Share this article

Spread the word on social media

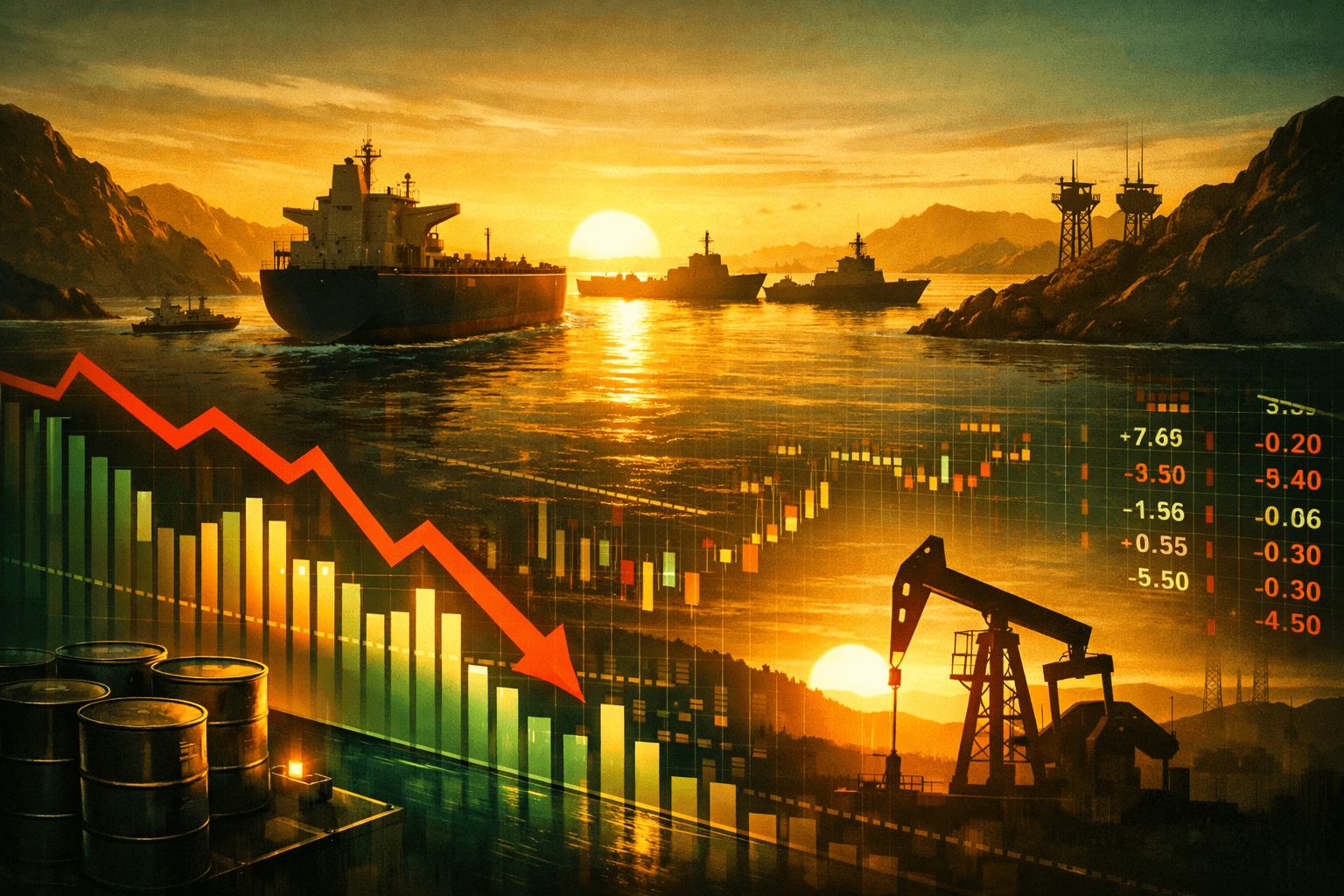

Opening: Brent jumps, global flows cut by a fifth

Brent crude futures spiked sharply, rising about 8% intraday as the United States moved to block maritime traffic through the Strait of Hormuz, which handles roughly 20% of seaborne oil flows, about 20–21 million barrels per day based on historical EIA figures.

What happened: Immediate facts and market moves

The US announced enforcement measures closing the Strait to certain commercial traffic on [date], effectively interrupting oil tankers carrying crude and condensate from the Gulf. Global seaborne crude shipments of roughly 21 million barrels per day are exposed to that chokepoint, and today's market reacted with price moves not seen in months.

Oil benchmarks reflected the supply shock: reports indicated Brent and WTI rose sharply in that session, reportedly by roughly 8% and about 7% respectively, while the US Strategic Petroleum Reserve, reported to hold roughly 350 million barrels, became an obvious policy lever for Washington.

Why it matters: Supply, spare capacity and historical context

This matters because modern oil markets run on tight margins. OPEC+ spare capacity is commonly estimated in the low single millions (roughly 2–3 million barrels per day), though estimates vary and can change quickly, not enough to fully replace a 20 million b/d transit that now faces blockade risk.

History shows how quickly geopolitics can reshape prices. In 1973–74 oil prices effectively quadrupled after the embargo, and in 2008 Brent peaked at about $147.50 per barrel on July 3 as supply worries compounded financial market exuberance. Today's shock is different because global inventories are lower and floating storage is limited, making price moves faster and potentially more violent.

Macro spillovers are immediate. A sustained $10–20 rise in crude prices typically subtracts 0.2–0.4 percentage points from GDP growth in oil-importing countries over a year, while boosting cash flow for upstream producers. That math matters for central banks evaluating inflation and growth tradeoffs.

Bull case: Tight supply lifts majors and services

In the bull scenario, the blockade lasts weeks to months, OPEC+ adds only 1–2 million b/d of spare capacity, and global demand holds near 100 million b/d. That combination pushes Brent beyond $100 per barrel, re-rating upstream earnings. Integrated majors like Exxon Mobil (XOM) and Chevron (CVX) would see free cash flow improvements; Exxon generated about $31 billion in free cash flow in 2022 (operating cash flow for the year was substantially higher), showing how much incremental cash a $10 rise can add.

Energy services and exploration names such as Schlumberger (SLB) and Halliburton (HAL) would benefit if higher prices sustain rig activity and longer-term capex. Private equity and M&A activity could accelerate too, as buyers chase asset-backed cash flows.

Bear case: Demand destruction, policy response, and escalation risk

The bear case flips on three dynamics. First, a prolonged price spike above $100 risks demand destruction: historically, every sustained $10–$20 increase reduces discretionary consumption and slows GDP, pressuring oil demand growth below current ~1–1.5 million b/d forecasts.

Second, coordinated SPR releases or diplomatic de-escalation could bring supply back quickly; a coordinated release of 50–100 million barrels globally would blunt price moves and cap gains for producers. Third, escalation risk is asymmetric: full military confrontation would disrupt broader trade and equity risk premia, spiking volatility and depressing cyclicals including energy in a risk-off rout.

What this means for investors: actionable takeaways and tickers to watch

For investors, this is a short- to medium-term trade on supply shock, not a permanent structural thesis. If the blockade holds longer than 30–60 days, favor integrated producers and certain E&Ps with low decline rates: XOM, CVX and Occidental Petroleum (OXY) are primary longs, as each has either diversified refining exposure or strong upstream cash flow.

Energy services like SLB and HAL are tactically attractive if drillers restart wells, but they carry operational cyclicality so use time-limited positions. Refiners such as Valero (VLO) and Phillips 66 (PSX) are mixed; if crude rises faster than product cracks, refiners' margins compress, so hedge exposure or prefer refiners with global logistics.

Hedge ideas: buy XOM/CVX call spreads to capture upside while limiting premium, or buy SLB on a pullback. Protect portfolios with short exposures to airlines like American Airlines (AAL) and Delta (DAL), which see fuel cost blows directly. Monitor key triggers: 1) OPEC+ announcements, 2) SPR release size in millions of barrels, and 3) shipping insurance spreads that can double maritime costs within days.

Risk management: cap position sizes because geopolitical events are binary and sentiment can flip. A coordinated SPR release of 50–100 million barrels or a diplomatic reopening would likely erase a large portion of near-term gains in energy equities.

Investor takeaway: Treat this as a supply-driven, time-sensitive opportunity. Favor integrated oil majors (XOM, CVX), selectively add energy services (SLB), avoid unhedged refiners without logistics advantages (watch VLO, PSX), and size positions for binary geopolitical outcomes.---