Share this article

Spread the word on social media

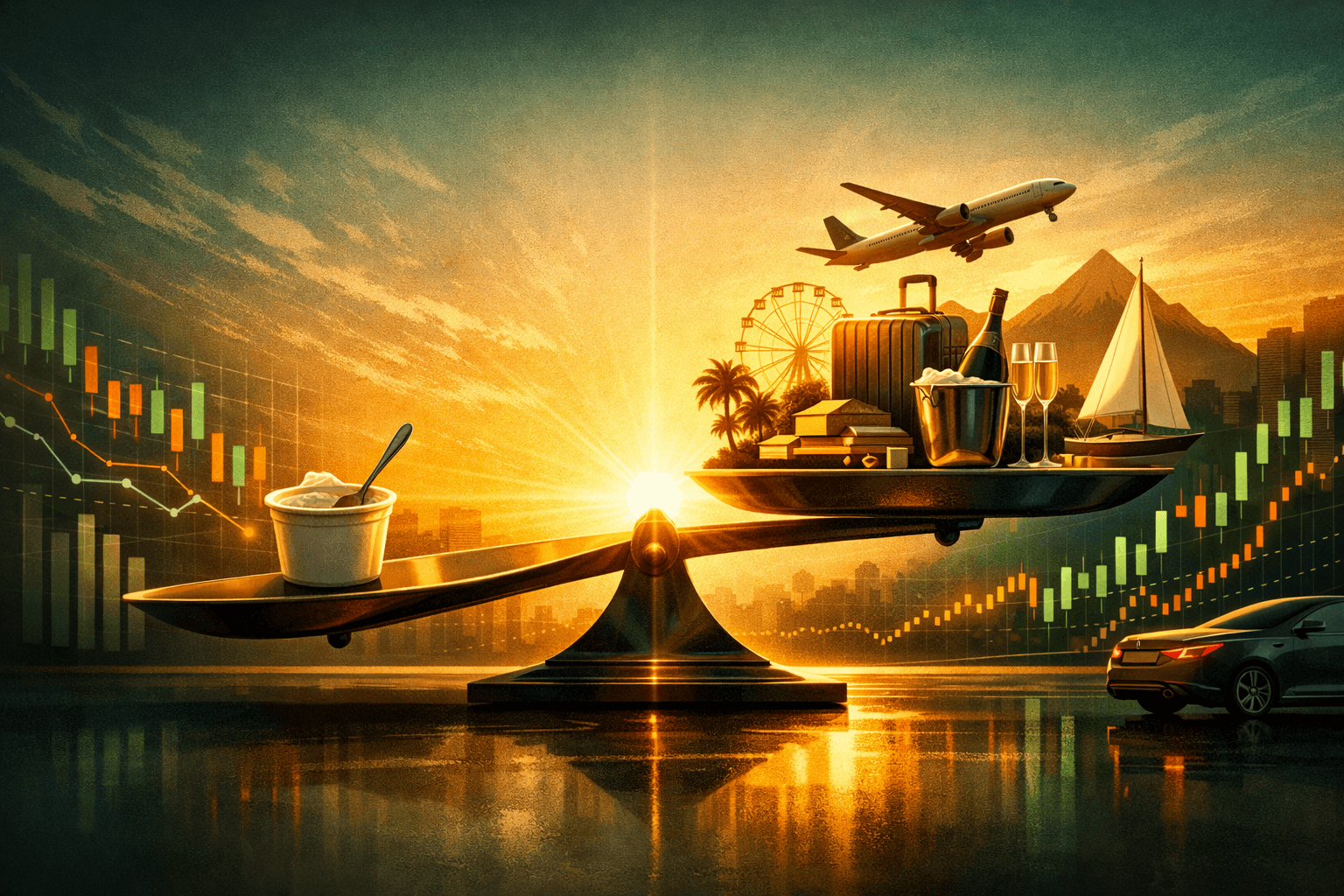

Affluent households trim basics while funneling cash into experiences

According to Federal Reserve data on household wealth, the top 10% of U.S. households hold a disproportionately large share of total household wealth (net worth), and that concentration is one factor behind a subtle but consequential reallocation of spending in 2024. High-income households — broadly those with annual incomes in roughly the top 10–15% of the distribution (income cutoffs vary by data source and year) — report cutting back on routine grocery items even as they increase purchases of travel, dining, and one-off experiences.

What happened: the frugal rich pivot from staples to splurges

Some surveys and transaction datasets through the first quarter of 2024 indicate two trends: essential grocery categories are softer among higher‑income cohorts, while experiential and premium discretionary categories are firmer. Retail sales for everyday grocery items have slowed relative to 2022 in certain measures, and bookings for premium travel and experiences have risen in some company-reported metrics.

Corporate signals match portions of the anecdotal evidence. Discount grocers and value-oriented staples sellers face flat same-store sales in many urban, high-income ZIP codes, while luxury hotels, boutique tour operators, and experiential platforms saw revenue acceleration into 2024 in specific reports. Investors are already repricing perceived winners and losers: experience and premium brands may trade at higher multiples versus traditional staples in many cases.

Why it matters: margin and mix, not just headline spending

This shift matters because affluent consumers punch above their weight in dollars. The top 10% by wealth generates a disproportionately large share of discretionary spend, so small changes in their behavior ripple across retail and services. A 5% reallocation away from low-margin staples into high-margin experiences can move earnings for certain consumer discretionary names by several percentage points.

Historical precedent matters. After the 2008 financial shock, luxury and experiential categories rebounded unevenly: premium dining and travel recovered faster than mass-market grocery chains. The current pattern echoes that recovery, but with higher starting levels of wealth concentration, meaning the elasticity of spending can be more potent now.

Macro context amplifies the effect. With inflation moderating in 2023 and early 2024, real disposable income for affluent households rebounded, enabling more ‘big ticket’ experiences. At the same time, value-seeking within everyday categories has been amplified by higher baseline prices, prompting substitutions like private-label yogurt instead of branded variants, or fewer spontaneous grocery purchases per week.

Bull case: durable demand for experiences and premium goods

In the bullish scenario, high-income consumers continue to prioritize experiences, sustaining revenue growth for experiential platforms and premium brands. Companies like Airbnb (ABNB) and Live Nation (LYV) stand to gain if bookings and ticket prices keep rising, and premium travel chains and luxury retailers benefit from higher margin mixes. If households in the higher-income cohort increase travel and dining spend by even 5% annually, that can produce meaningful incremental revenue for experiential players.

Technology and payment platforms also benefit. Visa (V) and Mastercard (MA) capture higher-ticket, international transactions, improving interchange revenue. Ecosystem winners with high-margin services, like Apple (AAPL) through Apple Pay and in-store experiences, may also see gains as affluent consumers remain heavy spenders on both gadgets and services.

Bear case: sustainability and distribution risks

The contrarian view is that the current pattern is cyclical and fragile. If economic sentiment sours or credit costs rise, affluent households can reverse discretionary spending quickly, and that would hurt high-multiple experiential names disproportionately. A 3% drag in premium travel bookings, for example, can compress consensus earnings for experience-centric platforms by 10-20% if investors had baked in steady growth.

Distribution matters, too. Grocery and staples companies with scale, like Costco (COST), can win share if value-seeking among the affluent deepens. Staples names with private-label strategies can offset volume declines with mix and margin management, creating a counterintuitive defensive hedge against experiential winners.

What this means for investors: tilt toward premium experiences, but hedge staples

Actionable positioning follows the core insight: prioritize exposure to experiential and premium discretionary names while keeping hedges in scaled staples. Favor platforms that monetize experiences and have durable network effects, like ABNB and Live Nation, where increases in bookings or ticket prices generally boost revenue due to fee-based models — although the exact revenue pass-through depends on each company’s take rates and cost structure.

Look for luxury and premium brand managers that reported double-digit growth in recent quarters and strong cash flow conversion; some such companies trade in a roughly 15-25x forward earnings band, but valuations vary widely and should be checked on a company-by-company basis. At the same time, keep positions in high-quality staples and value retailers such as COST as recession hedges; Costco’s membership model and trailing-12-month free cash flow provide ballast if spending retracts.

Monitor three KPIs monthly: 1) booking growth and average booking value on experiential platforms, 2) same-store sales in staples versus premium food retailers, and 3) premium travel spend in key metropolitan markets. A swing of 3-5% in any of these metrics should trigger a tactical rebalance.

Investor takeaway: tilt toward experiential and premium consumer names like ABNB and selective luxury retailers, but keep defensive exposure to staples such as COST. Track booking and same-store sales monthly and be ready to rebalance on a 3-5% swing.