Share this article

Spread the word on social media

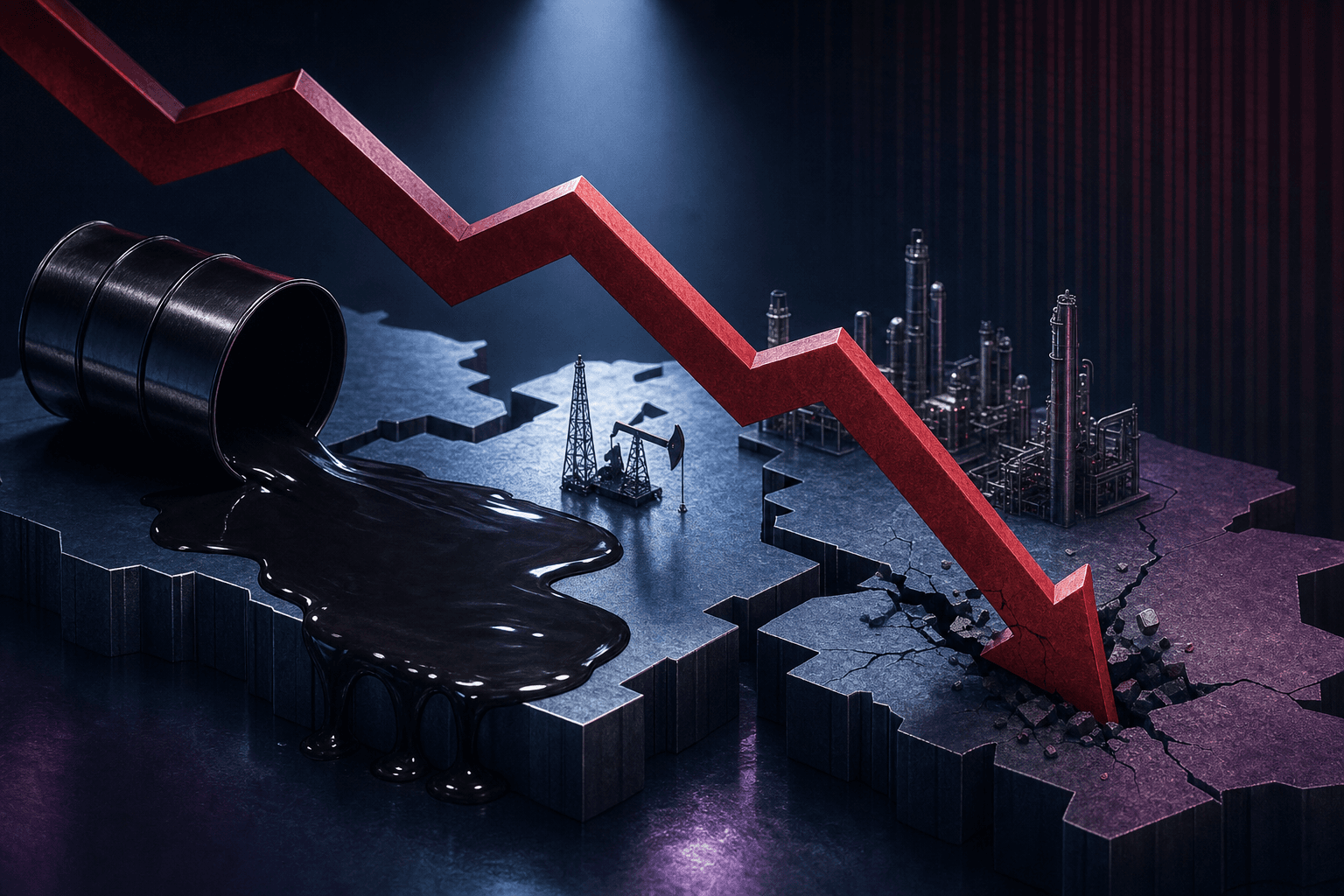

Opening hook: WTI slips under $75 for first time since Feb. 24, 2022

Reportedly, on June 24, 2026 WTI crude fell below $75 per barrel, which, if confirmed, would be the first close under that threshold since the start of the Russia-Ukraine war on February 24, 2022. The move cuts straight into energy earnings assumptions, and it changes the risk calculus for large-cap oil names and cyclical investors.

What happened: price, timing, and immediate market reaction

Market reports indicate WTI traded beneath $75 on June 24, after easing throughout June from levels above $85 in late spring — roughly a 12 percent decline over about six weeks, according to market sources. Brent crude reportedly tracked lower as well, trading in the high $70s, leaving refiners, producers, and service companies repricing near-term cash flow expectations.

U.S. equities reflected the rerating; the S&P 500 energy sector — roughly 5 to 6 percent of the index — reportedly underperformed the broader market intraday. Heavyweights ExxonMobil (XOM) and Chevron (CVX) are the clearest near-term casualties, given their scale and direct exposure to crude realizations.

Why it matters: earnings, macro and historical context

Oil below $75 matters because it removes a key tailwind that sustained the energy complex since 2022. Integrated majors and E&P companies priced budgets, dividends and buybacks assuming a multi-year band of $70 to $85 per barrel. A sustained drop beneath $75 compresses upstream free cash flow; for many U.S. E&P names a $10 move in WTI can swing free cash flow by tens to hundreds of millions of dollars per quarter.

Historically, crude shocks translate quickly into equity responses. Look at 2014-2015, when Brent fell from about $110 to about $50 — roughly a 55 percent decline. That period prompted many producers to cut capex, in many cases by substantial amounts (often reported in the 20 to 40 percent range), and led to multi-year share-price declines at some companies. The current decline is smaller, about 12 percent over six weeks, but the lesson holds: producers cut investment fast, and that amplifies cyclicality for drillers such as ConocoPhillips (COP) and Occidental (OXY).

Macro spillovers are real. Lower oil takes pressure off headline inflation, potentially reducing the Federal Reserve's need to tighten, while also signaling weaker global demand. China demand metrics have been soft this quarter, and a 1 million barrel per day swing in global consumption or supply can move prices materially. With spare OPEC+ capacity limited relative to pre-2014 levels, even modest demand weakness has outsized market effects.

The bull case: cheaper feedstock, defensive earnings and smarter capital allocation

The constructive view is straightforward, oil below $75 is net positive for consumers and for sectors that pay and receive fewer energy costs. Airlines and transport operators see margin relief, while consumer spending can benefit from lower pump prices. Integrated majors benefit on the downstream side; lower crude often widens refining margins temporarily, which helps companies like Chevron and ExxonMobil offset upstream pressure.

On capital allocation, sustained lower prices force discipline. If prices dip to the low $70s, many E&P firms will accelerate payout-focused strategies, converting capex into higher dividends or buybacks. That makes names such as ConocoPhillips (COP) and Occidental (OXY) potentially interesting for income-oriented investors if production guidance is trimmed and returns to shareholders rise.

The bear case: margin squeeze for producers and higher equity risk

The bearish view is that prices under $75 are a direct hit to upstream cash generation, forcing producers to cut capex and delaying projects with positive long-term returns. For pure-play explorers and producers, a 10 percent to 20 percent lower oil price can translate into double-digit declines in free cash flow and equity valuations. That raises insolvency risk for high-leverage names and prompts dividend cuts at the margins.

From a market-structure perspective, falling prices that reflect weak demand increase the probability of prolonged volatility. If WTI continues below $75 and global growth indicators deteriorate, the sector's earnings revisions will outpace the broader market, putting sustained pressure on XOM, CVX, COP, and energy services like Schlumberger (SLB).

What this means for investors: concrete steps and tickers to watch

First, reassess exposure to pure E&P stocks. Reduce concentrated positions in high-cost, high-leverage drillers; target a maximum of 2 to 4 percent portfolio weight in speculative upstream names until guidance is updated. Watch ConocoPhillips (COP) and Occidental (OXY) for revised capital plans, they will be the fastest to announce cuts if prices stay low.

Second, favor integrated majors with diversified cash flow. Integrated majors such as ExxonMobil (XOM) and Chevron (CVX) typically have downstream and chemical operations that can help offset weaker crude realizations; their dividend yields have been in the mid-single digits historically but vary over time, so check current yields before assuming a 3 to 4 percent range. Monitor refining margins; if they widen, refiners like Valero (VLO) and Marathon Petroleum (MPC) could outperform even while crude declines.

Third, opportunistic trades for risk-tolerant investors include energy services and equipment suppliers. Schlumberger (SLB) and Halliburton (HAL) are cyclical plays that may offer high beta exposure to any rebound, but only after activity indicators such as the U.S. rig count and capex guidance improve by 10 percent or more.

Finally, hedge macro exposure. Consider short-duration protective positions via energy ETFs like XLE or the oil futures-backed USO, size hedges to no more than 1 to 2 percent of portfolio value, and be ready to redeploy if WTI breaks back above $85 on a sustained basis.

Investor takeaway: trim speculative E&P exposure, favor large integrated majors XOM and CVX for stability, and use hedges or selective service names for tactical upside.