Share this article

Spread the word on social media

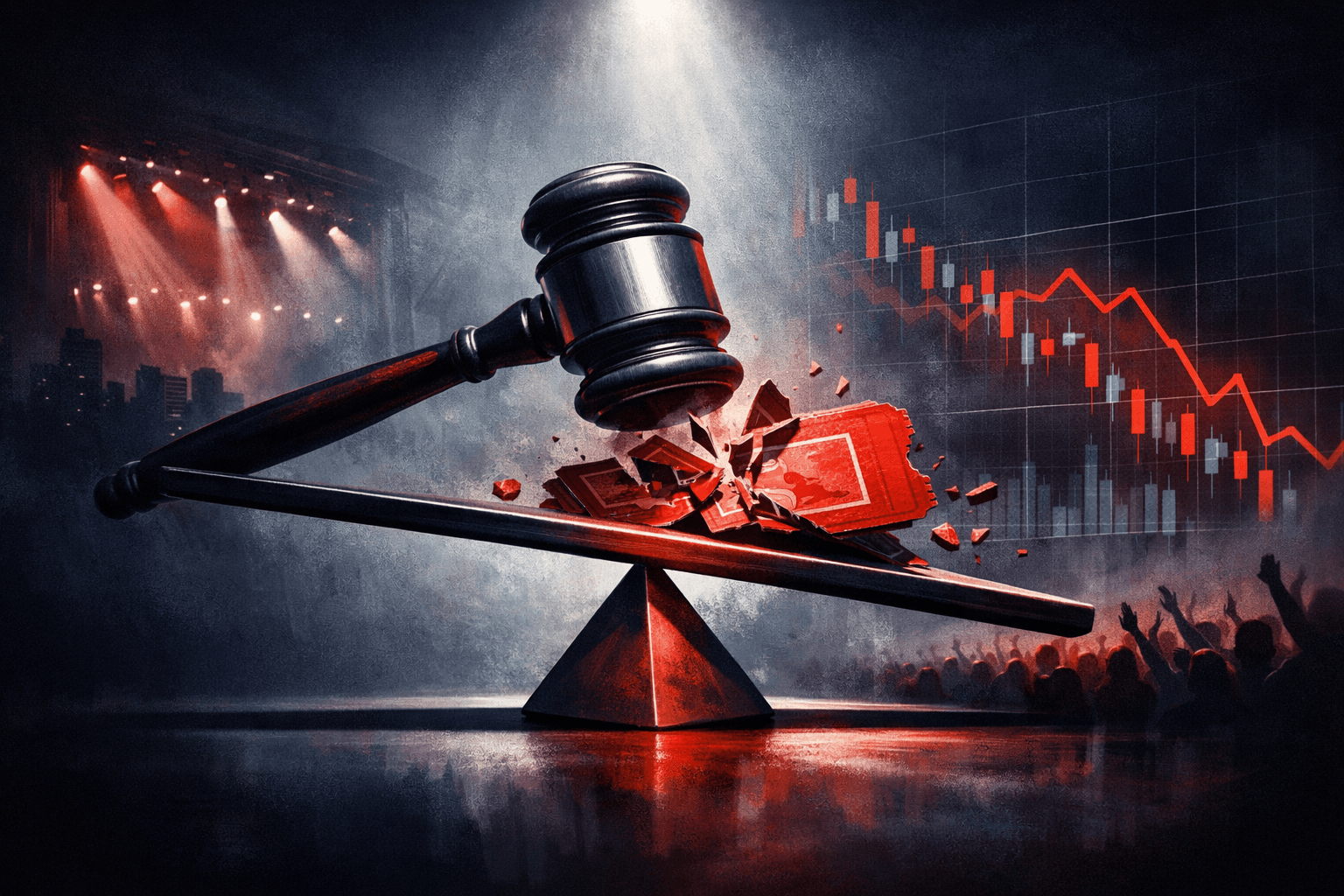

Opening hook: Jury rules Live Nation an illegal monopoly on April 15, 2026

On April 15, 2026 a federal jury found Live Nation and Ticketmaster operated as an illegal monopoly, a verdict that immediately turns one of the music industry's dominant businesses model inside out. The decision moves the case into a second phase where judges will decide remedies and monetary awards.

What happened: Verdict hands states a win and starts Phase 2

The jury verdict is the outcome of a multi-state antitrust suit that resumed after the Department of Justice pursued a settlement, and it rejects the last-minute deal in favor of a court determination. The trial now enters Phase 2, which will quantify damages and could order structural or behavioral remedies.

Legal exposure is significant because U.S. antitrust law allows for treble damages, meaning plaintiffs could seek up to 3x actual damages, and a judge can impose conduct restrictions that alter Live Nation's (LYV) core Ticketmaster operations. Expect the remedy discussion to unfold over months, not days.

Why it matters: This threatens a decade-long business model built since the 2010 merger

Live Nation merged with Ticketmaster in 2010, creating an integrated promoter-primary-ticketing behemoth. That integration underpins LYV's revenue streams across promotion, primary ticketing, and venue services, and it helped push the company to national scale over the last 16 years.

The jury ruling strikes at the commercial logic that allowed Live Nation to bundle services and extract fees. If judges impose divestitures or long-term behavioral remedies, revenue mix and margins could shift materially. Antitrust remedies in comparable U.S. cases have taken years to implement; Microsoft’s antitrust case began in the late 1990s, and appeals and remedial actions unfolded over several years with competitive effects that lasted roughly a decade.

For investors, the verdict raises two direct financial risks: potential damages in the hundreds of millions or billions, and structural change that could reduce synergies and pricing power. Either outcome would likely pressure LYV's profitability metrics, where ticketing fees and promoter economics directly feed operating margins.

The bull case: The business survives, fees remain sticky, and alternatives lag

On the upside, Live Nation has scale advantages that are hard to replicate. LYV owns exclusive promoter deals and long-term venue relationships that represent years of contract value and bargaining leverage; undoing those relationships is operationally painful and legally complex. That gives management runway to negotiate remedies that preserve core economics.

Investors who lean bullish argue the practical cost of splitting Ticketmaster out, or imposing strict conduct rules, could depress ticket volumes temporarily but not eliminate Live Nation’s market access. In past industry reconfigurations, incumbents retained material share because competitors lacked national promoter networks. If that pattern repeats, LYV could reprice or restructure fees while keeping many revenue lines intact.

The bear case: Treble damages and break-up risk could erode valuation sharply

The bear case is straightforward, and it is dangerous: the court could award trebled damages, potentially reaching into the billions if aggregated consumer and competitor claims proceed. Even without massive fines, mandatory divestiture of Ticketmaster or restrictions on exclusive promoter agreements would remove key synergies that underwrite current margins.

Beyond direct legal costs, reputational damage and higher regulatory scrutiny create living risk. Management may need to spend years complying with monitoring and behavioral injunctions, increasing operating costs and lowering return on invested capital. If remedies force LYV to surrender primary ticketing control for large venues or to open promoter contracts, revenue and EBITDA could fall by multiples analysts currently are not pricing in.

What this means for investors: Practical portfolio moves and tickers to watch

Time horizon and position size matter. In the next 6-12 months expect liquidity events as institutional holders re-price LYV based on judge decisions and potential appeals. For traders, volatility will present short-term opportunities; for long-term holders, outcomes hinge on remedies and cash-flow resilience.

- LYV (Live Nation Entertainment)

- Vivid Seats: Potential beneficiary. A forced opening of primary ticketing or diminished Ticketmaster dominance creates an opening for competitors; Vivid Seats could gain market share if it scales distribution, expect positive re-rating potential if conversion costs stay manageable. (Verify current ticker symbol on your trading platform.)

- MSGE (Madison Square Garden Entertainment)

- SPOT (Spotify)

Actionable checklist: reduce LYV exposure to a targeted weight if you have a short-term risk mandate, initiate selective exposure to Vivid Seats and venue owners on any confirmed remedy that limits exclusive promoter-ticketing ties, and monitor legal filings closely for estimated damages ranges. Expect judge rulings and appeals to take at least several months, and plan for higher volatility during that window.

Investor takeaway: The jury verdict is a structural inflection point for LYV. Reduce outright exposure until remedies and damages are quantified, but reweight into credible secondary and venue plays if the market confirms forced opening of ticketing markets.