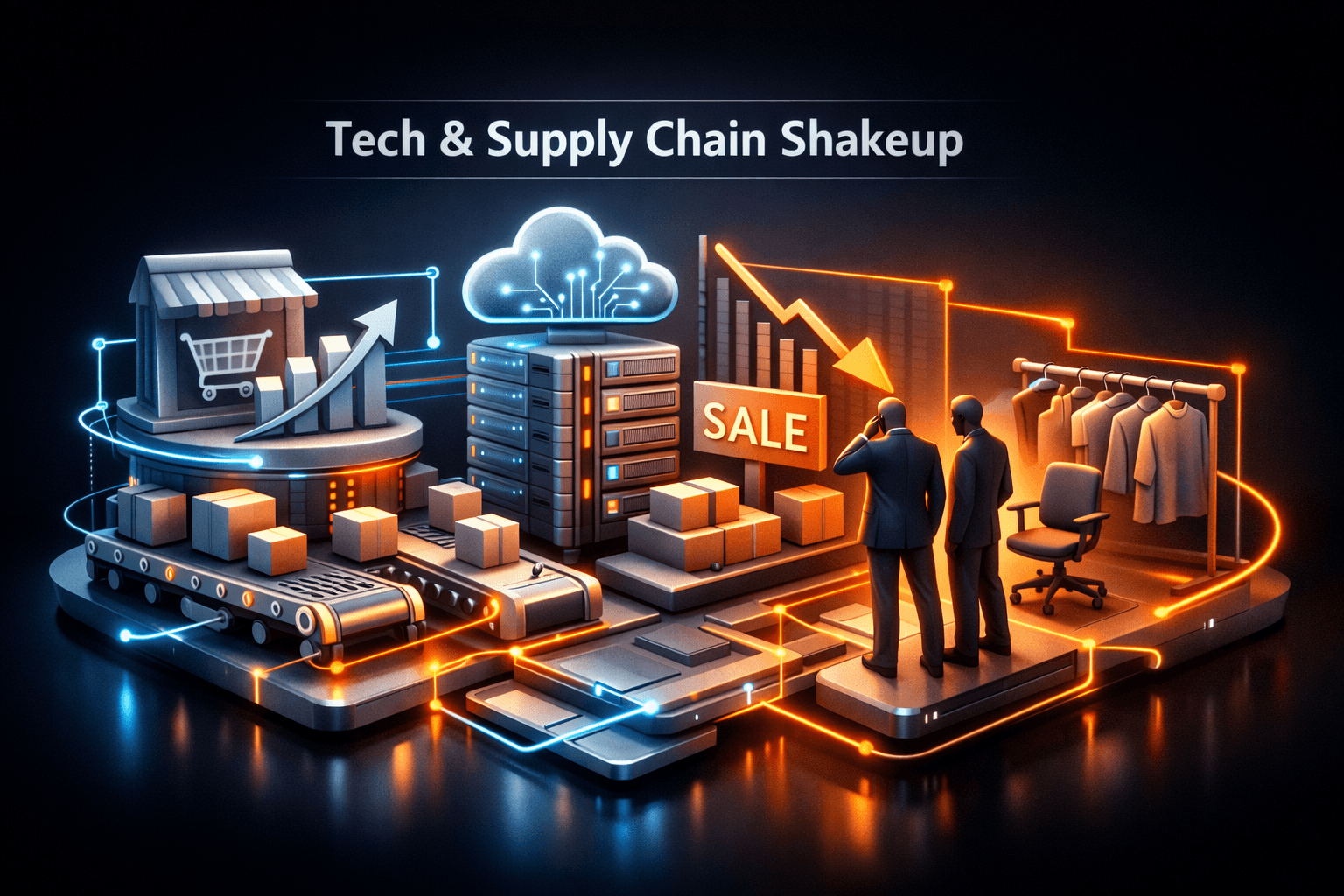

The Big Picture

The consumer and retail sector delivered a day of contrasts on Mar 27, 2026, with technology and capacity investments standing out against persistent execution challenges at some specialty retailers. You saw major vendors and retailers advancing AI, fraud prevention, and distribution capacity, while reports show many merchants still lag in unifying digital and physical operations.

That mix matters because it suggests a sector in transition, where tech and supply-chain upgrades are creating opportunities, but uneven execution and soft comps are keeping risks front and center for your portfolio. How you weigh modernization against near-term retail weakness will matter for positioning into upcoming earnings and seasonal cycles.

Market Highlights

Here are the quick takeaways from today’s leading stories and what moved the conversation in the sector.

- Oracle $ORCL rolled out Fusion Agentic Applications, embedding AI agents across finance, supply chain, and procurement systems, a move likely to accelerate B2B ecommerce automation.

- Skullcandy reported improvements in fraud prevention after working with Riskified, highlighting the revenue and customer-service upside from smarter checkout verification.

- Manhattan Associates $MANH published a benchmark finding just 7% of retailers reach unified commerce maturity, a stark reminder of the execution gap facing many chains.

- Designer Brands $DBI combined its U.S. and Canada reporting to streamline operations, though it posted flat Q4 sales and a comps decline, signaling near-term pressure.

- Shoe Carnival $SCVL paused parts of its Shoe Station rebrand after customer pushback, underlining the risk of merchandising changes during repositioning efforts.

- Fareway broke ground on a 105,000-square-foot freezer expansion to support its stores and future automation investments, a clear capacity bet on regional grocery growth.

- Brown-Forman $BF-B is in talks to merge with Pernod Ricard $RI, a major potential consolidation that would reshape global drinks portfolios and geographic exposure.

Key Developments

AI, automation and checkout tech take center stage

$ORCL's announcement of Fusion Agentic Applications brings AI-driven agents into core back-office workflows, from finance to procurement. That widens the addressable market for vendors selling automation to retailers and suppliers, and it could reduce friction in B2B ordering and fulfillment over time.

At the same time, Skullcandy's work with Riskified shows the tangible ROI of targeted fraud tools, with fewer false declines and fewer service tickets. For you, that means reducing checkout friction can recover lost revenue without increasing fraud risk.

Operations and format risks pop up at specialty retailers

Manhattan Associates' finding that only 7% of retailers have reached unified commerce maturity is a cautionary note. It helps explain why Designer Brands reported flat Q4 sales and a comps decline despite efforts to streamline reporting across the U.S. and Canada.

Shoe Carnival's decision to scale back the Shoe Station conversion after customers reacted poorly highlights how merchandising and format changes can backfire. Meanwhile, Gabe's leadership departures after narrowly avoiding bankruptcy show that off-price chains still face governance and execution hazards. What can retailers do to avoid similar missteps?

Supply-chain capacity and M&A reshape the landscape

Fareway's freezer expansion is a practical example of retailers investing now to shorten delivery cycles and enable future automation. Those kinds of capital moves can improve margins and service over time, especially for regional chains facing growing demand for fresh and frozen items.

On the strategic front, Brown-Forman's talks with Pernod Ricard would be a major industry consolidation, offering scale and a more balanced geographic footprint. If it goes through, analysts note the deal could prompt further consolidation among spirits makers and distributors.

What to Watch

Keep an eye on near-term catalysts and potential downside triggers that could change the tone for the sector tomorrow and into the next quarter.

- Earnings season: Watch retailer same-store sales and margin commentary. Exec remarks on digital integration and inventory will be especially telling.

- Oracle implementation timelines: Faster enterprise adoption of agentic AI could lift vendor revenues and change procurement workflows for retailers.

- M&A progress: Any formal announcement or regulatory filings in a Brown-Forman and Pernod Ricard deal will affect beverage peers and distribution partners.

- Operational execution: Look for follow-up on Shoe Carnival and Designer Brands to see if merchandising and reporting changes translate into comp recovery or further restructuring.

- Supply-chain investments: Updates on Fareway's automation plans and similar distribution builds can indicate which regional players are positioning for durable growth.

If you’re weighing exposure to retail tech or specialty apparel, consider how execution risk and IT modernization timelines affect near-term earnings. Do the long-term automation gains offset short-term sales pressure?

Bottom Line

- The sector shows mixed momentum: technology and distribution investments are positive, but same-store sales and execution issues are limiting near-term upside.

- $ORCL's AI push and tactical moves like Skullcandy's fraud wins point to measurable productivity and revenue recovery opportunities.

- Retailers that fail to integrate digital and physical channels, as the Manhattan Associates study shows, risk margin pressure and lost sales.

- M&A talk in spirits could trigger broader industry adjustments and create consolidation winners and losers.

- Watch earnings, implementation timelines, and any formal M&A steps for clearer signs on who benefits from the tech and capacity investments.

FAQ Section

Q: How will Oracle's AI agents affect retail operations? A: Analysts note Oracle's agentic applications could automate routine finance and procurement tasks, reducing manual workload and speeding B2B transactions once implementations scale.

Q: Should I be worried by the Manhattan Associates finding that only 7% of retailers are mature? A: Data suggests the gap is a structural risk, because retailers lagging on unified commerce may face higher costs and lost sales, so you should watch execution metrics and tech investments closely.

Q: What could a Brown-Forman and Pernod Ricard deal mean for the drinks market? A: Industry commentary points to increased scale and geographic diversification, and such a transaction could prompt further consolidation among large spirits companies and affect distribution economics.