shipping updates: Daily reporting on Strait of Hormuz transits, UN or coalition actions, and Iran-related developments will remain the primary driver of oil volatility.

- Oil inventory and refinery data: Weekly U.S. inventory reports and refinery utilization rates will show how supply and demand are balancing as crude prices climb.

- Renewables contracting and procurement: Watch PPA and storage tender announcements in Europe and Australia, plus any government procurement schedules that could expand demand for batteries and solar.

- Critical materials policy: Moves by governments to secure rare earth processing or to limit exports will affect manufacturers and could create winners among companies that secure upstream supply.

- Company-level updates: Earnings, capital expenditure guidance, and project FID announcements from majors and renewables developers will give you signals on cash flow and growth trajectories.

Bottom Line

- Near term, oil market risk is elevated because of the Strait of Hormuz disruptions, and that’s pushing WTI sharply higher and lifting fuel prices for consumers.

- Longer term, the renewables and storage build-out remains robust, with record additions in 2025 and stronger PPA activity, especially in Europe and Australia.

- Supply chains, especially for processed rare earths and battery components, are a crosscutting risk that can slow deployments or raise costs even as demand grows.

- You should expect headline-driven swings in oil and more selective, fundamentals-driven moves in the clean-energy segment.

- Analysts note that this dual reality favors both vigilance on geopolitical news and selectivity among renewable and storage project developers that have secured supply and offtake.

FAQ Section

Q: How is the Strait of Hormuz disruption affecting oil prices? A: The transit slowdown has increased supply risk premiums, helping push WTI about 51% higher over the past month and keeping prices above $100 per barrel.

Q: Will renewable growth slow because of higher oil prices? A: Not necessarily, higher oil raises operating costs for some sectors but data suggests renewables build-out is accelerating, with 692 GW added in 2025 and stronger storage PPA activity.

Q: What should you monitor for supply-chain risks? A: Track policy and trade developments around rare earths and processed materials, vendor backlog disclosures, and company-level supply agreements that can indicate bottlenecks or resilience.