Share this article

Spread the word on social media

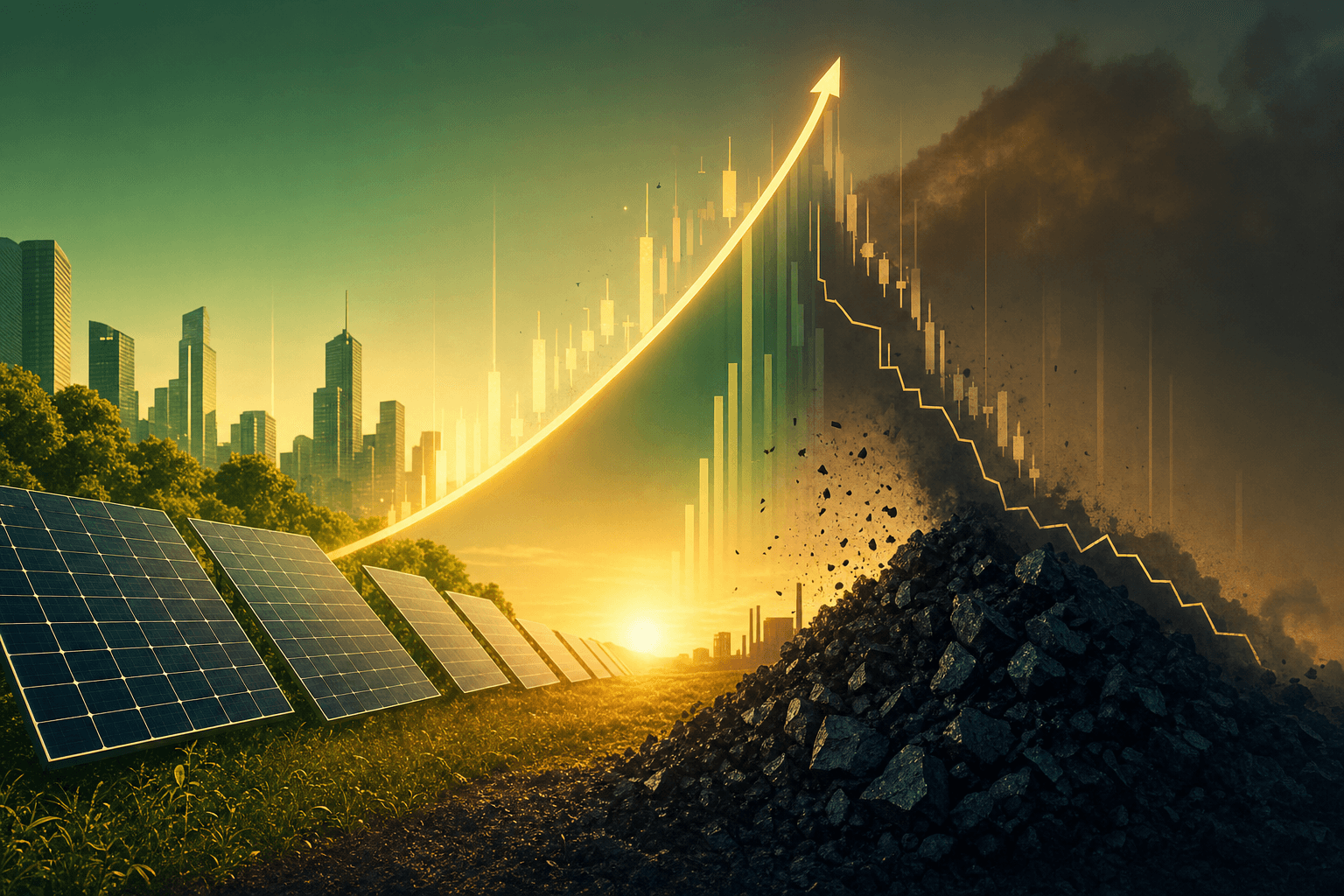

Opening hook: Solar produced more electricity than coal in May 2026

In May 2026 solar panels supplied 12.8% of U.S. electricity, surpassing coal at 12.2% for the first month on record, with solar output reaching a new high of 45.5 terawatt-hours (TWh).

What happened: The numbers, the timing, the source

Ember reported solar's 12.8% share for May 2026, up 17% year over year, and said total solar output was 45.5 TWh that month. Coal generated roughly 12.2% of the electricity mix in May, about 43.4 TWh if total U.S. generation was near 356 TWh for the month.

Solar's share has more than doubled in five years, rising from 5.4% in May 2021 to 12.8% in May 2026, while coal fell from roughly 20% to 12.2% over the same period. Solar now ranks third in the U.S. supply stack behind natural gas and nuclear.

Why it matters: Structural shift with measurable momentum

The 12.8% milestone is not a one-month anomaly, it's the result of sustained growth. A rise from 5.4% to 12.8% in five years implies an implied compound annual growth rate near 18% for solar's share, and the 17% YoY jump in output in May underlines that trend.

The scale matters for markets. Solar producing 45.5 TWh in one month means grid-scale and distributed assets are dispatching at scale across regions. That changes revenue pools for inverter and tracker makers, materials suppliers, and developers, and shifts demand away from thermal coal producers like Peabody Energy (BTU). Coal accounted for about 12.2% of generation in May.

Policy and demand dynamics amplify the technical change. Federal incentives and corporate power purchase agreements continue to accelerate buildouts, while rising power needs from artificial intelligence data centers increase demand for predictable new capacity. The result is faster offtake of projects and deeper order books for suppliers.

The bull case: Why investors should favor solar exposure

If the recent pace continues, solar will capture more of the incremental megawatt growth in U.S. generation. A 17% YoY rise in monthly output and an implied ~18% CAGR in share over five years support a scenario where module and inverter demand remains robust for multiple years.

That favors vertically integrated manufacturers and balance-of-system suppliers. Companies with scale in module production, inverters, or trackers can grow revenues as solar moves from niche to mainstream. Utilities that can pair solar with storage will also monetize higher capacity factors and premium daytime prices.

The bear case: Constraints, seasonality, and grid bottlenecks

Solar's gain is concentrated in sunny months and midday hours. Sunlight produced 45.5 TWh in May, but seasonal and diurnal variability mean average monthly shares can fall dramatically in winter. Interconnection backlogs and transmission constraints remain a material risk; projects can be delayed for months or years.

Storage is not yet ubiquitous. If battery deployment lags, curtailment and depressed marginal prices during peak production could compress project returns. Coal's share fell from about 20% to 12.2% in five years, but remaining dispatchable coal and gas fleets still underpin reliability and can cap price spikes during cloudy or windless stretches.

What this means for investors: specific positions and metrics to watch

Rebalance toward companies with direct exposure to the installed solar base and clear paths to margin expansion. Watch module and cell manufacturers like First Solar (FSLR), inverter and energy-management names such as Enphase Energy (ENPH) and SolarEdge (SEDG), and utility-scale developers like SunPower (SPWR) and NextEra Energy (NEE).

Monitor these three metrics each quarter: (1) backlog or contracted pipeline in gigawatts, (2) average selling price trends for modules and inverters, and (3) curtailment rates or storage attach rates. A sustained increase in contracted GW and stable ASPs indicates durable demand; rising storage attach rates indicate improving realized capacity value.

Be selective on coal exposure. Pure-play coal producers like Peabody Energy (BTU) face structural headwinds if the trend persists. Conversely, companies that can integrate solar plus storage or offer firmed renewable products will capture premium pricing.

For growth investors, consider position sizing limits. Allocate no more than 3% to 6% of a diversified equity portfolio to single solar names, given execution and policy risk. For income-oriented investors, regulated utilities with defined renewable pipelines, such as NextEra (NEE), offer a lower-volatility way to play the transition.

Bottom line: Solar's milestone is real and actionable

Solar surpassing coal in May 2026, producing 12.8% versus coal's 12.2% and delivering 45.5 TWh, signals a structural shift. The implied ~18% CAGR in share and 17% YoY output growth point to durable demand for panels, inverters, trackers, and storage.

Investors should favor scaled suppliers and integrators, watch key operational metrics each quarter, and limit exposure to coal producers. Specific tickers to follow: FSLR, ENPH, SEDG, SPWR, NEE, BTU, and NVDA for indirect exposure through AI-driven power demand.

Actionable takeaway: if solar's monthly growth stays near 15% to 20% YoY and storage attach rates climb, overweight scaled solar equipment suppliers and utility-scale integrators with proven pipelines; trim exposure to thermal coal names lacking diversification.