Share this article

Spread the word on social media

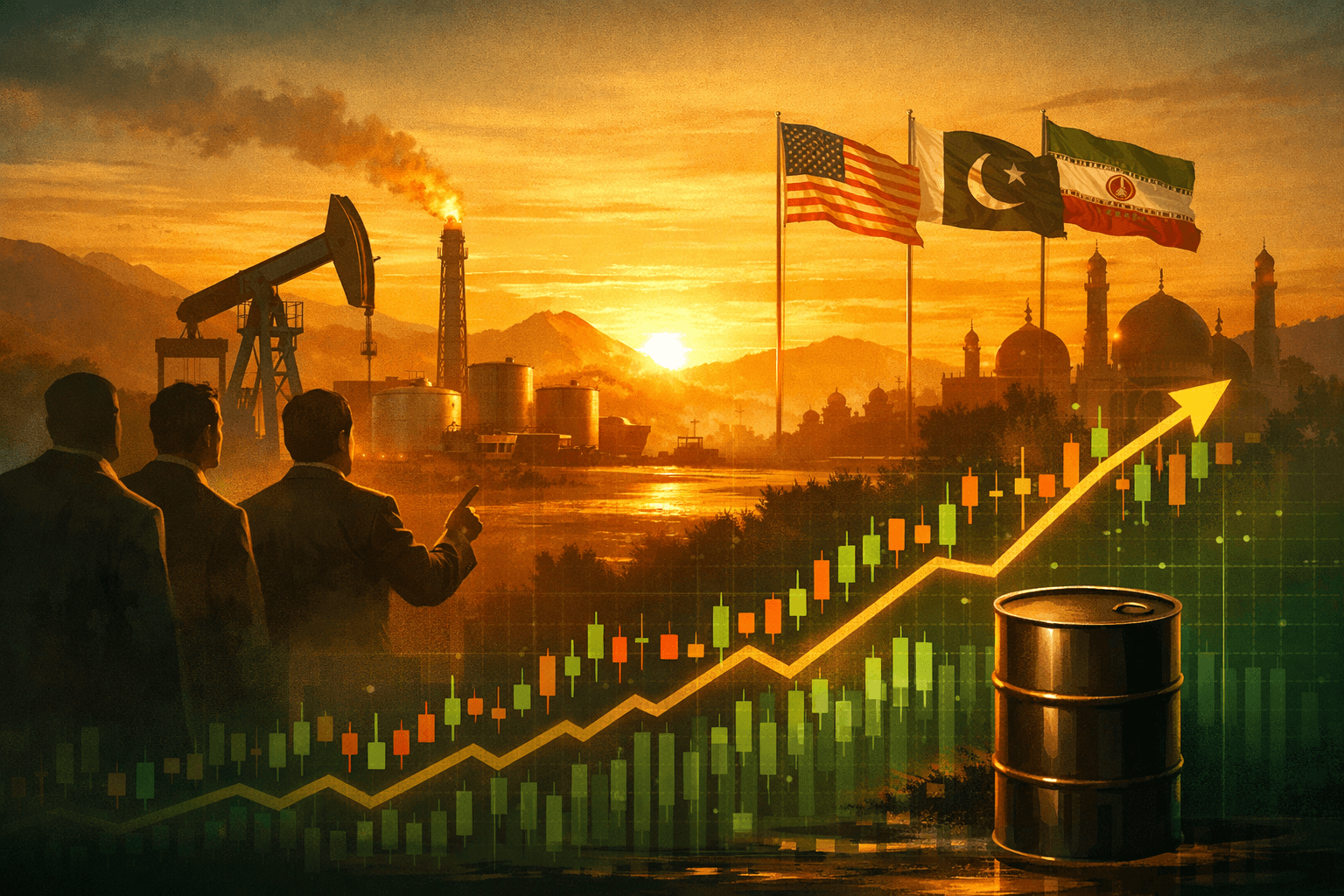

Opening hook: Brent tops $95 as a two-week truce nears expiry

Brent crude futures were reported around $95 per barrel after President Donald Trump said U.S. negotiators will meet in Pakistan on Monday, while a fragile two-week ceasefire with Iran is set to expire on Wednesday. Over the weekend the U.S. seized an Iranian-flagged vessel in the Gulf of Oman, a concrete escalation that lifted risk premia across energy and shipping markets.

What happened: delegation, seizure and a ticking clock

The U.S. dispatched a negotiating team to Pakistan to pursue a diplomatic follow-up to a truce that began roughly two weeks ago, with talks scheduled for Monday and the truce scheduled to lapse on Wednesday. Iran denied it had committed to attend, creating uncertainty about whether diplomacy will prevent renewed strikes on shipping lanes.

Compounding the diplomatic drama, U.S. forces seized an Iranian-flagged vessel in the Gulf of Oman over the weekend, an action linked to allegations of ceasefire violations in the Strait of Hormuz. The Strait handles an estimated roughly 17 to 21 million barrels per day of seaborne oil flows depending on the year, a number that explains why any threat to its openness immediately moves prices.

Why it matters: supply concentration, low spare capacity and historical precedence

The oil market is acutely sensitive to disruptions in the Gulf because global spare capacity sits in low single-digit millions of barrels per day. A 5 percent disruption of the roughly 21 mb/d of seaborne flows equals about 1.05 mb/d of effective lost supply, far larger than routine weekly inventory swings.

History shows how quickly markets reprice geopolitical risk. The September 2019 drone strike on Saudi facilities pushed Brent up roughly 10 percent intraday (with some intraday measures spiking higher). That episode forced refiners and traders to scramble for crude and highlighted how little buffer exists when major exporters face outages.

Shipping matters too. Tanker capacity names and freight rates can re-rate quickly. A short-lived closure of Hormuz in past incidents pushed spot tanker freight rates higher by multiples in days, translating into cost pass-through for refiners and consumers.

The bull case: small disruptions create outsized price moves

If the delegation fails to secure a written agreement by Wednesday and Iran or proxy forces resume attacks, even a limited disruption of 1 mb/d would force markets to reprice immediately. At $95 per barrel, an incremental $5 to $10 rise is plausible within days, lifting sector ETFs such as XLE and majors like XOM and CVX on relative strength.

Energy services and shipping would also benefit. Schlumberger (SLB) and Valero (VLO) could see margin expansion from higher utilization and refining spreads, while tanker plays like Nordic American Tankers (NAT) and Ship Finance (SFL) would gain if freight rates spike by 2x to 3x.

The bear case: diplomacy, demand erosion and headline-driven reversals

A written agreement or an operational de-escalation before Wednesday would likely reverse much of the price move, pushing Brent back toward the low $80s or high $80s within days. Geopolitical premiums tend to evaporate quickly when shipping lanes reopen, as happened after prior episodic flare-ups in the Gulf.

On the demand side, persistent concerns about a global slowdown can mute rally sustainability. If Brent breaches $100 and stays there, demand destruction can accelerate within 1 to 3 quarters, hitting refining margins and slowing economic activity in countries heavily dependent on oil imports.

What this means for investors

Immediate strategy: treat this as a tactical, event-driven trade window, not a regime change. Consider a 2 to 4 percent tactical allocation to energy exposure if you have conviction the truce collapses. Target large-cap producers XOM and CVX for balance-sheet resilience, and use XLE for sector exposure.

- Hedged long: buy call spreads on XOM or XLE with 6 to 12 week expiries to limit downside while capturing a 10 to 20 percent upside if Brent re-rates.

- Shipping play: short-duration exposure to NAT or SFL can pay off if tanker spot rates double; size positions small and use stop losses because freight is volatile.

- Defense hedge: allocate 1 to 2 percent of portfolio to defense contractors like RTX or LMT as an asymmetric geopolitical hedge.

- Downside protection: use short-dated puts on high-beta discretionary names or buy inverse oil ETFs only as temporary hedges against a quick unwind.

Watch these data points this week: Brent price, U.S. Strategic Petroleum Reserve draw or refill announcements, weekly EIA inventory change in millions of barrels, and any confirmed shipping lane closures measured in lost cargoes per day. Each of those numbers will drive 1 to 3 percent moves in related equities.

Investor takeaway: be tactical. Position for a short-term oil risk premium with limited, hedged exposure to XOM, CVX, SLB and select tanker names, while keeping capital ready to trim if diplomacy materializes before Wednesday.

We are bullish on near-term oil and related equities given the asymmetric supply risk, but the trade requires active monitoring and disciplined position sizing because the situation can reverse in days if talks succeed.