The Big Picture

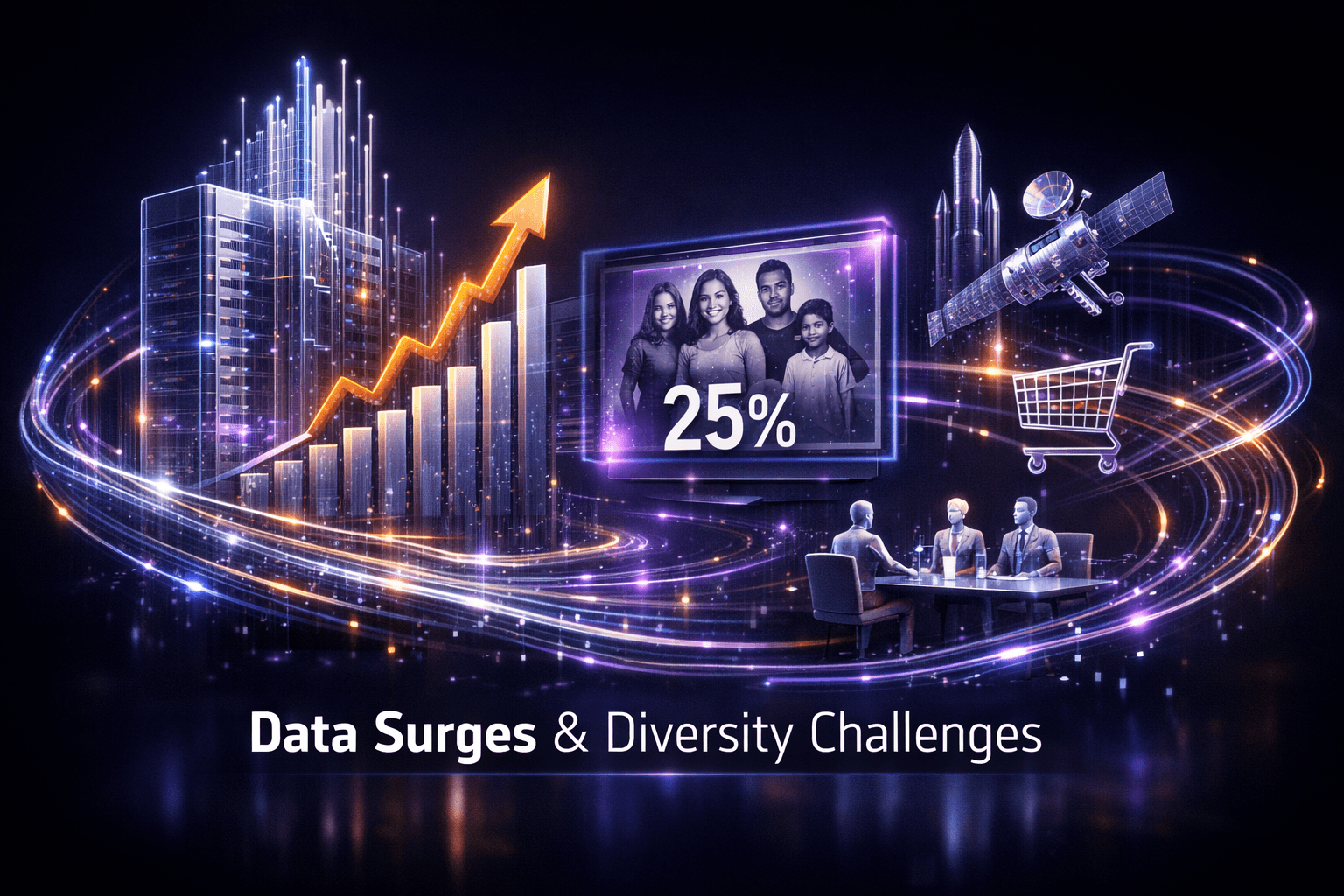

The biggest market development today came from infrastructure: Dell'Oro reports data-center IT semiconductor and component revenue jumped 116% in 1Q 2026, signaling continued capital spending on AI and cloud capacity. That surge has clear implications for carriers, cloud providers, and equipment suppliers across communications and media.

At the same time cultural and programming issues grabbed headlines, with a new report finding Latine immigrant representation in scripted TV has fallen to 25 percent. You might ask, which of these trends matters more to your exposure in the sector? Both shape demand, costs, and reputational risk for media companies.

Market Highlights

Key quick facts and price context from today for investors to track.

- Data-center components up 116% year over year in 1Q 2026, according to Dell'Oro, driven by AI infrastructure expansion and higher memory prices.

- Charter Communications executive Chris Winfrey was elected chair of the NCTA board, a governance move affecting $CHTR and the cable lobby's policy posture.

- Clarus Networks signed to resell Amazon Leo satellite broadband to enterprise and maritime customers, expanding distribution for $AMZN's satellite services.

- Scripted-TV representation for Latine immigrants measured at 25 percent in a Define American and USC Norman Lear Center report covering shows aired July 2023 to June 2025.

- Industry buzz: Venice 2026 festival lineup anticipation, a Prison Break reboot teaser, and ongoing reality-TV developments such as Love Island USA Season 8 continue to generate content momentum.

Key Developments

AI Demand Fuels Data-Center Component Growth

Dell'Oro's 116 percent growth figure for 1Q 2026 is stark. The firm points to AI infrastructure expansion and rising memory prices as primary drivers, which suggests continued order flow for semiconductor suppliers and equipment vendors used by hyperscalers and telcos.

For you watching the supply chain, this means revenue and pricing trends for memory makers and AI chip suppliers will be central to earnings cycles. Analysts note the data reinforces momentum in infrastructure capex, but supply dynamics and product cycles still matter.

Policy and Distribution Moves: Charter, Clarus, and Amazon Leo

Charter CEO Chris Winfrey's election as NCTA chair elevates a major cable operator's voice in Washington. That matters for regulatory and policy areas that affect carriage, broadband subsidies, and wholesale rules for video and connectivity, all of which influence $CHTR's operating backdrop.

Clarus Networks joining as a reseller for Amazon Leo's satellite broadband expands distribution to maritime and enterprise customers. That deal shows providers are layering satellite options into enterprise connectivity stacks, adding a competitive channel for $AMZN's satellite services and creating new addressable markets.

Cultural and Content Signals: Representation and Programming Buzz

The Define American and USC report finding Latine immigrant representation at 25 percent raises reputational and content strategy questions for networks and streamers. The industry quote that it "cannot rely on a few programs to represent the whole" highlights pressure on executives to diversify pipelines and licensing choices.

Content-side stories also included Venice 2026 festival anticipation and franchise activity such as a teased Prison Break reboot and Love Island USA developments. These items keep viewer engagement and licensing discussions alive, even if they don't immediately move market prices.

What to Watch

Look ahead to catalysts and risks that could move stocks and strategies in the communications and media space.

- Earnings season and guidance from large content owners and cable operators, where infrastructure spending trends and subscriber metrics will be scrutinized.

- Memory price movements and semiconductor quarterly results, since Dell'Oro's data suggests these are key drivers for data-center revenue growth.

- Regulatory developments around broadband and video, where NCTA leadership could influence lobbying and rule-making affecting $CHTR and peers.

- Corporate deals extending satellite and edge connectivity, including reseller programs for Amazon Leo and partnerships tying satellite to maritime and enterprise use cases.

- Reputation and content pipeline changes after the representation report, as networks and streamers may face pressure to adjust commissioning and promotion strategies.

How will networks respond to representation criticisms? What will earnings say about capex and margins next quarter? Those are the questions that will guide your watchlist into the coming weeks.

Bottom Line

- Data suggests the infrastructure side of communications is currently the strongest signal, with Dell'Oro reporting a 116 percent rise in 1Q data-center component revenue.

- Distribution and policy shifts are unfolding, highlighted by $CHTR's NCTA leadership and Clarus's reseller deal for $AMZN's satellite service.

- Programming and reputation issues, such as the 25 percent Latine immigrant representation finding, create potential content strategy and public-relations headwinds for media companies.

- Expect mixed earnings takeaways: revenue upside from infrastructure, offset by content and subscriber trends that will vary by company.

- Pay attention to memory and semiconductor pricing, regulatory signals, and content commissioning moves that will affect fundamentals going forward.

FAQ Section

Q: How significant is the 116 percent Dell'Oro figure? A: It indicates very strong year over year demand for data-center IT components in 1Q 2026, driven largely by AI infrastructure buildout and higher memory prices.

Q: Does the representation report affect company revenues? A: Direct revenue impacts are indirect, but reputational and licensing pressure can influence programming strategy, marketing spend, and long-term subscriber sentiment.

Q: What should I monitor tomorrow? A: Watch semiconductor pricing, any company commentary tied to Dell'Oro's findings, policy statements from NCTA leadership, and deal announcements expanding satellite broadband distribution.