Share this article

Spread the word on social media

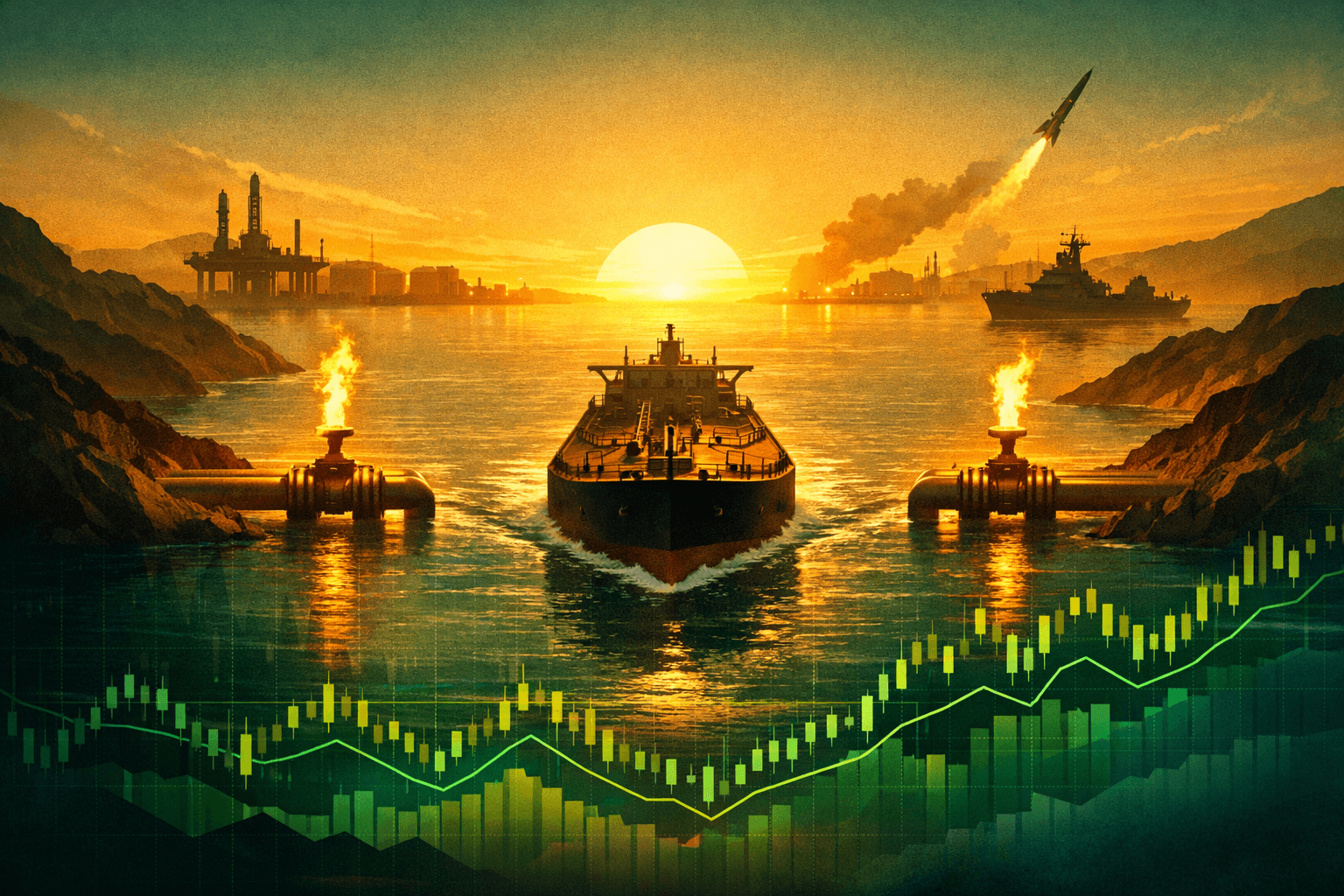

Opening hook: Roughly 20% of seaborne oil runs through a single choke point

About 20 percent of global seaborne oil trade, roughly 21 million barrels per day, transits the Strait of Hormuz, and Iran's recent moves to strengthen control there raise a clear, measurable supply risk. At the same time Saudi Arabia halted operations at several energy facilities, temporarily removing productive capacity from the market.

What happened: Iran tightened controls and Saudi operations paused

This week Iran increased enforcement and naval activity around the Strait of Hormuz, tightening transit procedures for commercial vessels and tankers. Concurrently Saudi authorities paused operational activity at several energy facilities, affecting upstream and midstream throughput in a country whose crude capacity is about 12 million barrels per day.

The two developments are separate but compounding, because the Strait handles crude and product flows originating in the Gulf, including Saudi exports that supply Asia and Europe. The immediate effect is an operational squeeze on seaborne flows that account for millions of barrels per day.

Why it matters: Immediate supply shock, elevated insurance and shipping costs

Even a regional chokepoint disruption of 1 million barrels per day is material; it equals roughly 1 percent of global seaborne oil flows (and about 1% of global oil consumption), but can still materially tighten markets depending on inventories and spare capacity. Markets price chokepoint risk aggressively; in past incidents a short-lived supply scare pushed Brent up 3 to 6 percent within days.

Shipping and insurance costs will rise too. War-risk and Gulf premiums for VLCCs and Suezmaxes have in past episodes risen sharply; premium increases have varied by event and route, and have sometimes moved by tens of percent, adding several dollars to delivered crude cost and compressing refinery margins. That effect shows up in refinery throughput decisions and product crack spreads within 7 to 30 days.

For diversified oil producers, the macro impact is asymmetric. A sustained 1 million bpd effective hit to exports can lift global benchmark prices by $5 to $15 per barrel depending on inventories and spare capacity. Saudi spare capacity and OPEC+ responses matter; Saudi Arabia's advertised spare capacity of around 1 to 2 million bpd is often cited as a key buffer, but actual usable capacity can vary; operational halts reduce that cushion in the short term.

Bull case: Near-term price premium benefits integrated majors and shippers

If the tightening persists for more than 2 to 4 weeks, Brent could reprice higher by $7 to $12 per barrel, restoring cash flows for integrated majors. A $10 per barrel rise in oil typically adds several billion dollars to combined free cash flow across Exxon Mobil (XOM) and Chevron (CVX), improving buyback and dividend optionality.

Tanker owners like DHT Holdings (DHT) and product carriers should see charter rates spike, translating to outsized quarterly revenue if the Gulf remains constricted for 4+ weeks. Energy services companies such as SLB benefit from higher upstream activity and maintenance work triggered by operational disruptions.

Bear case: Quick diplomatic de-escalation, inventories absorb the shock

The worst-case pricing outcome is avoidable if inventories and spare capacity are mobilized fast. OECD commercial stocks and U.S. Strategic Petroleum Reserve releases can substitute for lost seaborne flows; combined OECD inventories ran near multi-year averages, providing a buffer of tens of millions of barrels.

Market history shows geopolitical premiums fade once a diplomatic window opens; in several 2019 to 2022 Gulf flare-ups prices reverted within 10 trading days when shipping lanes reopened or alternative export routes compensated. If Saudi pauses are operationally limited to days rather than weeks, majors' forward earnings will barely move.

What This Means for Investors: Tactical moves and specific tickers

Positioning depends on time horizon and risk tolerance. For event-driven trades over the next 1 to 6 months, overweight XOM and CVX given their scale and the historical leverage of integrated producers to higher oil. Monitor Exxon Mobil (XOM) and Chevron (CVX) for relative strength; a $10 rise in Brent meaningfully expands their free cash flow.

Consider energy ETFs such as XLE for broad exposure, and direct tanker exposure via DHT Holdings (DHT) if you want to play freight-rate upside; short-term call spreads can control cost if volatility spikes. Watch service companies like SLB for a mid-cycle recovery play if upstream activity ramps, and keep an eye on refiners such as Valero (VLO) where margins can compress if product spreads move unfavorably.

Risk management matters: use position size limits because a diplomatic resolution can erase a large portion of any premium within 10 trading days. Set stop-loss levels and prefer options to outright long equity exposure if you expect volatility above 30 percent implied volatility in the near term.

Actionable takeaway: Overweight large integrated producers XOM and CVX for cash-flow leverage, add DHT to play tanker-rate upside, and size positions for a possible quick unwind within 2 weeks.