Share this article

Spread the word on social media

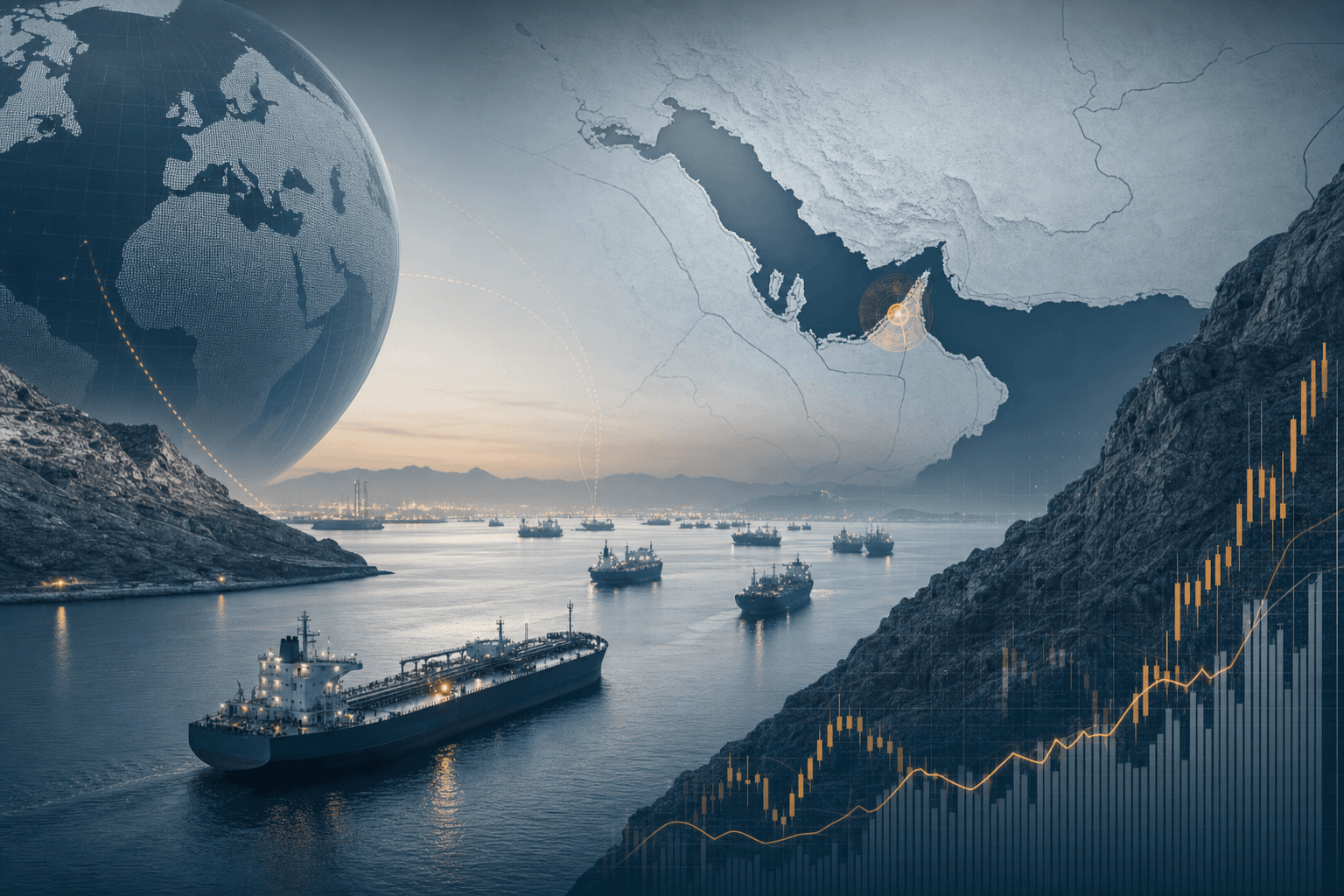

Hormuz traffic collapses to one crude carrier, Brent holds near $80

AIS tracking showed very low crude tanker traffic through the Strait of Hormuz on Friday; some AIS feeds recorded only one crude tanker that day, though other reports indicated several tankers exited the blockade around the same period, and Brent crude was trading just under $80 per barrel. The immediate shock is measurable, the political risk is rising, and the market is reacting with caution.

What happened: talks postponed, hostilities reverberate

The United States and Iran postponed scheduled talks in Switzerland on Friday after Israeli strikes targeted Hezbollah positions in Lebanon. Ship movements through Hormuz slowed dramatically, with vessel traffic down to a trickle; some AIS feeds recorded only one crude tanker clearing the strait that day, while other reporting indicated several Iranian tankers had left the blockade in the same period.

Hezbollah and Israel agreed to a renewed ceasefire late Friday morning, but the pause in diplomacy already shifted risk pricing. Casualty reports from the clashes noted 18 fatalities in Lebanon, according to the Lebanese health ministry, adding a human and political dimension that complicates any rapprochement between Tehran and Washington.

Why it matters: 20% of seaborne oil and the market's shock memory

The Strait of Hormuz channels roughly 20% of global seaborne crude oil, the equivalent of about 17–20 million barrels per day in normal conditions, into global markets that consume roughly 100 million barrels per day. A meaningful constriction in that flow changes the supply calculus immediately.

Oil markets price in both measured shortages and tail risks. Brent near $80/bbl today reflects that premium, and history shows how quickly sentiment can swing. In June 2019, regional attacks and tanker incidents produced a roughly 4% rally in Brent crude within two sessions as insurers and charterers repriced risk.

Shipping economics also shift. Vessels avoiding Hormuz must add distance by routing around the Cape of Good Hope, a detour that can add days to weeks to voyage times (estimates vary by route and vessel speed) and raise voyage costs materially. That reduces effective supply availability even when barrels exist, because physical delivery timing matters for refiners and traders.

The bull case: higher oil prices and an energy sector re-rating

If talks remain stalled and regional skirmishes restart, the market can reprice a risk premium quickly. A sustained reduction of just 10% in flows through Hormuz would be the equivalent of removing roughly 1.7–2.0 million barrels per day, a shock that could push Brent several dollars above current levels within weeks.

That scenario favors integrated majors like Exxon Mobil (XOM) and Chevron (CVX), which can capture wider upstream margins, and service names such as Schlumberger (SLB) that benefit from higher capex. Tanker names such as Nordic American Tankers (NAT) could see freight rates and utilization rise if longer sailings and risk premiums persist.

The bear case: disruption proves short-lived and demand softens

Diplomacy can reassert itself quickly. The ceasefire that returned on Friday, along with the potential for resumed talks in Switzerland, creates a credible path for traffic normalization. If flows return to pre-shock levels within 7–14 days, the price bounce could be fleeting.

On the demand side, global consumption is still vulnerable. A modest slowdown in emerging-market demand or a stronger dollar could wipe out a $3–5/bbl geopolitical premium, leaving previously buoyant energy names exposed. Refiners like Valero (VLO) can be cyclical losers if crack spreads compress sharply after the initial shock fades.

What This Means for Investors: concrete moves and tickers to watch

Short term, expect volatility. Position sizing matters more than direction. A 2–6% allocation swing into energy can capture a near-term geopolitical premium, but only if you accept higher intraweek swings.

- XOM, CVX — Tradeable on strength. These integrated majors have the balance-sheet capacity to sustain production increases and buybacks. Consider 3–6 month call spreads or incremental exposure if Brent closes more than $3 above current levels for three consecutive sessions.

- SLB — Service-play. Higher capex and reactivation of stranded projects lift service demand. Monitor tender flow and backlog; an uptick of 5–10% in contract awards would be a clear signal.

- VLO — Conditional play. Refiners benefit from stable crude prices and wide crack spreads. If Brent rises but benchmarks for gasoline and diesel widen more than $5/bbl, consider adding refiners.

- NAT — Tactical tanker exposure. Freight rates typically firm when routes lengthen. A sustained 10–15% increase in charter rates would validate a tactical overweight.

Risk control: use stop-losses and size for headline risk. If Hormuz traffic normalizes within 7 days, unwind short-duration trades. Conversely, if shipping insurance premiums and AIS data show continued routing away from Hormuz for more than two weeks, increase exposure to dividend-paying majors and tanker equities.

Actionable takeaway: favor selective energy exposure, prioritize balance-sheet strength, and treat any early rally as an opportunity to trim and rotate into high-quality producers and tanker plays if disruption persists.

StockAlpha.ai view: The immediate market reaction prices a plausible short-term supply squeeze, but the path to a sustained energy re-rating depends on whether diplomacy collapses or recovers in the coming 7–14 days. Manage risk, watch AIS flows and insurance premiums daily, and prefer names with cash flow resilience.