Share this article

Spread the word on social media

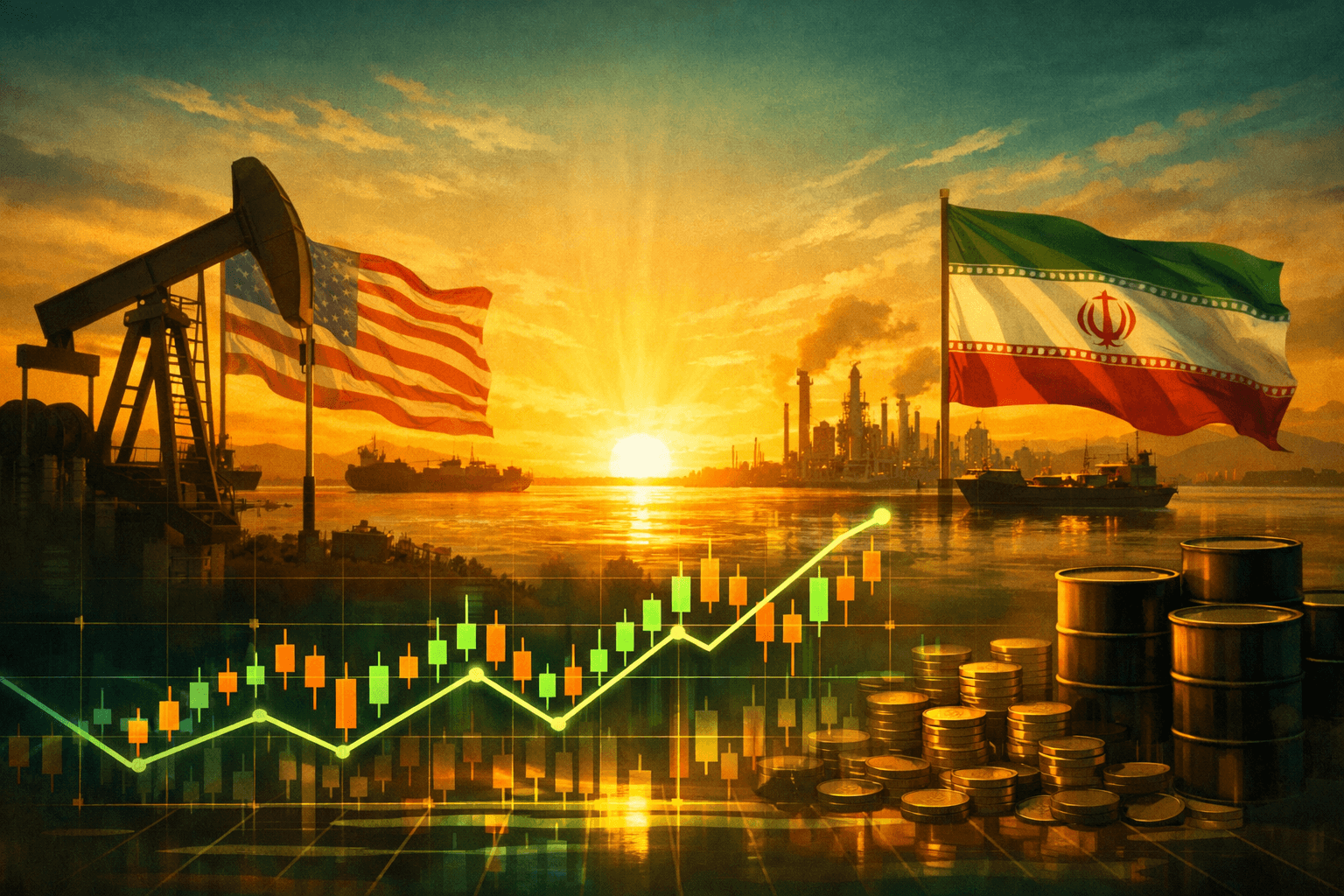

Opening hook: Markets shrugged as oil dropped nearly 15%

WTI crude prices plunged nearly 15% on the ceasefire announcement, while U.S. stock futures reportedly jumped roughly 1.5% within hours of the news. The sudden move erased part of the risk premium built into oil and equity prices over the past six weeks, and it matters for portfolios that had been hedging geopolitical risk.

What happened: Two-week ceasefire and safe passage through Hormuz

Washington and Tehran agreed to a two-week ceasefire that includes coordinated passage for commercial vessels through the Strait of Hormuz, which historically carries about 21 million barrels per day, roughly 20% of seaborne crude. Iran said passage would happen in "coordination with Iran's Armed Forces and with due consideration of technical limitations," and both sides framed the arrangement as temporary, lasting 14 days.

Markets reacted immediately. Oil fell nearly 15% from intraday peaks and the S&P 500 futures rallied about 1.5%, while the CBOE VIX pulled back approximately 6% from levels earlier in the week. The International Monetary Fund warned that higher prices and slower growth remain a risk even if hostilities pause, which keeps the macro picture complicated.

Why it matters: Supply, shipping and the fragility of the risk premium

The Strait of Hormuz is not symbolic, it is economic. About 21 million barrels per day transit the Strait at peak, so even short disruptions affect seaborne balances quickly. A 14-day window lowers immediate supply fears, but it does not eliminate the structural uncertainty that pushed Brent to multi-month highs earlier.

Spare production capacity matters now. OPEC+ spare capacity is in the ballpark of 3 to 4 million barrels per day today, which can cushion short shocks, but that buffer is thin relative to a sustained blockade. The U.S. Strategic Petroleum Reserve holds roughly 415 million barrels, but SPR releases take policy coordination and time to affect the market. Those numbers mean a two-week corridor buys breathing room, not a permanent solution.

History shows markets overreact both ways. In 2019 maritime attacks and seizures around Hormuz produced volatility spikes of 4% to 7% for Brent in days, not weeks. By contrast, the Iran-Iraq war in the 1980s drove sustained price dislocations exceeding 20% over months. The current ceasefire reduces immediate tail risk, but it raises the premium on political intelligence and operational risk in shipping lanes. Traders will pay for that intelligence, and that creates asymmetric opportunities for information-sensitive assets.

The bull case: Risk premium unwinds, cyclical names rally

If the ceasefire holds for the full 14 days and container flows resume meaningfully, oil could retrace a large chunk of its recent spike. A 10% to 20% drop from peak levels is plausible, which would relieve immediate pressure on transportation costs and input inflation. Airlines like Delta Air Lines (DAL) and American Airlines (AAL) would get a direct benefit from cheaper jet fuel, while consumer discretionary and industrials could see margin relief.

Major integrated oil companies like Exxon Mobil (XOM) and Chevron (CVX) would likely give back some multiple expansion tied to geopolitical premiums, but their cash flow profiles stay robust. Investors could use a short-term oil pullback to accumulate high-quality energy names that yield 3% to 5% and buy cyclical leverage elsewhere in the market.

The bear case: Fragile deal collapses, oil spikes back above $100

The ceasefire is explicitly temporary at 14 days, and the operational language leaves room for incidents. If the corridor breaks down, oil could snap back and test levels above $100 per barrel within a few trading sessions, reintroducing inflationary pressure. That outcome would hurt real returns for equities, push 10-year Treasuries higher, and force the Federal Reserve to reconsider rate guidance.

Defense contractors like Lockheed Martin (LMT) and Northrop Grumman (NOC) are natural hedges if the conflict resumes, but they trade with longer-duration defense budgets embedded in valuations. Shipping equities and container lessors would see freight rates spike, creating short-term winners and losers across logistics chains.

What this means for investors: Tactical steps and tickers to watch

Time horizon matters. For the next 14 days, treat positions as event-driven. If you are risk-on, reduce hedges that were sized for prolonged disruption and consider adding cyclical exposure at the margin. If you are risk-off, use any oil retracement to pare positions in energy names that rallied on the conflict.

Key levels and indicators to monitor: WTI at $80 and $100 are practical triggers, the 10-year Treasury yield moving above 4.0% would signal market repricing, and global shipping rates rising 10% week over week would indicate renewed disruption. Watch oil ETFs like United States Oil Fund (USO) for short-term exposure, and energy majors Exxon Mobil (XOM) and Chevron (CVX) for cash-flow resilience.

Tickers to watch: XOM, CVX, USO, DAL, AAL, ZIM (container operator), LMT, NOC. Also monitor macro cues such as the 10-year yield and the CBOE VIX for volatility regime shifts. For active traders, set stop losses around 6% to 8% on directional positions given the high event risk.

Bottom line: the two-week ceasefire is a relief rally, not a reset. Treat this window as an opportunity to rebalance, not to assume the geopolitical risk premium has permanently evaporated. If you trade the headlines, keep position sizes modest and use price triggers at $80 and $100 per barrel to scale exposure.

Investor takeaway: use the 14-day corridor to shift from insurance to opportunity, but size positions for blowback; monitor WTI at $80 and $100 and watch XOM, CVX, USO and DAL closely.