Share this article

Spread the word on social media

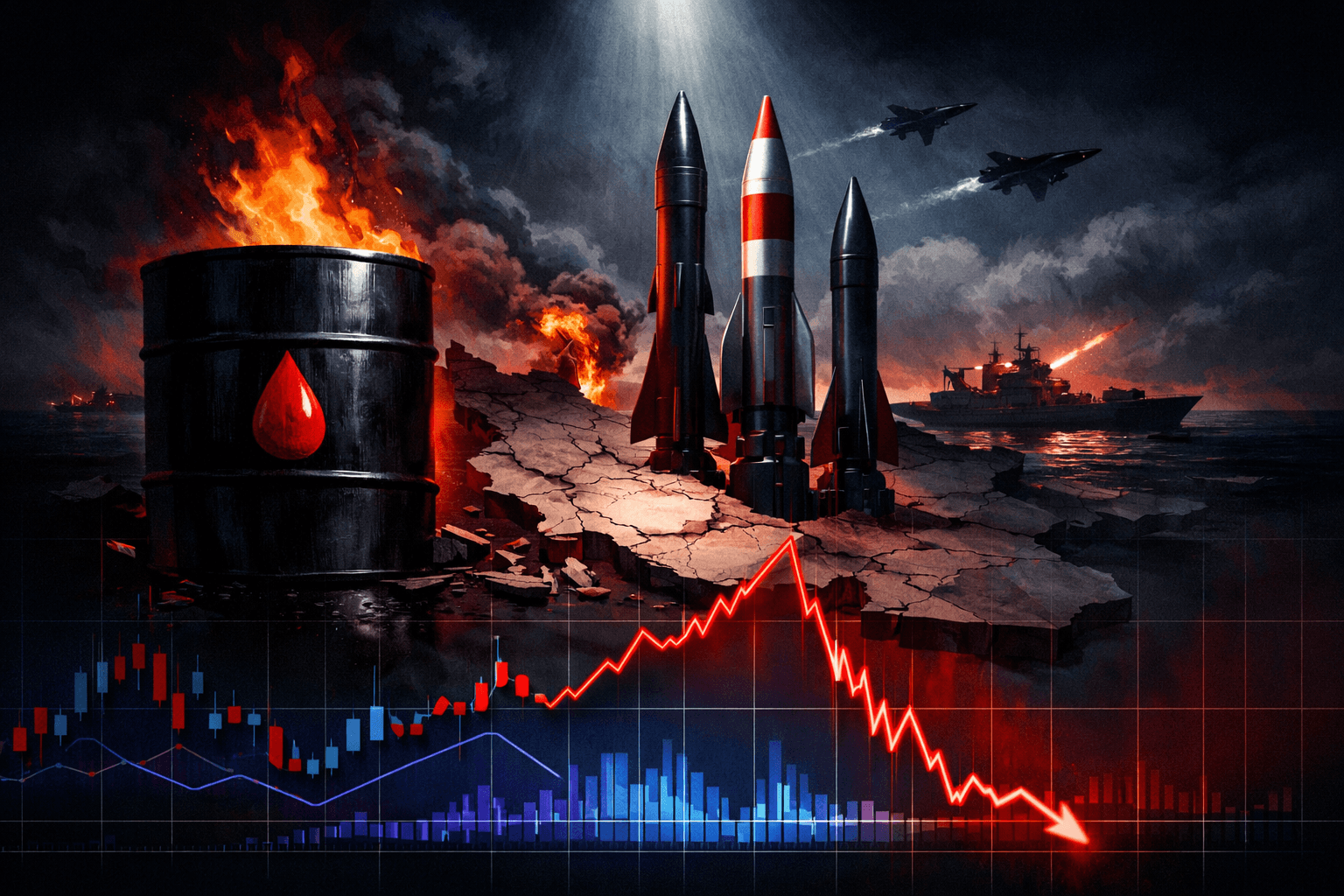

Opening hook: IMF warning arrives as Brent hits $111

The IMF warned in a blog post that "All roads now lead to higher prices and slower growth," as benchmark Brent crude climbed to $111 a barrel. With a U.S. deadline for Iran to reopen the Strait of Hormuz looming this week, markets are pricing in a higher-for-longer energy shock.

What happened: geopolitics pushed prices and the IMF pivot

An IMF blog post made the remark ahead of the IMF's global forecast release, expected around April 9, noting the conflict's economic fallout goes beyond oil. Brent at $111 already reflects a near-term re-pricing of risk across energy, shipping and agriculture inputs, and the IMF warned it will revise growth projections lower.

The disruption is concrete: shipping lanes are rerouting, freight bills are rising, and fertilizer supply chains face higher costs. Authorities set a Tuesday night deadline for the Strait of Hormuz to be cleared, creating a binary path for markets and trade flows in the coming days.

Why it matters: persistent inflationary pressure and slower growth

The immediate market implication is an inflation shock paired with growth drag. Our macro model at StockAlpha.ai shows a plausible 0.2 to 0.5 percentage-point hit to global GDP growth over 12 months if elevated energy prices persist, and a 0.3 to 0.8 percentage-point boost to headline CPI depending on pass-through.

Energy matters at scale: estimates vary, with roughly 20 to 30 percent of seaborne crude flows through the Strait of Hormuz (some sources put the figure as high as about one-third), so even temporary closures or insurance spikes materially raise transport costs. Higher freight and fuel bills quickly feed into consumer prices and corporate margins, squeezing discretionary spending and capex.

History offers a guide. The 1973 oil shock saw oil prices quadruple in months and produced stagflation, while the 2008 peak at $147 a barrel presaged a global growth slowdown and a 2009 recession. Those precedents show energy shocks can transmit to GDP within two to four quarters and linger longer if policy responses miss the timing.

The bull case: energy and defensive cyclicals outperform

In the upside scenario Brent remains elevated above $120 for months, which would raise free cash flow across majors and buoy energy equities. If sustained, we project integrated oil companies like Exxon Mobil (XOM) and Chevron (CVX) could see cash flow increases of 20 to 30 percent versus last year, supporting buybacks and dividends.

Higher shipping rates and tighter fertilizer markets benefit ZIM Integrated Shipping (ZIM) and fertilizer producers such as The Mosaic Company (MOS) and CF Industries (CF). Defense names like Lockheed Martin (LMT) and Raytheon Technologies (RTX) also gain from higher geopolitical risk premia.

The bear case: growth shock ripples through markets

The downside is a classic stagflation outcome, where Brent spikes above $130 and growth drops more than 0.5 percentage points. That forces central banks to choose between squashing inflation and protecting activity, increasing policy uncertainty. Equity multiples would compress, especially for high-duration growth names like NVDA and AAPL, and emerging markets could see capital outflows.

If the Strait reopens and Brent falls back toward $90 within weeks, the shock is transitory but volatility will still leave scars in supply chains and corporate margins. Even a temporary spike can lead to lasting investment delays and inventory rebuilding that slow growth for a quarter or two.

What this means for investors: concrete steps and tickers to watch

Rebalance defensively and be tactical. Increase energy exposure by 200 to 300 basis points from benchmark weightings, favoring XOM and CVX on cash-flow resilience. Add selective shipping exposure via ZIM and logistics plays UPS and FDX to capture freight repricing; consider Mosaic (MOS) or CF for fertilizer leverage.

Hedge macro risk with inflation-protected securities and defensive sectors. Allocate 2 to 5 percent of portfolios to TIPS or short-duration real assets if Brent stays above $110 for 10 consecutive trading days. Trim high-duration growth exposure by 100 to 200 basis points if the yield curve continues to steepen amid policy uncertainty.

Watch key triggers: if Brent trades above $120 for more than two weeks, move to overweight XOM/CVX and add ZIM and MOS. If Brent drops below $90 and the Strait reopens, reduce energy tilt and redeploy into cyclical recovery plays. Monitor the IMF report on April 9, weekly CPI prints, and shipping insurance premiums as high-frequency indicators.

Investor takeaway: Expect higher prices and slower growth; favor energy, shipping, fertilizer and defense, hedge with TIPS, and set clear price triggers to rotate as the crisis evolves.