Share this article

Spread the word on social media

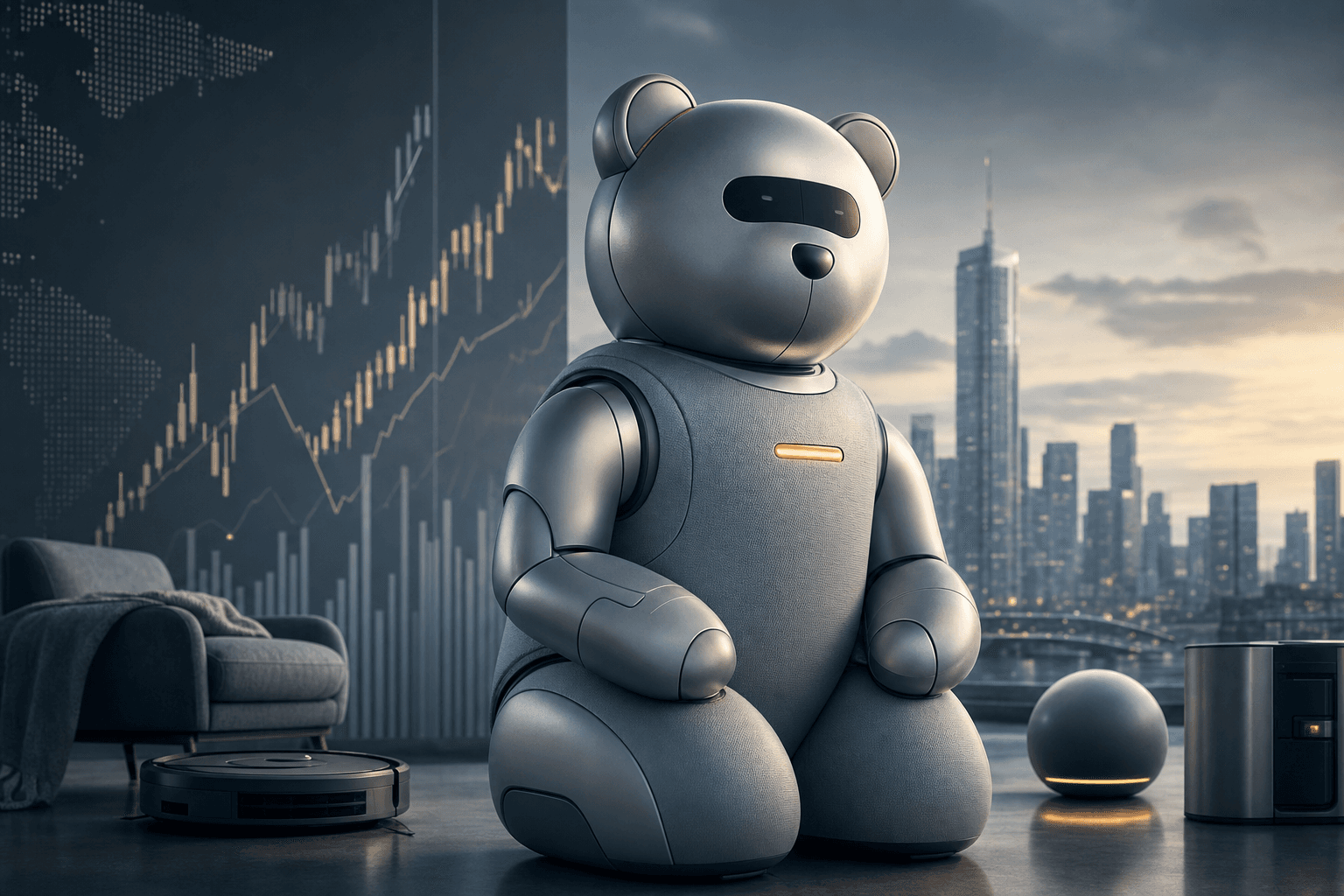

Opening hook: Two years and one prototype changes the conversation about robots

According to reports, a former iRobot CEO spent about 24 months building what is described as an "abstracted bear," a single prototype intended as a robot companion. Two years of effort by a leader who helped scale Roomba matters, because it signals a renewed push from veteran hardware executives into emotionally framed consumer robotics.

What happened: A prototype, not yet a product, aims at companionship

The project is reportedly a purpose-built robot companion that the ex-CEO developed over about 24 months and presented as an "abstracted bear" form factor. At this stage there is one physical prototype and a stated focus on emotional interaction rather than cleaning or industrial tasks.

That makes this different from iRobot's core business, which commercialized the Roomba cleaning robot after its 2002 launch. This new effort targets long-duration engagement and daily presence, not single-task automation, which implies a different product roadmap and unit-economics profile.

Why it matters: Companion bots rewrite the addressable market assumptions

Consumer robotics has historically been a niche, with large hits like Roomba capturing scale by solving a narrow, repeatable pain point. Roomba moved from early hobbyist interest to mainstream adoption because it delivered a clear, measurable outcome, and companies could rationalize margins and replacement cycles. Roomba's commercialization began in 2002; a companion robot attempts to create recurring value that is harder to quantify.

Demographics and long-duration engagement give this idea legs. By 2030 roughly 20 percent of Americans will be age 65 or older, creating demand for in-home assistance and social engagement. If a companion robot reaches even 1 percent of U.S. households, that is roughly 1.3 million units based on the current ~130 million households figure, and that scale would reshape revenue opportunity for entrants and suppliers.

Technology supply chains matter. Modern companion robots will need sensors, compute and AI stacks. Companies like NVIDIA (NVDA) provide the GPUs and inference platforms that accelerate perception, while Sony (SONY) has precedent with Aibo — released in 1999 and relaunched in 2018 — which was positioned as a robotic pet demonstrating consumer emotional engagement and shows that emotionally framed robots can coexist in the market. Cloud and edge economics will determine whether these devices sell for $500, $1,000 or $2,000, and each price point implies very different adoption curves.

The bull case: veteran leadership and a large, under-monetized market

Veteran founders with category experience shorten the learning curve. The ex-iRobot CEO brings operational knowledge from scaling product design, supply chain and retail distribution, and that can compress time-to-market from prototype to commercial launch. If the product hits an MSRP in the $1,000 to $2,000 range and pairs hardware sales with recurring services, the lifetime value could support meaningful margins.

There is an incumbency angle for chipmakers and cloud providers. A credible entrant could secure partnerships for compute and AI, generating non-linear economies of scale. If the device achieves modest penetration, public suppliers such as NVDA and Amazon (AMZN) that provide cloud and inference infrastructure stand to benefit through compute and service revenues.

The bear case: high price, slow adoption and uncertain unit economics

Companion robots face the same challenges that limited earlier consumer robots: cost, utility, and replacement cycles. Sony's Aibo showed emotional engagement in 1999 and again in 2018, but it remained a premium niche toy.

Behavioral adoption is also uncertain. Consumers bought Roombas because they saved time and delivered quantifiable outcomes. Companionship is subjective, and sustaining daily engagement at scale is harder. If the product does not build a sticky ecosystem of services, retention may fall short and ARPU will be low, making the entire business uneconomical without massive scale.

What this means for investors: tactical ways to play a long-term idea

Short term, this remains a speculative founder-stage story with one prototype and two years of development, not a public company pivot. Investors who want exposure to the concept without private rounds should focus on suppliers and ecosystems, not the founder's new venture directly.

- Watch IRBT, the legacy iRobot player, for strategic moves or partnership signals. If the new project proves consumer appetite, IRBT could respond with its own companion features or acquire IP, which would be a binary catalyst. IRBT remains the direct public proxy for consumer robot hardware.

- Buy exposure to compute and AI through NVDA, which supplies the chips that power perception stacks. NVIDIA's modules are increasingly central to on-device inference that companion robots need.

- Monitor AMZN and AAPL for platform plays. Amazon's ecosystem could bundle services, while Apple (AAPL) is a wildcard if it chooses to pursue ambient hardware tied to its services revenue.

- Consider SONY as a behavioral precedent; Aibo demonstrates that emotional robotics can be sustainable at premium price points.

- If you prefer a high-beta speculative play, track TSLA for its Optimus effort, where product timelines and manufacturing scale pose both upside and execution risk.

Position sizing should be modest. Treat exposure as a thematic allocation, not core equity. A 1 to 3 percent allocation to the robotics theme across hardware suppliers and compute beneficiaries makes sense for diversified portfolios, with a plan to add on demonstrable product-market fit, such as pre-orders or retail rollouts.

Investors should expect a multi-year path to commercialization; the novelty of an "abstracted bear" is real, but so are the engineering and behavioral hurdles to scale.

Final takeaway: this is a credible founder-led attempt to move consumer robotics from task automation to daily companionship. The nearest-term public plays aren’t the prototype maker, they’re the suppliers and platform firms. Watch for pre-orders, strategic partnerships and chip supply agreements as the first concrete signs that this prototype could become an investable market opportunity.